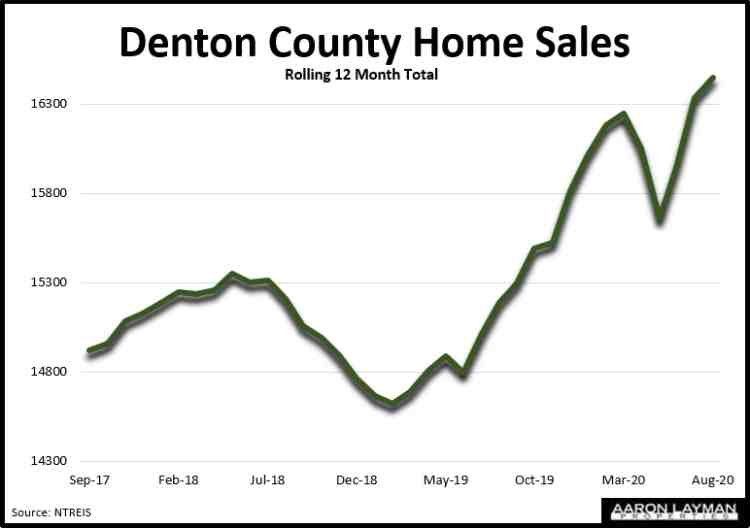

The North Texas real estate market continued to ramp higher in August. Median home prices in Denton County jumped 6.3 percent last month, with average prices rising 7.4 percent compared to a year ago. Denton County home sales increased 10 percent, while pending sales for Denton County homes shot 33 percent. Home buyers are still riding that wave of liquidity, and who can blame them. Mortgage rates just hit a new record low in the latest weekly survey, with the rate on the 30-year fixed dropping to 2.86 percent.

Those low rates helped push North Texas home prices through the roof this summer. The median price of a DFW home rose 8.6 percent in August. Average prices were up 11.2 percent compared to August 2019. Home sales in North Texas are experiencing a V-shaped recovery and inventory is scraping the bottom of the barrel. Months of supply dipped to just 2.1 months in August. Months of supply for new homes in Dallas-Fort Worth plummeted 47 percent from last year, dipping to just 2.5 months. In case you’re wondering, that 2.5 months of inventory for new construction is lower than what we saw in the spring and summer of 2008, just before the mother of all housing bubbles came unglued and nearly destroyed the world economy.

The housing market is waiving off concerns about the economy and the more than 1 million Texans still on insured unemployment. The September employment report showed the U.S. has recovered over 10 million jobs since April, but employment is still 11 million jobs below the February peak! No worries. Central bank liquidity is all we need for a party, and so the show continues. It’s a great time to be in real estate if you are a homeowner or a home seller. Not so much if you are a prospective buyer trying to find a home in a market where asset prices are being pushed to their limits.

Buyers who are still employed or have assets are taking advantage of record low rates to buy homes. Some are cashing in gains from the stock market ramp. The north Texas real estate market continues to benefit from multiple levels of support, including excessive liquidity, low rates and competition among multiple buyer cohorts.

Jerome Powell made it clear at the recent Jackson Hole conference that the Federal Reserve has no real plans other than more of the same. Looks like it’s going to be low rates forever as the Fed attempts to inflate away an even large pile of debt. The Fed couldn’t achieve their 2 percent inflation target for the past decade, so Powell’s answer is to keep his foot on the accelerator until the car skids off the road. That means more trickle-down monetary stimulus poured through a corrupt financial system. Powell and his Fed colleagues are letting asset inflation run hot while they keep rates low for years to come, praying for a soft landing. For those old enough to remember this movie, just visualize the ending of Thelma and Louise.

Powell’s highway to a soft landing is riddled with potholes. Many Americans aren’t benefiting from all the cheap capital, certainly not savers. While Wall Street is issuing tons of corporate debt to keep their sinking ships afloat, record low rates don’t help the millions of Americans who are out of a job and can’t qualify for a loan. The low rate bonanza also has a nasty side effect in terms of stimulating home prices and market speculation. It is already evident that home price inflation has cancelled out much, if not all of the additional purchasing power for Denton area home buyers this summer.

The Real House Price Index (RHPI) from First American showed Dallas Texas in the top 10 on a recent list of metro markets where housing affordability actually declined. Things look pretty similar in Denton County. Using Denton Texas an example, imagine a hypothetical purchase price for an average home. For August 2019 the rolling 3-month average price in Denton was $282,221. The 30-year fixed rate mortgage rate averaged 3.73 percent in the summer of 2019.

With rampant home price inflation this summer the 3-month rolling average of a Denton home was $299,670. The average interest rates this summer was 3.04 percent according to Freddie Mac figures. Assuming you were making a 20% down payment, the principal and interest payment on last year’s purchase would have been $1043. The same payment this year on a more expensive home at a lower interest rate would be $1015.

Your purchasing power barely increased with these record low mortgage rates, and that’s assuming you still have the same job with the same income. Factor in higher property taxes on the more expensive home and you are likely staring at zero to negative improvement in terms of real home purchasing power.

The dirty little secret in the Marriner Eccles building is that the Powell Fed is still practicing the same brand of trickle-down crony capitalism benefiting existing asset holders, Wall Street and those with first access to the Fed’s cheap capital. For a good primer on how the Fed dupes working Americans into spinning their wheels Powell’s recent interview with NPR is a must read. The misdirection, half-truths and outright lies are just part of the working script at the Federal Reserve.

Steve Inskeep’s question regarding Fed policies and inequality elicits an utterly comical response from Jerome Powell which is both insulting and laughable. It is obvious Powell will twist himself into a pretzel six ways to Sunday before he ever admits the obvious truth that the Fed’s polices are a direct cause of income and wealth inequality. It’s a sad joke. If you are typical working American watching the purchasing power of your currency being inflated away by Fed policy as you struggle to buy a decent home, the joke is on you. Make it a double if you are a recent buyer with an FHA mortgage.

FHA delinquency rates in several Texas markets are just one cause for concern. FHA borrowers frequently use the smallest down payments, and thus have little to no equity when they initially purchase a home. If markets turn south and home prices decline even slightly, borrowers can find themselves upside-down on their mortgages. That means they owe more on the mortgage than the home is worth in the open market. Research from the American Enterprise Institute shows that 1 in 6 FHA loans in the U.S. is currently delinquent. More than 1.36 million FHA loans in the portfolio of 8 million are currently delinquent. Houston, San Antonio and Fort Worth made the list of the top 10 metro areas with the greatest risk of FHA delinquencies.

But hey, Party on!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

It’s like there’s a party in the market, and I’m not invited….