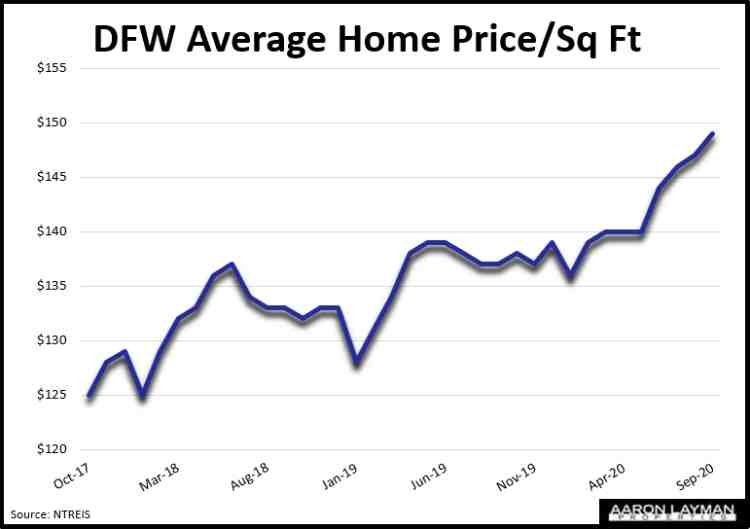

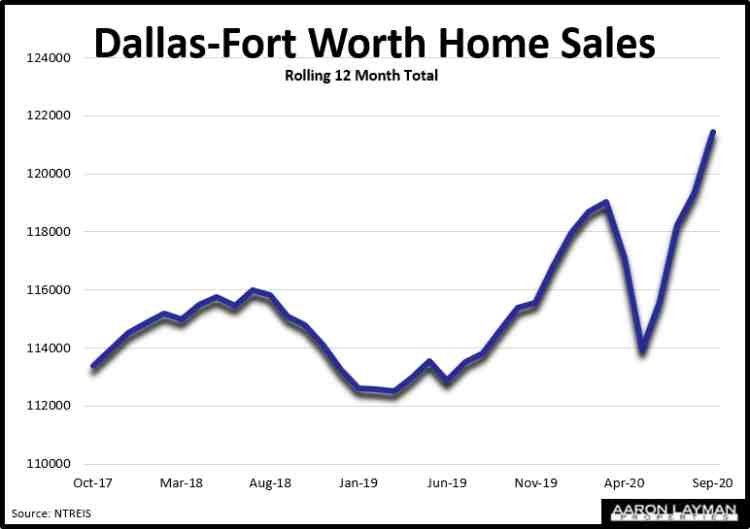

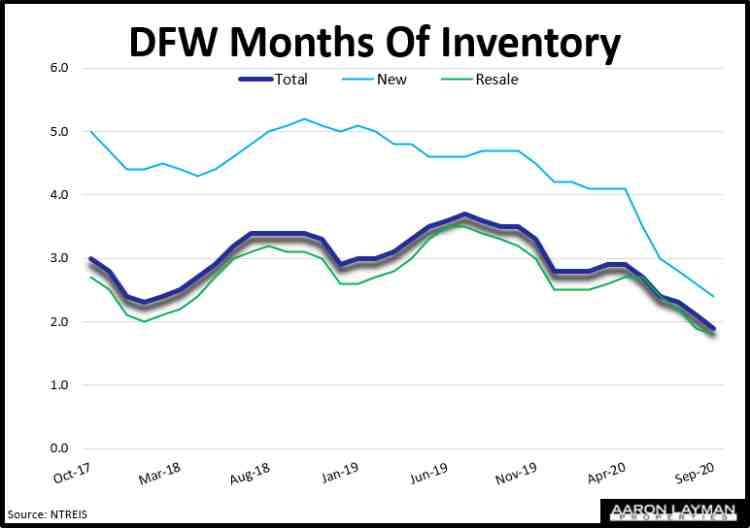

North Texas home sales continued to defy economic stagnation in September. NTREIS data reflect a 24 percent rise in home sales in the DFW area last month. Pending sales look to be up by 17 percent. The median price of a DFW home jumped 10.3 percent compared to a year ago. Average prices climbed 13.4 percent. Months of inventory plummeted 46 percent to just 1.9 months of supply.

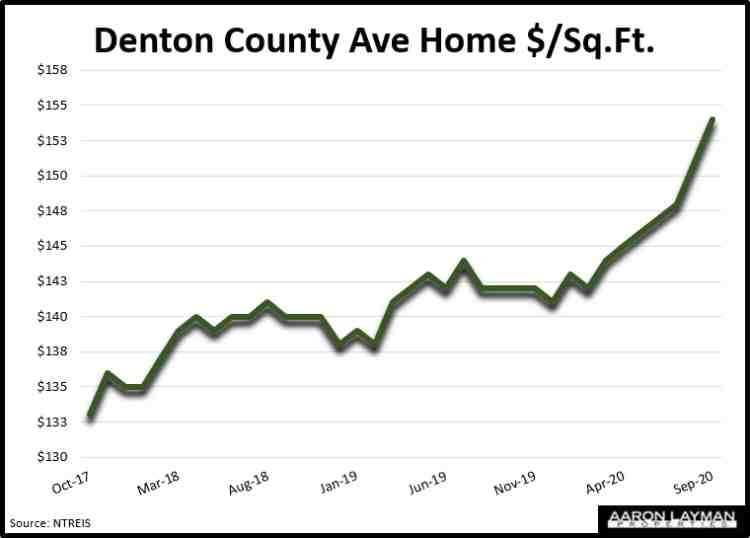

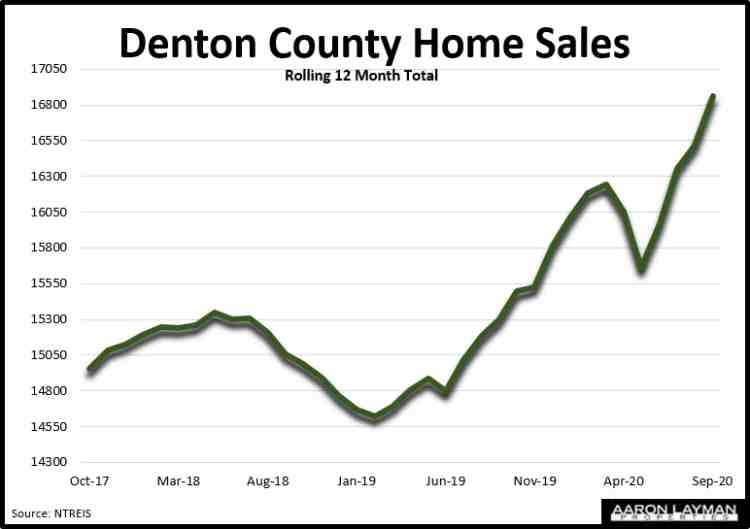

Denton County home sales skyrocketed 30 percent with pending sales up 18 percent. The median price of a Denton County home jumped 7.8 percent while average prices were up 10.9 percent from the same time a year ago. The available inventory of homes in Denton County nosedived 53 percent to a new record low of just 1.5 months supply. Available inventory has all but vanished from the market as the supply of new homes has failed to keep up with demand.

Across Denton County the supply of new construction dipped to a new record low of just 1.8 months supply. That’s a 60 percent drop from this time last year. For the entire North Texas market the supply of new homes fell 49 percent to a new low of just 2.4 months of inventory.

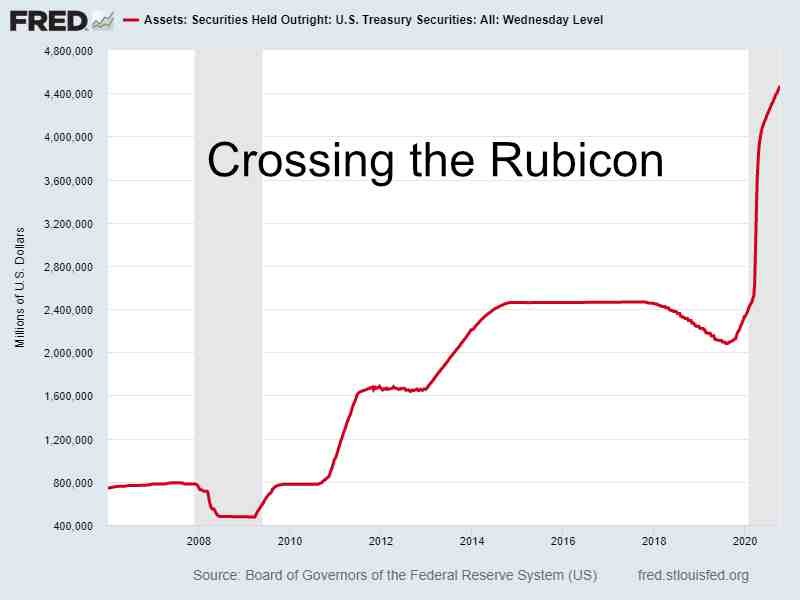

The Federal Reserve has continued to flood the market with liquidity and jawbone asset markets higher. All of that liquidity has combined to create the perfect storm for home price inflation. We are still in the middle of a pandemic and recession yet DFW and Denton County home buyers are paying record high prices for homes. With the Fed backstopping hedge funds and Wall Street buy-to-rent landlords, speculation in the housing market has seen a dramatic resurgence.

First-time home buyers and many millennials are getting buried by $trillions in new Federal Reserve trickle-down stimulus. It’s almost as if the housing market doesn’t care that weekly unemployment claims are still running above 800,000…per week. The latest report from the BLS shows the 4-week average of weekly unemployment claims at 857,000!

“The sense of responsibility in the financial community for the community as a whole is not small. It is nearly nil. Perhaps this is inherent. In a community where the primary concern is making money, one of the necessary rules is to live and let live. To speak out against madness may be to ruin those who have succumbed to it. So the wise in Wall Street (and in the professional and credentialed class) are nearly always silent.” John Kenneth Galbraith, The Great Crash of 1929

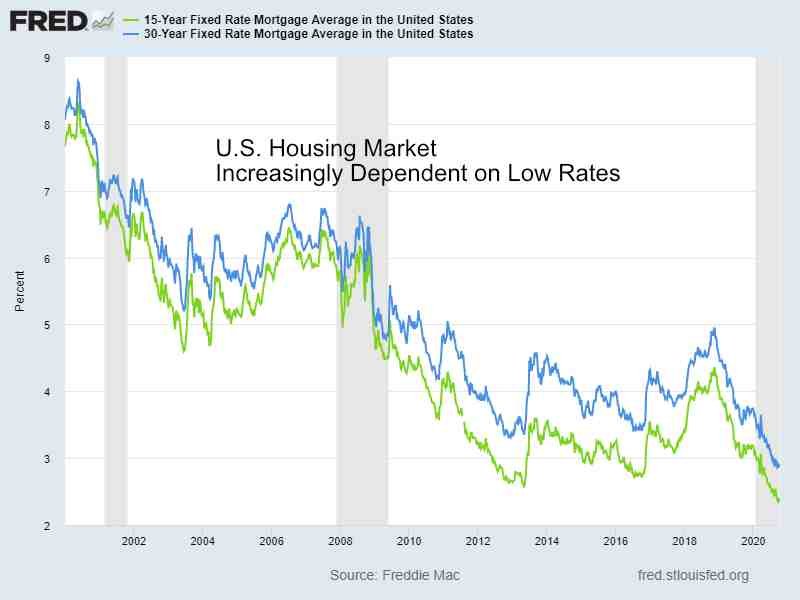

This is not your father’s housing market for sure. It’s hyper-financialized, fragile and potentially dangerous. If the multiple levels of support and stimulus are removed, look out below. There’s a reason Jerome Powell and the Fed are calling for low rates until 2023. The housing market would become an unmitigated disaster with any significant rise in rates at this stage. The Fed has no credible plan to reduce its now $7 trillion balance sheet. The Fed’s answer is always moar. The Federal Reserve is monetizing debt like there’s no tomorrow.

Rates are low because they have to be to keep the show going.

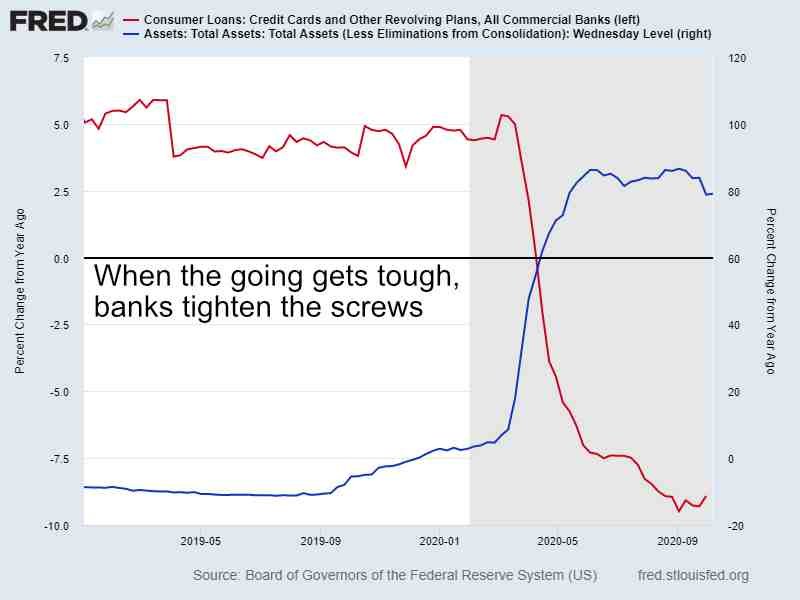

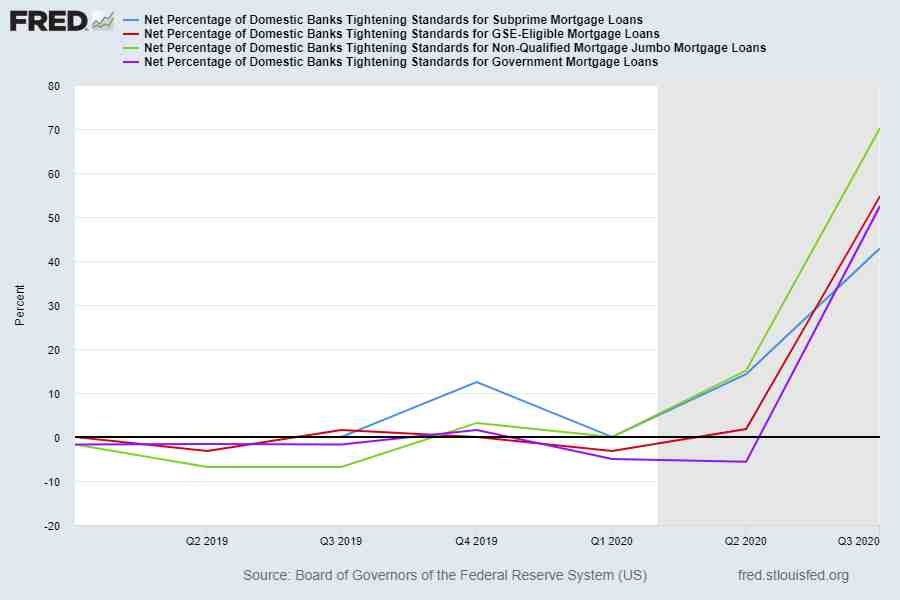

The carnival bakers at the Federal Reserve, which includes basically every district branch president including Dallas, continue to deny the obvious fact that Fed policies are causing income and wealth inequality. The Fed has been showering Wall Street with unlimited sums of cash this year. At the same time, banks continued to tighten the screws on consumers, cutting access to credit.

While mortgage interest rates remain near record lows, lenders have been reducing mortgage credit availability. Mortgage products of all varieties are seeing availability shrink as high prices and economic risk put a damper on the refinance boom and purchase party.

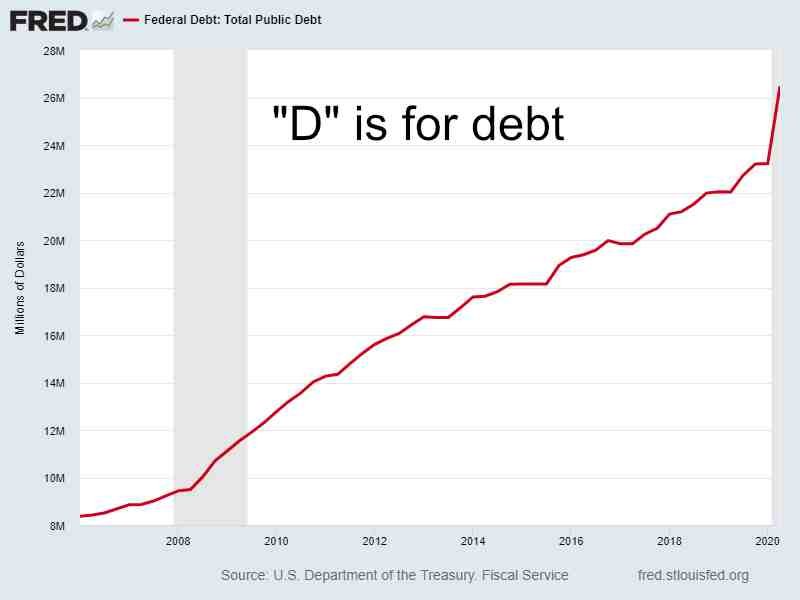

Jerome Powell continues to call on Congress to pass more stimulus because the Fed needs more product to monetize. Powell wants to keep the punch bowl full for Wall Street and investors. Ditto for the housing market. Without additional stimulus, the party for North Texas home sales comes to an end. We are already seeing this play out with local pending sales numbers now trailing the growth in actual closings. The Fed has pulled so much demand forward, growth becomes increasingly hard to produce. Or as Dr. Lacy Hunt would probably describe it, the declining marginal revenue product of debt is rearing its ugly head again. It is a safe assumption we will soon be staring at a total public debt in the United States in excess of $30 trillion. The sharp rise in the price of gold this year is not too difficult to understand in this context. Gold is often considered a hedge against central bank stupidity, and we are literally drowning in bad ideas from central bankers.

The North Texas housing market can remain afloat if the Fed keeps printing, but absent continued stimulus things get really sketchy in a hurry. If you are in the market to buy or sell a home check your politics at the front door. Watch what the Federal Reserve is doing. The Fed continues to float misdirection and cover for their destructive policies. You can either pay attention or be buried by them.

The latest quarterly review from Hoisington Investment Management offers a good summary of where we’ve been during the past 40 years and what lies ahead. Dr. Hunt specifically addresses that declining marginal revenue product of debt and the secular erosion in the U.S. economy. The tail risks ahead include a debt financed fiscal package which could produce short term inflation followed by more deflation. If the Fed’s liabilities are somehow deemed legal tender (major policy shift), that would change the ballgame and create a more serious inflationary dynamic.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment