The Census Bureau reported that new home sales for March declined to a seasonally adjusted annual rate of 511,000. This was below expectations of 522,000, but higher than March of last year. The median price of a new home contracted in March was $288,000, a YoY decline of $5,400. The average price of a new home contracted in March was $356,200, $3,500 more than March of 2015.

New home sales have remained grounded as the Fed’s “wealth effect” continues to diminish within the real economy. New home sales are still hovering around 1991 levels, due in large part because of the decline in U.S. household incomes. Lenders have been expanding the credit box to find more buyers and keep home sales numbers looking respectable, but that hasn’t solved the problem of the declining affordability of homes in general.

Recent comments from Dr. Allan Meltzer detail the problem very nicely. I think this paragraph gets to the heart of the “Federal Reserve Failures“:

“The chief beneficiaries of Fed policy gained from the rise in the stock markets. Speculators and short-term traders became a vociferous opponent of ending the very big increase in stock prices. What they fail to understand is that unlike the stock market the economy benefits from the rise in stock prices only if the rise in asset prices stimulates new investment. New investment occurs if investors see the lower price of new, current capital as a substitute for purchasing existing assets. This did not happen. Spending for new capital never increased in this recovery. Instead, companies bought existing assets, removing competitors.”

This, in a nutshell, is why the rich have gotten richer, and most American’s were left behind during the last 7 years of the “recovery”.

I think it also goes without saying that the policy blunders by our central bank also include facilitating a various assortment of fraudulent banking activity within our largest financial institutions which has made wealth and income inequality even worse. By ignoring one of their primary functions a regulator of the banking system, the Fed has lost virtually all credibility in terms of who they are really serving. It is patently obvious that the “wealth effect” has not reached a majority of the U.S. population, as profits and liquidity were skimmed off the top by those with first access to the capital.

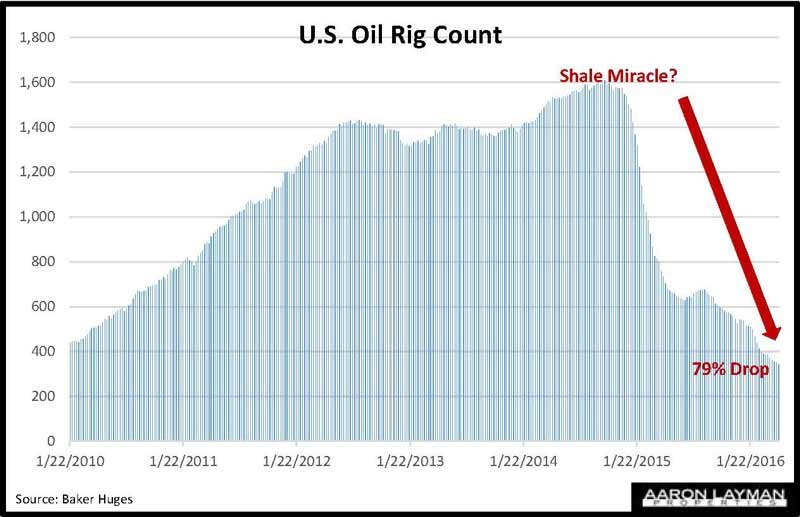

In the oil patch, the Fed’s illusion of endless liquidity has already unraveled in spectacular fashion as the fundamentals of supply and demand trumped the central bank’s charade…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment