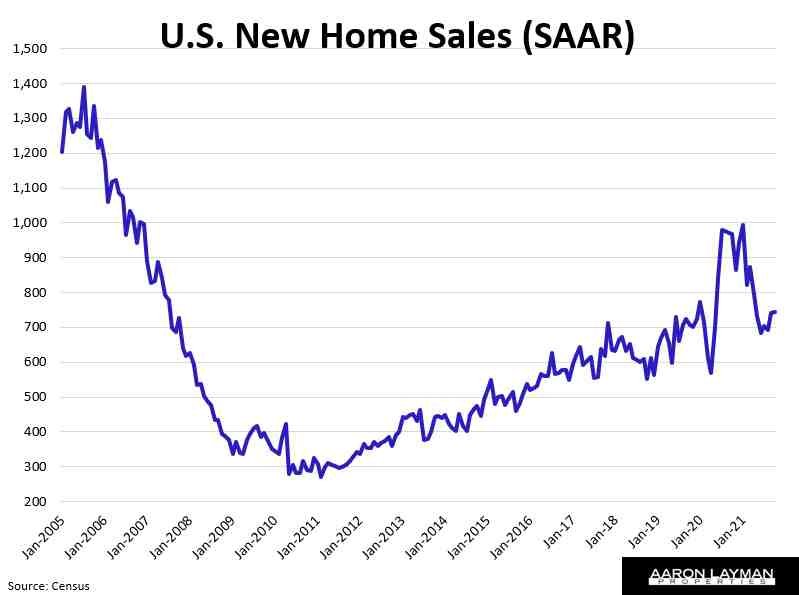

New home sales came in lighter than expected for October. The previous three months were also revised lower. Census numbers showed October new home sales at a seasonally adjusted annual rate (SAAR) of 745,000 units. Months of supply rose slightly to 6.3, but up 80 percent from last year. If supply is so abundant, why aren’t new homes selling like hotcakes?

The answer lies in the real unadjusted data. The Census Bureau puts a lot of seasonally adjusted optimism into their figures. Headline Census estimates for new home sales get repeated by major media all the time as gospel even though they are estimates of contracts, not actual new home closings/sales. It would be more accurate to call them pending sales of new homes.

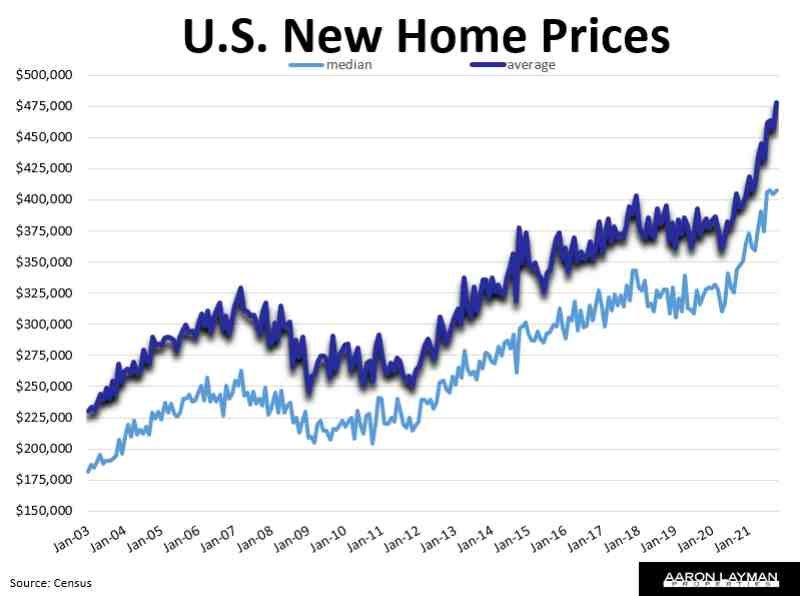

The problem with new home market right now is sky high prices and limited finished inventory. New home prices hit record highs last month. Median and average new home prices hit new highs of $407,700 and $477,800 respectively. No inflation there, right. Considering the recent bump in mortgage rates above 3 percent, the sticker shock for prospective new home buyers was even more pronounced last month.

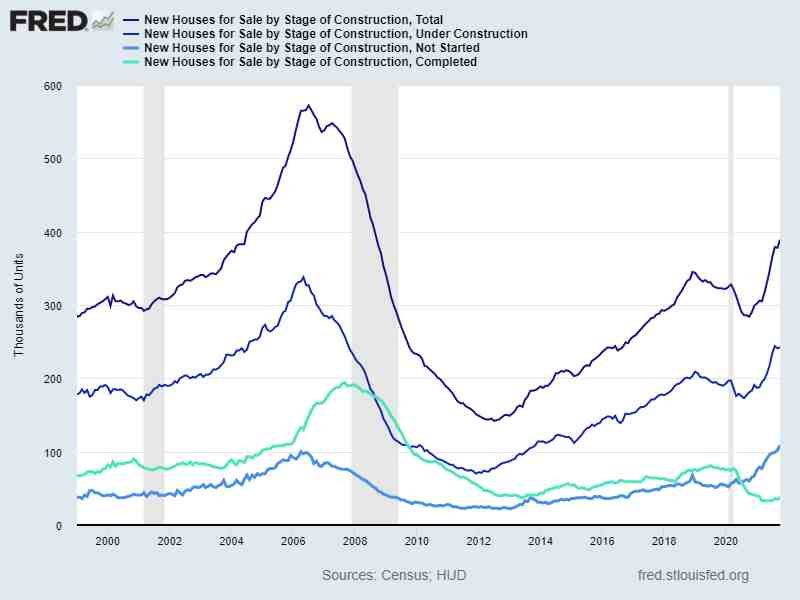

Digging deeper into the unadjusted data, the headline stat of 6.3 months on new home inventory is a seasonally adjusted work of fiction. Yes, there is a huge amount of backlogged new home construction, but the amount of finished or near-completed new home inventory is still extremely thin. Of the 388,000 new homes for sale at the end of October, a record 106,000 had not even been started. Another 245,000 were under construction. Only 38,000 new homes for sale were actually completed. The median months for sale was just 2.4 months, meaning buyers were picking off inventory at a very brisk pace once a new home was completed.

With the Federal Reserve still priming the economic pump, existing asset owners have been willing to stomach record high prices for new homes. With the stimulus unwind now underway, some buyers are having second thoughts. Buyers always love that new home smell, but there is a limit to everything.

We are seeing this play out in Denton County Texas where the median price for a new home hit a record $195 per square foot in October, shattering the previous high of $183 in September. New home sales in Denton County tanked 52 percent compared to last year as inventory fell back to just 2 months of supply. Pending sales of new homes were down 7.6 percent compared to last year. Pending new home sales have been trending up since June when we essentially ran out of new home inventory.

Builders in the North Texas area have been ramping up new developments and production trying to catch up with demand. Buyers have responded by signing contracts to build. If you want a new home in North Texas, completed inventory is hard to come by, but there are plenty of opportunities to build from the ground up if you are willing to take a leap of faith in this hyper-inflated market.

The following chart shows how new home inventory looks by various stages of construction. The number of homes under construction has ramped up significantly, but it’s still below the previous peak. The number of homes not yet started is has spiked to a record high while completed inventory is still near record lows. The next time you hear someone talk about a housing crash due to a glut of construction, just show them this chart. Builders are still doing a decent job managing their pipelines and inventory.

Much of the talk about supply chain issues and cost increases for builders is also driven by narrative and spin. New home builders are still raking in huge profits. Publicly-traded builders have been buying back their own stock hand over fist this year. They’re spending way more money buying back shares than they are on warranty service for the homes they build.

Hearing builders complaining about “challenges” in the current market is a bit like listening to billionaires complaining about having to pay taxes. Government (and particularly Federal Reserve) policy continues to feed the wealthy at the expense of the general population and longer-term growth prospects. With inflation raging, the Fed is still pumping over $100 billion per month into the markets because apparently the rich don’t have enough new homes to buy for their second or third vacation rental.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment