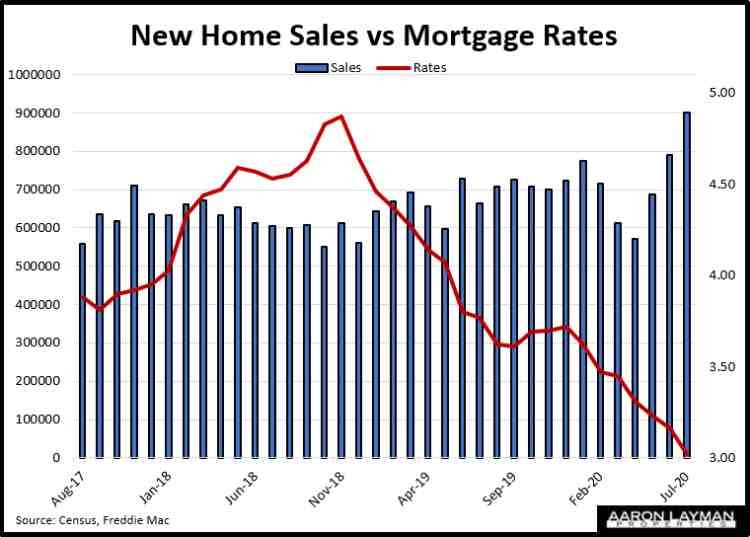

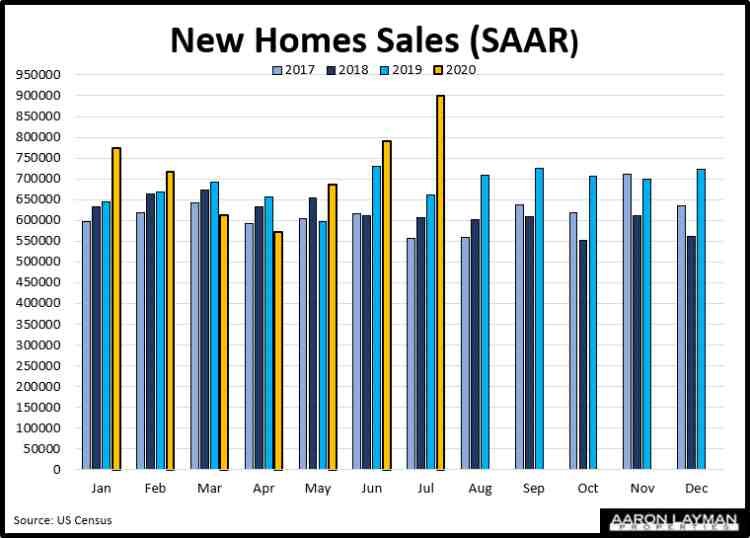

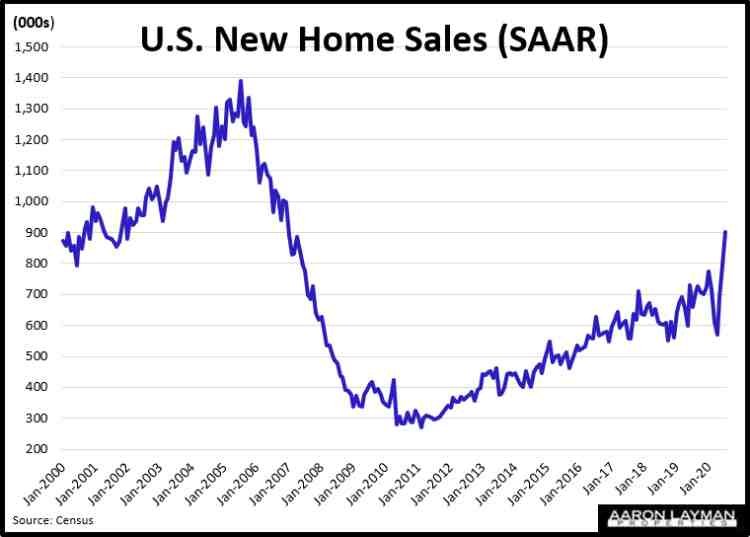

New home sales for July soared to a seasonally adjusted annual rate (SAAR) of 901,000. That was the best showing for the new home market since 2007 as sales increased 13.9 percent for the month and 36.3 percent compared to July 2019. Both median and average prices jumped, rising $330,600 and $391,300 respectively. The supply of new homes plummeted to 3.9 months looking at the unadjusted numbers.

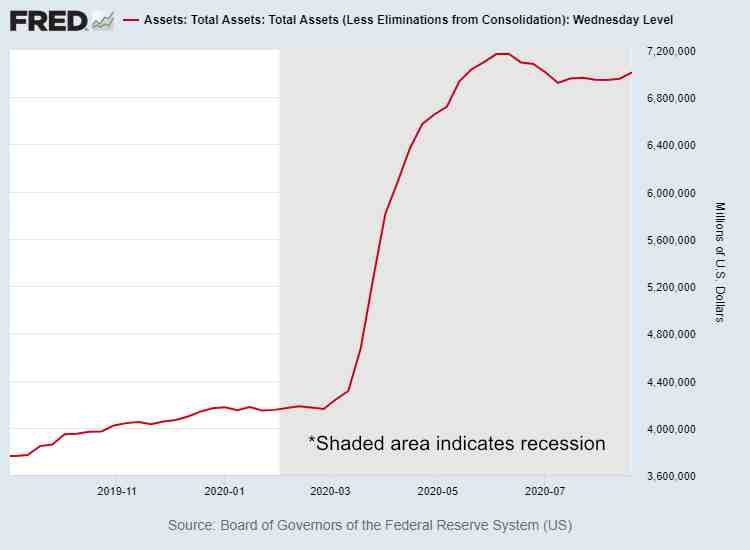

Record low mortgage rates and $trillions in stimulus courtesy of the Federal Reserve’s Covid-19 bailouts have proven to be the perfect recipe for home price inflation this summer. It’s almost as if the pandemic didn’t even happen…unless you look at the still elevated unemployment numbers and millions of mortgages in forbearance.

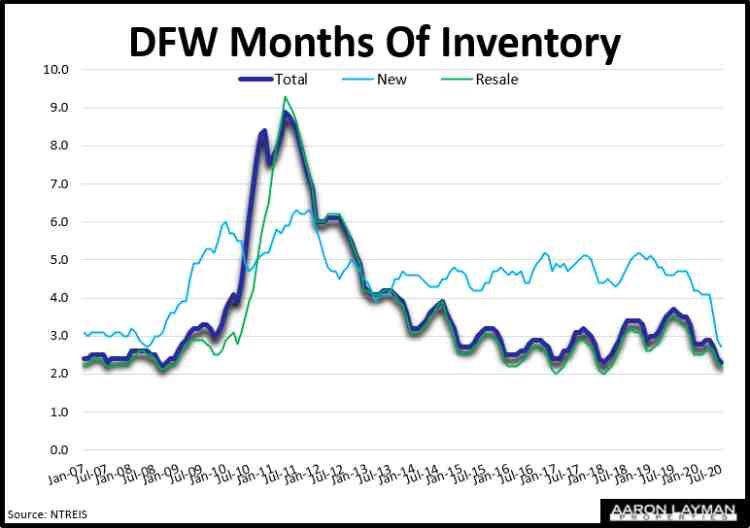

New home sales in North Texas were on a tear during July. Updated figures from NTREIS show closings of new construction soared 34 percent. Pending sales, the closest comparison to the Census figures, show contracts for new construction up 33 percent last month. As a reminder, Census counts a new home sale at the time of contract, not the actual closing.

Luxury home builder Toll Brothers reported earnings today which were also in line with the recent summer strength in the new home market. While Toll saw lower revenue and earnings during their third quarter, the luxury home builder saw a 26 percent jump in signed contracts for the latest quarter ending in July.

While the new home sales numbers for July are certainly encouraging, it is important to remember the price tag. It took $trillions in artificial stimulus to facilitate the recent V-shaped recovery in housing this summer. The bill for the Fed’s latest intervention hasn’t been paid yet. Inventory is running thin, and prices are at record highs. That’s before you even look at the underlying economic headwinds. Something’s going to give. It’s just a question of the timing now.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment