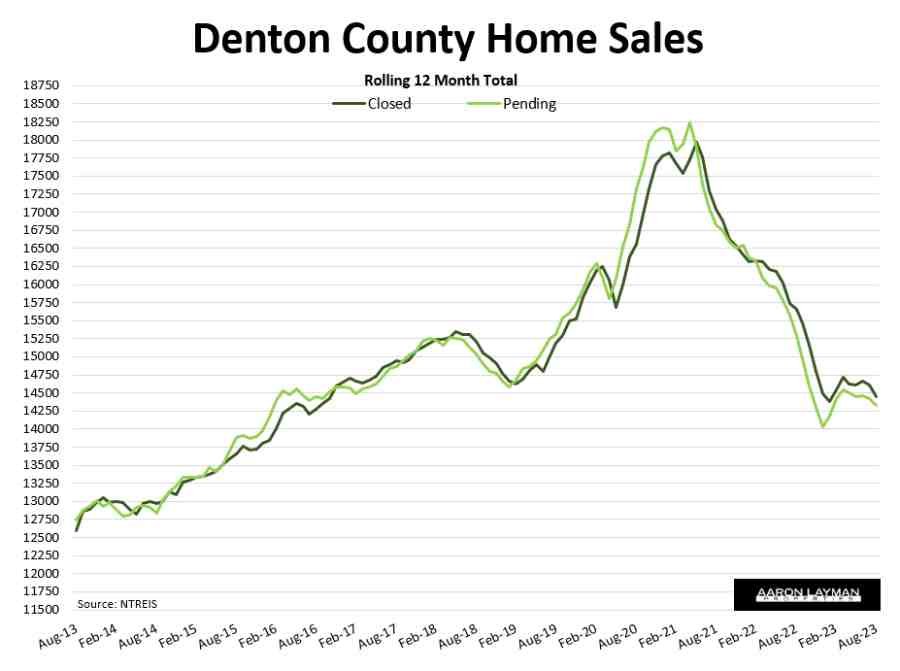

Denton County’s real estate market ran into significant hurdles in August. Mortgage interest rates for prospective buyers reached a new high for the cycle. That took a bite out of sales activity as the summer winded down. Closed sales in Denton County fell ten percent form the same time last year. Forward-looking contract activity slid 5 percent. Median and average home prices also cooled for second consecutive month.

One thing that didn’t cool in August was the incentives and mortgage-rate buydowns offered by new home builders. New home builders are agnostic sellers. They do what they have to if they want to hit their quarterly sales targets and make payroll. This is why we’ve seen incentives from major builders ramp up once again. In the fourth quarter of 2022, builders saw the writing on the wall and took appropriate measures. They are doing it again!

Incentives from builders have approached the $20,000-$30,000 mark on many recent contracts. These big seller concessions are NOT reflected in the reported sale prices you see in the media. This is a critical point if you really want to understand what it takes to sell homes in the current environment. Real net median and average sale prices were probably $10,000 lower than what has been reported in the normal statistics. If you don’t factor in the huge seller concessions or BTSA’s (bonus to selling agent), you can make the reported sales figures (and the overall market) look stronger than it really is. This exactly what’s happening.

Available home inventory in Denton County has continued creeping higher for the last six months. This is a direct result of diminished affordability. As area house payments for prospective buyers have reached new record highs, sales activity has continued to cool. New listings have been recovering. Demand has been getting flattened at the same time. Days on market moved higher in both July and August while percent of list price received by sellers cooled for the second consecutive month.

The Denton County real estate market appears to be rolling over again as we end the summer of 2023. The interesting part of this backdrop is that it comes on the back of a massive $2 trillion budget deficit from Uncle Sam this year to keep the show going. The Fed has been tightening policy, but the Biden administration has been spending like a drunken sailor to maintain the illusion of a strong economy.

The labor market remains relatively tight, but stress continues to build in the real estate sector. Inflation is still rippling through the economy in various forms as the Federal Reserve continues its game of whack-o-mole. With the U.S. government issuing boatloads of new debt, the big question is who is going to buy it all. That has some major implications for mortgage rates. We could still see higher mortgage rates this cycle before the next recession arrives.

Insufferable partisan hacks like Nobel-Prize-winning economist Paul Krugman are getting ratioed for their buffoonery. Krugman stands out for his comically tone-deaf attempts to talk up the “disinflation” narrative. Krugman had the audacity to post a chart of inflation excluding food, energy, shelter and used cars as “evidence that inflation has been largely defeated”. It’s good to know if you exclude all of the things you need, inflation is relatively tame. LOL!

In the realm of intellectually dishonest people there is a continued effort to play up any progress if it helps to support “their team” or a preferred narrative. In the real world, people are busy dealing with prices they actually pay. That often includes interest costs, something not included in the CPI formulas. Normal people are too busy trying to make ends meet. Most Americans see the reality of actual prices and payments spiraling higher.

There are a ton of moving parts and plenty of uncertainty as we head into the last quarter of 2023. If you are in the market to buy or sell a home, it will be prudent to stay flexible and keep an eye on the bond markets. 2022 showed us what can happen when the pundits and industry cheerleaders ignore the warning signs staring them in the face. The first half of 2023 renewed the hope and optimism for that elusive soft landing. History tells us it’s not quite that easy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment