Jerome Powel and the Federal Reserve are creating another massive housing bubble. The bubble inflated even more in June as the Fed continued with $120 billion per month in asset purchases and the balance sheet hitting $8.1 trillion. The Fed’s continued purchases ($40 billion per month) in the mortgage-backed securities market are utterly baffling considering the double-digit housing inflation numbers that keep piling up. So why is the Fed fanning the flames of asset inflation? Here’s the primary reason…

Lifestyles of the rich and famous

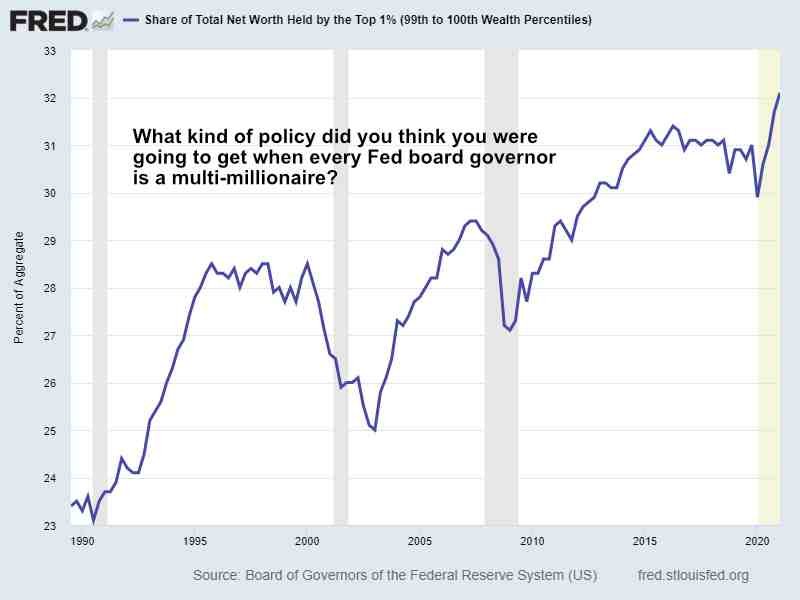

Fed officials, most whom are millionaires themselves, are smart enough to understand their trickle-down monetary stimulus isn’t getting homeless people off the street. They are aware that $trillions in trickle-down liquidity poured through a corrupt banking system is a poor mechanism for building a strong economy which improves the prospects of both labor and capital in a balanced manner. Unfortunately the Fed’s primary focus is always on capital (aka the monied class, asset holders). The endless PR about full employment and stable prices is just a convenient distraction for the public. If you really think the Fed is concerned about climate change, you haven’t been paying attention.

The Fed’s structure and massive public relations department is the reason you have Robert Kaplan, our Dallas non-voting member in the FOMC picture, continuing to pontificate about out-of-control housing inflation while Jerome and company pour gasoline on a burning building. It’s all a show enabling Jerome to line the pockets of Blackrock and his Wall Street brethren as millions of Americans get priced out of the housing market while Fed officials talk about “transitory” inflation.

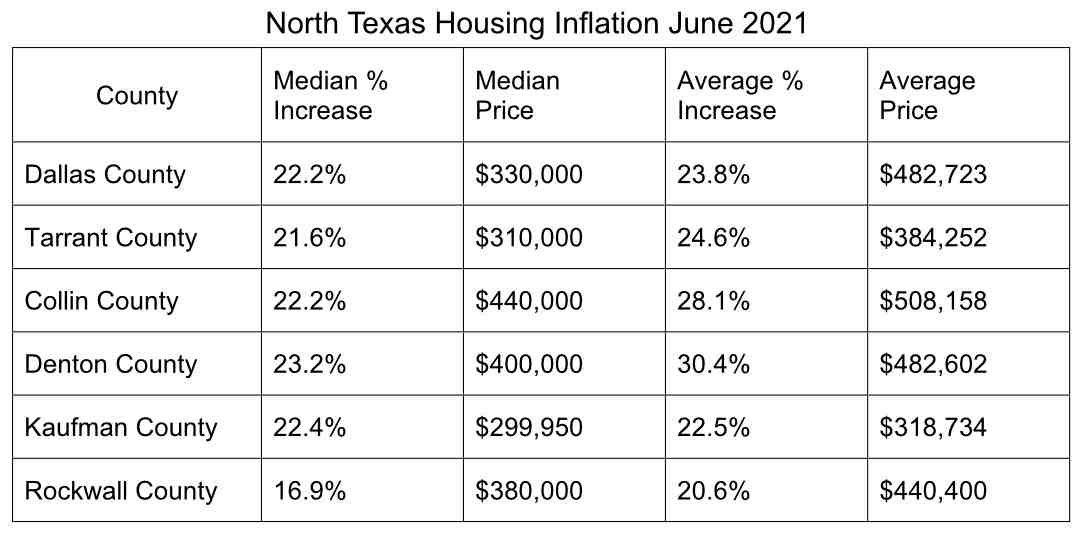

What took place in the North Texas housing market in June was absolutely astounding. We’ve never seen home price inflation like this in the Lone Star state, ever. Home prices in the Dallas-Fort Worth area continued to hit new record highs and the bidding wars for average single-family homes were stronger than ever.

Imagine you are a young couple trying to buy your first home, and you are competing against 60 other offers which are all over list price, some as much as 30 percent over list price. That’s what has been happening in the North Texas housing market the past few weeks. Reckless behavior, offers completely detached from reality and a general FOMO (fear of missing out) have caused many buyers to lose their heads. Some will also lose a lot of their equity when this all washes out.

That’s the nature of a bubble. Everyone is ready to pile on while it’s inflating, but the inevitable bursting leaves a big mess.

Median and average home prices in North Texas were up 22% and 26% in June compared to a year ago. The new median record of $339,615 and average price of $418,585. Those numbers are nothing compared to what is happening in some local submarkets. Here’s a look at the year-over-year gains in various North Texas counties for the month of June.

Even with the slight uptick in number of homes for sale, Denton County Texas is still sitting on less than a month of inventory. This helped push average price up 30.4 percent in June to another record high. The average price of a resale home in Denton County was up 32 percent last month. Wow!

Rental inflation is also hot. For the first week of July the average lease price of a single-family home in Denton County was about 12 percent higher than a year ago. That’s an increase of about $250 in the monthly rent to a little over $2300. This would be for a basic 3 bedroom 2 bath home.

Home prices are at all time highs. Stocks are at all time highs and the Fed is still pretending that inflation is “transitory”.

With the latest CPI numbers coming in hotter than expected for June, the purchasing power of U.S. consumers took another nosedive. Inflation (or at least the rate of inflation) may be transitory, but the continued loss of purchasing power is not.

It should be obvious by now that Fed officials will say just about anything to distract the masses so they can continue building their wealth transfer machine. A typical FOMC press conference is now more like stand-up comedy hour where Fed officials refuse to accept any culpability for their actions. The last few decades have been an absolute train wreck for the middle class, and particularly the working poor. The Covid bailouts were more of the same.

Just in case you were wondering who the Fed’s real constituents really are…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Staggering. I think we’ll be dealing with the fallout from this bubble bursting for years to come. Great local statistics, Aaron. Keep it up.