Demand destruction continues to hit the Denton County housing market. The Federal Reserve’s housing reset and tighter policy led to a 28 percent slide in home sales in November. Pending contracts for homes were down 24 percent from the same time a year ago. In reality sales numbers are softer than official estimates. We still have another 6 months or so before we’ll see more accurate comparisons on sales totals with new construction sales consistently in the MLS.

According to the Mortgage Bankers Association mortgage purchase applications are still running about 40 percent lower than this time last year. The drop from seven percent mortgage rates to six percent mortgage rates has barely made a dent in buyers’ demand for homes. The problem is that home prices are still way above the pre-pandemic trend and consumers’ discretionary income is falling.

Home builders have continued to report sharply declining contracts and orders during the second half of the year. Cancellation rates for builders remain high because the monthly payment are still giving buyers sticker shock. Demand destruction is hitting the housing sector across the pricing spectrum. Luxury home builder Toll Brothers saw net sales order plunge by 60 percent in the latest quarter ending in October. High net worth buyers are walking away from deposits on more of those million dollar homes. Toll’s quarterly cancellations as a percentage of signed contracts for the quarter surged from 4.6 percent last year to 20.8 percent.

Lennar homes, one of the country’s largest home builders, is also finding the market more challenging. While shelling out roughly a $billion on share repurchases in fiscal 2022 (update pending with this week’s earnings release) Lennar has also struggled of late. Bloomberg reported that Lennar is marketing 5000 homes to investor landlords now that buyer demand has softened. After spending copious amounts of capital padding executive compensation with buybacks, it’s rather amusing to see Lennar give first-time home buyers a giant middle finger by pitching discounted homes to investors. For what it’s worth, Lennar is also thumbing their nose at Realtors here in the local market with extremely stingy commission co-ops. When most builders have responded by a return to normal market incentives, Lennar has chosen the “screw you” approach to agents. We’ll see how that works out.

North Texas home prices continue their reset lower. Nominal prices have bounced around a bit the past few months, but median price per square foot for the DFW market posted their fifth consecutive monthly decline. Median prices in the Dallas-Fort Worth area fell to $365,000 in November. They peaked at $400,000 in May and July. Median home prices in Denton County fell to $450,000 in November, down from the peak of $500,000 in May. Median price per square foot in Denton County has declined for six consecutive months.

The demand destruction is visible in all facets of the market. Median and average percent of list price continue to nosedive. Average percent of list price in Denton County has fallen for seven consecutive months, down to 94.8 percent of list in November. Average days on market jumped to 39 days in November. Available inventory probably hit its high for the year in mid November. The past few weeks have seen inventory level off or drop slightly with typical year-end promotion and demand.

We are only a month or so away from the normal seasonal rebound and inventory build which typically starts in January. It will be interesting to see how much inventory hits the market in the first quarter of 2023. We already know home builders are sitting on huge backlog. I have also seen a number of investors trying to unload homes in the past few months. I expect to see more sellers in the first half of 2023. There were some who pulled their listings after unsuccessful attempts this summer.

Large institutional landlords are not immune to the recent downturn. American Homes 4 Rent, one of the country’s largest landlords, has been selling some of it’s inventory in Denton County. Big real estate investment trusts like Blackstone and Starwood have gated investor withdrawals on their funds to prevent a tsunami of redemptions. It remains to be seen whether big REITs will be forced to sell assets (aka homes) to fund the recent surge in redemptions.

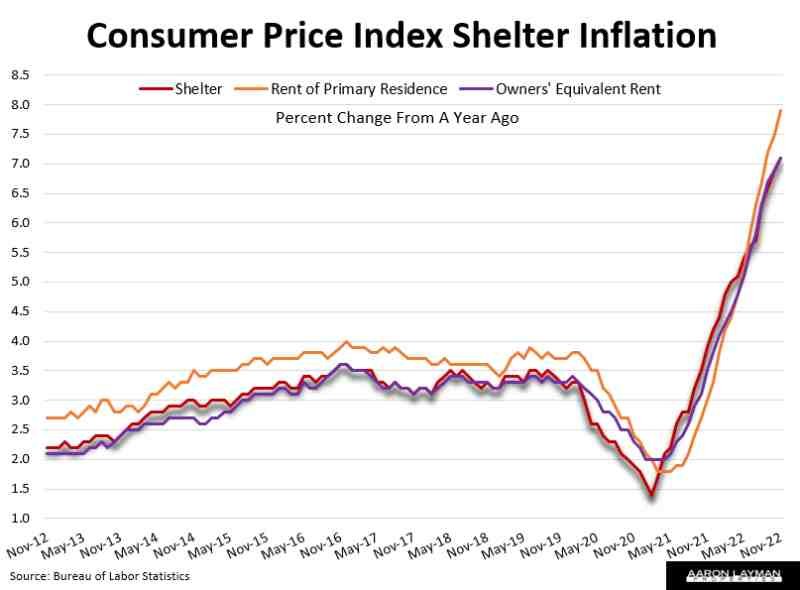

There are a lot of moving parts in terms of inflation and the economy. The November CPI print came in slightly softer than expected. Year-over-year headline inflation posted at 7.1 percent in November. Housing inflation is finally cooling, but the CPI measures of shelter inflation posted their highest readings of the cycle. When this lagged indictor of housing inflation starts to fall, a lot of the demand destruction from the Fed will already be baked into the economy.

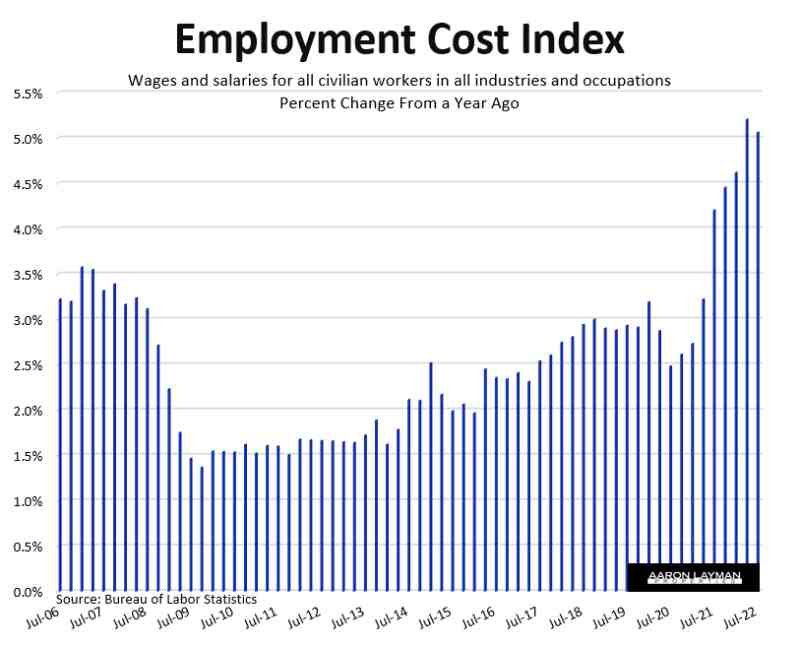

There is still the issue of embedded wage-price inflation that will cause the Federal Reserve headaches for months (if not years) to come. There are plenty of market participants hoping for a Fed pivot, but an end to rate increases is not the same as rate reductions. Many market participants apparently fail to grasp this reality. The latest numbers for wages show inflation still running in the 5-6 percent range, much higher than the Fed would like to see.

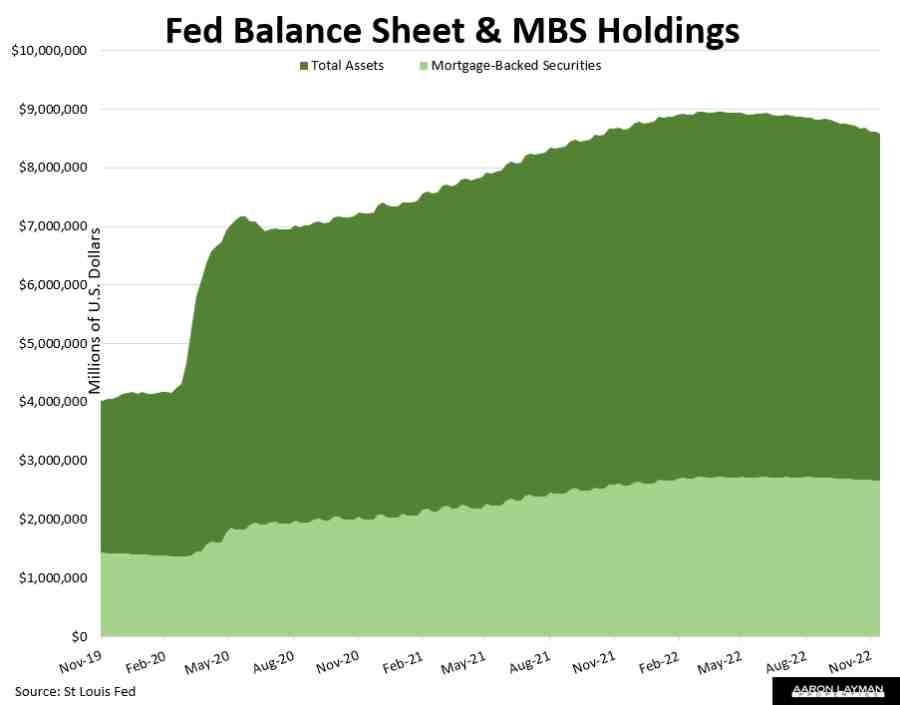

To put it another way, the Federal Reserve still has a year or more of demand destruction in its playbook. Remember that massive balance sheet, the one they expanded to nearly $9 trillion? The Fed is less than a quarter of the way to shrinking that balance sheet toward their goal. That means more liquidity will be exiting the market in 2023.

Six percent mortgage rates are better than seven percent rates. Is that enough to stem the downturn in housing demand? Not according to the market. With prices still inflated compared to historical fundamentals, the current housing market correction still has more gaps to fill.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment