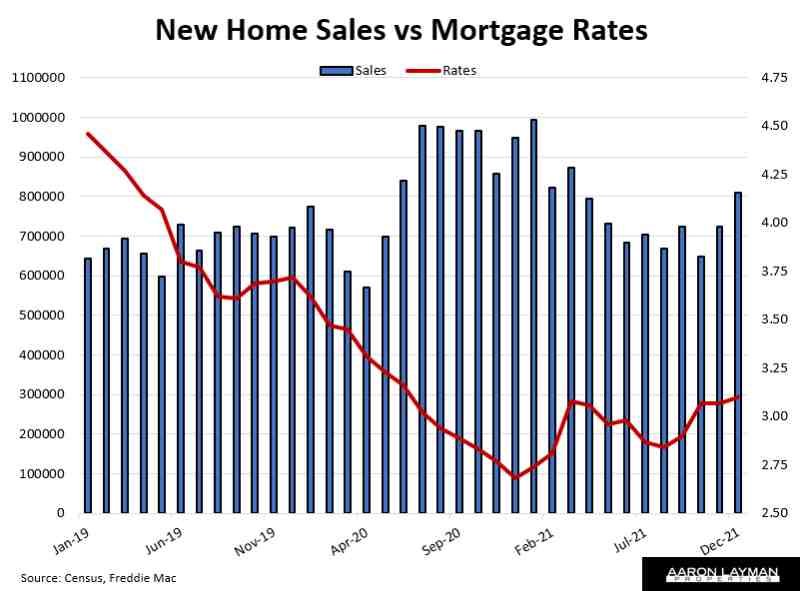

New home sales were a bit better than expected in December. The Census Bureau reported new home sales at a seasonally adjusted annual rate (SAAR) of 811,000 units. Previous months were revised lower. The median price of new home came in at $377,700. The average price of new construction contracted in December was $457,300.

New home sales are still suffering from supply constraints. Completed inventory remains very low while the number of units technically for sale remains very high. Looking at unadjusted numbers out of the 408,000 homes “for sale” at the end of December 104,000 had not started construction! Another 263,000 were under construction, while only 42,000 completed new homes were available for sale.

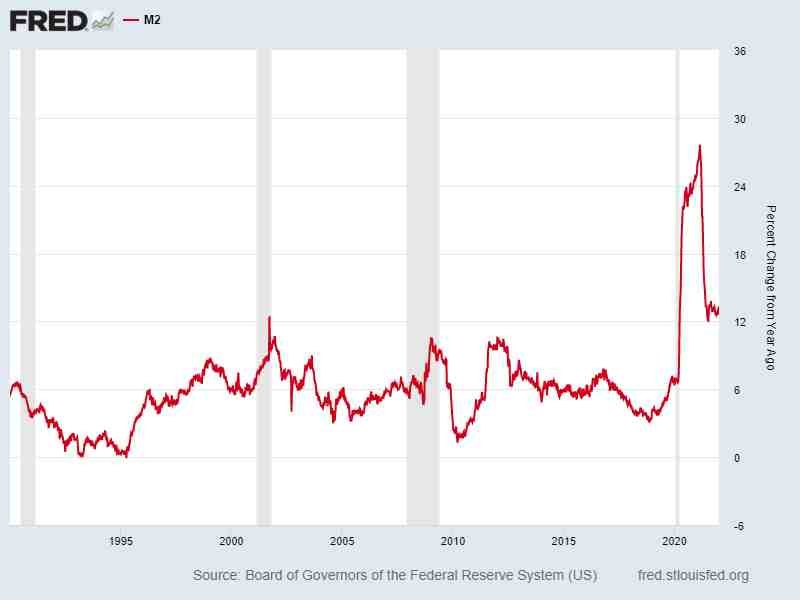

The supply constraints are only one symptom of a much larger problem. Spiraling inflation and record high home prices pose a huge challenge for housing this year. That lies squarely on the Fed. Not surprisingly, the Federal Reserve punted again on taking concrete action. Today’s FOMC policy statement just reiterates that quantitative easing (QE) will end in March. The Fed left the Federal Funds rate at the zero bound, with rate hikes to be considered at the March meeting.

Recent volatility in the stock market has the Fed spooked. The Fed is woefully behind the curve again. Treasury bond rates jumped after the Fed announcement. They smell a rat…and it’s a big one. It’s pretty ironic that Jerome Powell explicitly mentioned in his press conference how average Americans are burdened by high inflation, and yet he’s still fanning the flames of inflation!

The longer the Fed puts off taking the medicine, the bigger the problem grows. The equity markets are already figuring this out. The housing market will get on board soon enough. It’s only a matter of time. Liquidity flows continue to drive the real estate market but the tide is turning in the wrong direction for housing. Think of it as a big ship that’s difficult to steer. Housing is a lagging indicator.

Real estate pundits are still talking up the hot numbers for December and the pent-up demand for homes as we start 2022. What they fail to recognize or admit is that liquidity has been driving the action in real estate during the pandemic.

If you are in the market for a new home (any home for that matter), mind the flows. 2022 is going to be a bumpy road. Contrary to all of the spin about full employment and price stability, the Fed is a master of mayhem. Bubbles are what they do best. Apparently they just can’t help themselves.

Mortgage interest rates are already spiking, and the Federal Reserve hasn’t even started actual quantitative tightening. When the guard rails are removed in March Jerome is going to have a big mess to clean up.

With the Federal Reserve behind the curve, Jerome is going to have plenty of catching up to do. I know a lot of agents who think the spring selling season is going to be solid despite rising mortgage rates. Many of the agents currently selling homes probably haven’t even seen a down market. 2022 will be a year where you want to choose your representation wisely.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You’re the only agent I’d use, if I actually had any money….