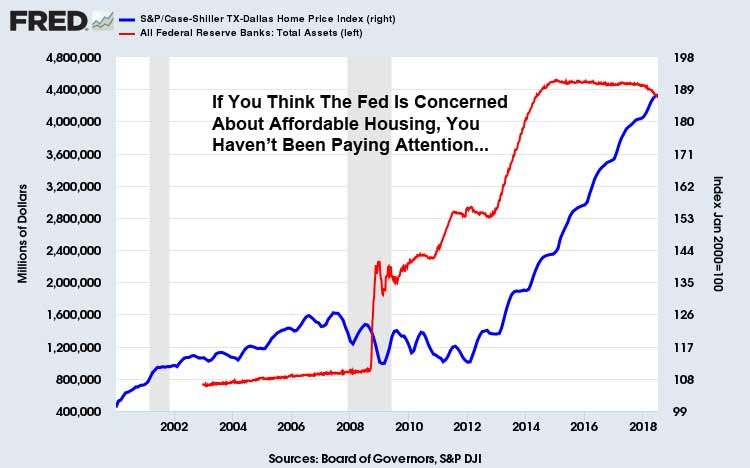

The Department of Housing and Urban Development’s Fiscal Year 2018 report to Congress is filled with useful information on the state of the U.S. mortgage market. Contained within the 2018 annual report we can see where the latest crop of underwater borrowers are hiding in Denton County Texas. As the size of new homes continues to shrink, particularly for entry-level buyers, prices increases have begun to moderate or even decline in many areas. This poses a big problem for unsuspecting home buyers who have been roped into the housing market at the cycle peak with little or no down payment.

As home prices have rising throughout North Texas in the latest echo bubble in housing, mortgage lenders have loosened restrictions to get more borrowers qualified in the face of rampant home price inflation. The FHA mortgage program has been no different. The quality of FHA loans has deteriorated this year, with debt-to-income (DTI) ratios climbing while average credit scores have fallen.

Exhibit I-8 shows us that the average FHA borrower credit score of 670 was at the lowest levels seen since 2008. That year might sound familiar. In figure I-9 you can see the rise in lower tier credit scores while the pool of borrowers in the 720 or higher category has decreased dramatically. In Layman’s terms, FHA borrowers are looking increasingly like subprime borrowers!

This deterioration in new FHA loan quality is confirmed by the sharp increase in debt-to-income levels during the last three years. Exhibit I-10 shows us that the average DTI ratio of 43.09 percent for FHA purchase mortgages is at the highest levels ever since fiscal year 2000. The pool of FHA borrowers with DTI’s between 43 and 50 percent is growing, and the proportion of borrowers with debt-to-income ratios above 50 percent is now up to 24.8 percent of the total pool of borrowers, an all-time high since fiscal year 2000. Yikes!

If you are buying a home and putting less than 5 percent down for your down payment, the odds of becoming an underwater borrower increase dramatically in a shifting market. Now that we have likely hit the cycle peak for this latest real estate cycle, it is certainly concerning to see the deterioration of the quality of FHA loans. You would have thought that we learned our lesson 10 years ago, but obviously nothing has really changed.

During the third quarter of 2018 the median single-family square footage of a new home decreased to 2320 square feet while the average size of a new home fell to 2495 square feet. You know you at the peak of the housing market when even the National Association of Home Builders is writing about the not-so-well-kept-secret that home sizes will likely keep shrinking as the custom home market cools. As builders struggle to build more entry-level (aka affordable) homes, buyers are getting pinched in ways they may not fully understand or appreciate. Buyers are getting less home for their money in many markets as prices remain at elevated (inflated) levels.

The problem with receiving less home for a higher price is that when the tide rolls out, borrowers who have put down little if any down payment on their now smaller piece of the American dream become upside-down renters paying property taxes on a depreciating asset. As any good real estate broker will tell you, it’s the REAL ESTATE (the dirt) that is key to a wise home purchase. If you are buying a poorly-constructed starter home on a deficient piece of dirt, it is now incredibly easy to become one of America’s new underwater borrowers. The latest data on FHA loans shows exactly how this is happening in Denton County Texas.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment