Denton County home price inflation broke new records in May. Median home prices were up 23 percent to a record $395,000. Average prices rose 26 percent to $462,193. That was just shy of the high seen in April. With inventory still sitting near record lows the average percent of list received by home sellers jumped to 104.9 percent in May. Closed sales rose 18 percent in May, but pending sales were down 13 percent from the same time last year. Pending sales in North Texas were down 7 percent as the market ran out of affordable homes.

Sellers continue to feast on the current dynamic of record low inventories and strong demand for homes. On the flip side, buyers are just trying to catch a break in the all-out bidding wars for average homes in the Dallas-Fort Worth area. The number of homes on the market in North Texas has ticked up slightly from the recent lows, but the current inventory of roughly 12,500 homes is still woefully inadequate to keep up with current demand. For context, DFW was sitting on 40,000 available homes in May of 2019.

Many of the “experts” interviewed by the local media are still pretending this is just a garden variety supply & demand mismatch that will sort itself out. According to these agents and economists, we are dealing with transitory bottlenecks and home prices will remain elevated as the market grows into this new normal. Interestingly you don’t hear any of these supposed experts discussing what led to the massive disconnect in the current housing market. Not a peep. Nope. It’s all fundamental supply and demand and good ole economic growth, or so the narrative goes.

Nothing could be further from the truth.

The dirty little secret that agents and industry pundits don’t want to discuss is the hilarious housing bubble staring us in the face, the result of $trillions in trickle-down Fed stimulus and government largesse. Even as home prices break new records the Fed is still embarked on $120 billion per month in QE. Someone has to backstop those huge fiscal deficits, so the Fed is playing their part. Mortgage rates are still extremely low, but that doesn’t help much if you are getting outbid by cash buyers in a hyper-inflated market.

The May CPI numbers which came in hotter than expected don’t even begin to tell the story of real home price inflation. There’s nothing normal about 20 and 30 percent annual price increases for homes. While sellers are likely hoping the record low inventory levels continue, it’s just a matter of time before the market sorts it all out. This will happen whether the Federal Reserve keeps priming the pump or not.

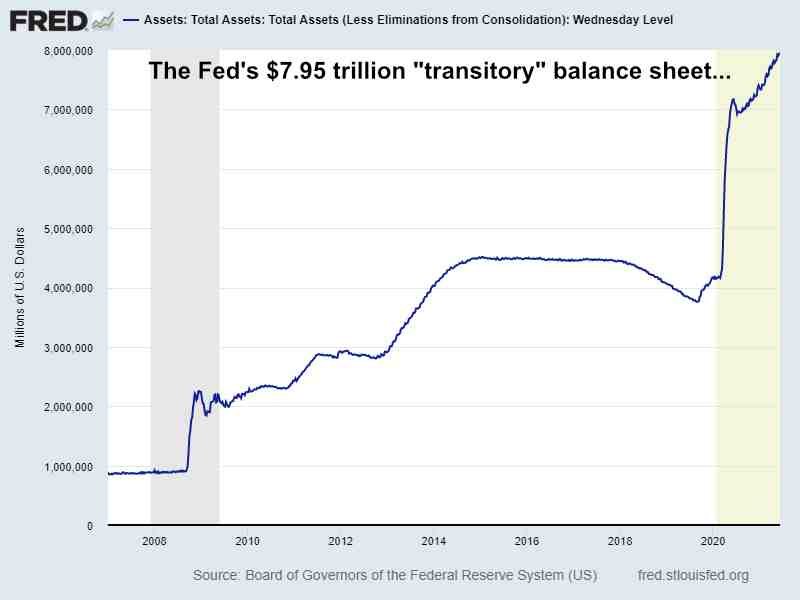

The Fed’s reverse repurchase operations eclipsed $500 billion per day this week, as the financial system plumbing keeps springing larger and larger leaks. The new record high of $7.95 trillion on the Fed balance sheet comes with a host of unintended consequences, with grossly overpriced real estate as just one of the more visible consequences.

As prospective home buyers are struggling to keep up with rampant home price inflation, average workers are really taking the brunt of the Fed’s inflationary push. As the balance sheet marches higher, the purchasing power of consumers continues to shrink. It should not be surprising that workers are demanding higher wages. Higher wages are necessary for workers who don’t want to be left behind. If you enjoy higher stock prices and real estate prices, you have no business complaining about the rising cost of avocado toast.

Jerome Powell is still sticking to the transitory narrative on inflation despite the mountain of evidence in the housing market to the contrary. It would be ironic if the Fed actually crashed the housing market again just to prove their point. Will it be the Big Short 2.0? Jerome is running out of time if he wants to tame the inflationary beast.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment