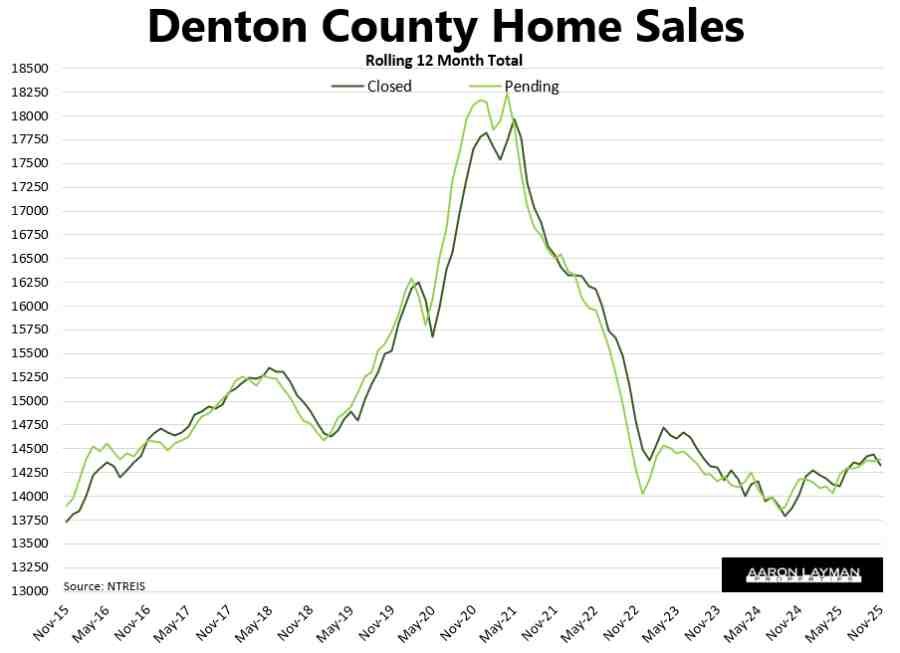

The North Texas housing market correction continues to cause more pain. Median home prices across Denton County collapsed 9.2 percent year-over-year in November. Average prices are down 8.7 percent from last year. Closed sales were down 12 percent from a year ago. With the sharp drop in prices, pending contracts managed a 3 percent increase. As we say in the business, “Price cures all defects”. That’s certainly true in today’s market.

Sellers Still in Denial

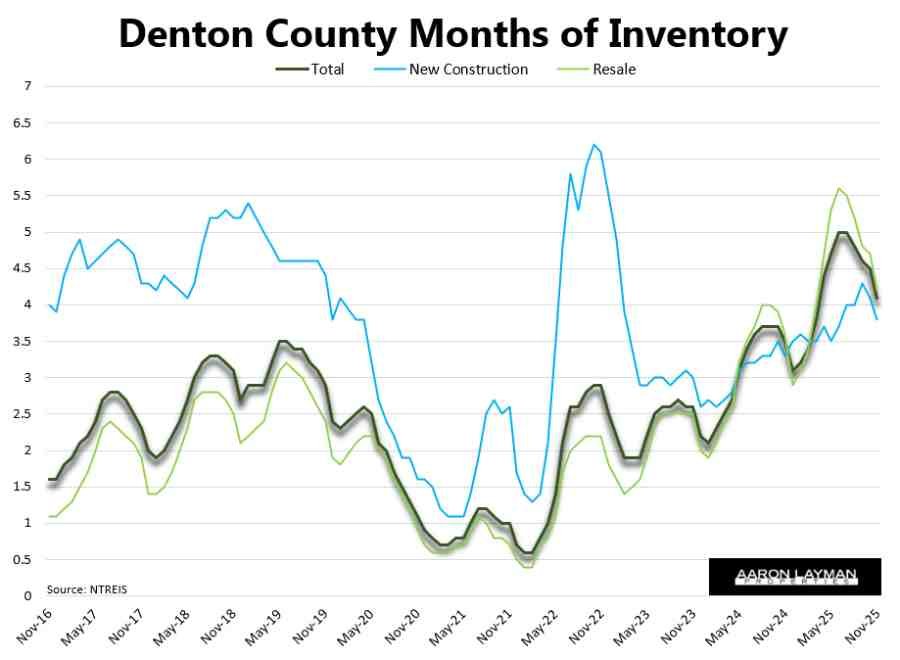

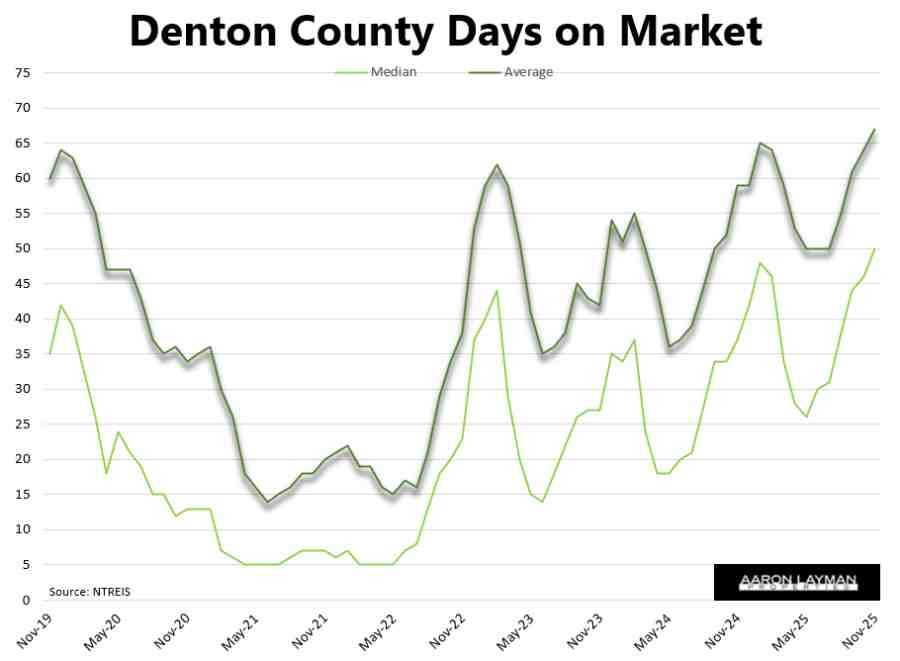

Many prospective sellers were getting their wings clipped this year. We can see this in the cancelled and expired listings. Those are up 37 percent from last year. When the fishing expeditions and over-hyped marketing from brokerages fails, more sellers are pulling the homes from the market or just renting them out. For homes that are selling, it’s taking an average of over two months (and likely several price reductions) to find that buyer. It’s the slowest market we’ve seen since 2012 in terms of days on market.

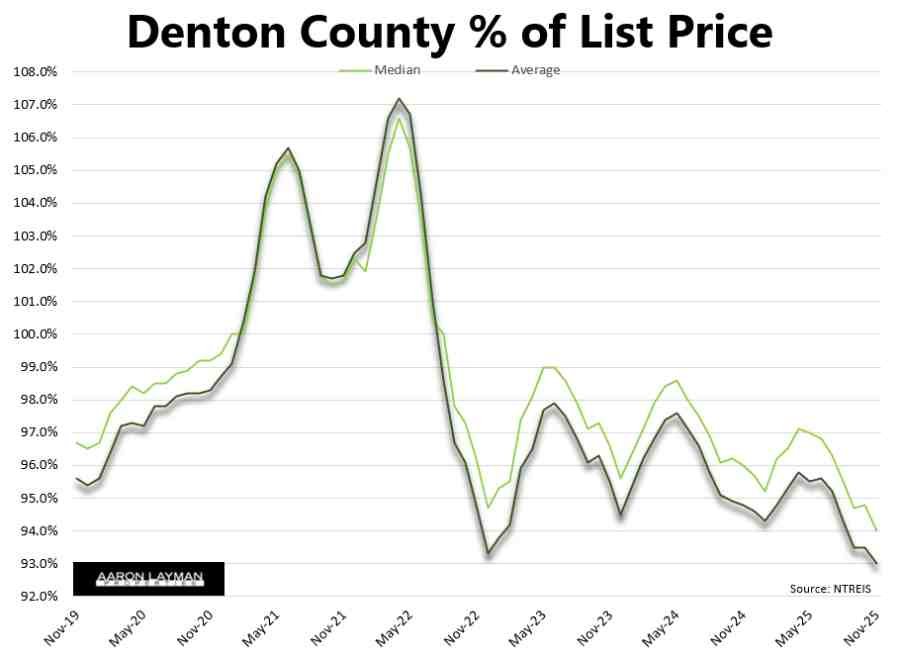

Average percent of list price received in Denton County was down to 92.6 percent. That’s the lowest figure we’ve seen since 2011. It’s truly incredible to think that average percent of list climbed to 108.5 percent during the Covid bubble peak of 2022. That was a truly wild ride through housing market insanity. Too much stimulus and artificially low interest rates have turned the housing market into a fine mess.

Bountiful Harvest of Consequences

What we’re experiencing now is the bountiful harvest of consequences. All of those short-sighted policy errors and stimulus measures have run their course, and now the bills are coming due. Homes are still expensive by most measures, and inflation is eating away at consumers’ purchasing power. All of the things you need (think homes, cars, healthcare, insurance) are much more expensive. At the same time, many discretionary items are relatively cheap. It is a K-shaped economy which has benefited asset owners and wealthy Americans. The bottom 90 percent of the U.S. population is getting buried by stagflation.

Michael Green penned a rather interesting series of posts on this K-shaped economy and the real cost of participation in today’s economy where everything is expensive and median wages haven’t kept pace with inflation. Green carefully details how broken, outdated benchmarks are seriously understating the true cost of living in America. You can argue with his calculations, but he’s spot on with the general themes in his series.

“For the middle class, rising home prices are not “Wealth Accumulation.” They are Asset Price Inflation. We have confused the capitalized cost of future rent with an asset. When housing prices triple relative to wages, we haven’t made homeowners rich; we have made non-owners poor. We pulled up the ladder and called it “Net Worth.””

He’s right, and this is why I have been consistently warning about the financialization of U.S. housing. Policy choices have consequences. Politicians just generally ignore them hoping the next person down the line will take the blame.

Relief for Renters

If housing market bubble deflation has you down, there is a bright spot. Rents for local homes have continued to soften. The latest report from Apartment List shows rents in Denton Texas are down 6 percent from this time last year and down 2.9 percent for the month of November. I have seen a number of move-in specials on apartments if you are looking to get in by the end of the year. Apartment rents are down across the DFW area, but the declines have been modest for most submarkets.

Single-family rents in Denton County are still relatively flat compared to last year. Rents for detached homes have been trending sideways for the past two years.

Builders Piling on the Incentives

With the local housing market still largely frozen, builders have continued to pile on the incentives. The improvement in pending contracts in November was driven by that motivation from builders. Lower prices and big incentives have been necessary to keep the pipeline of new homes moving.

Median and average prices for new homes are down 15.3 percent and 13.9 percent respectively for Denton County. That’s the smell of motivation! This is also what’s causing severe indigestion for many existing sellers who are watching builders steal their customers. In a soft market the agnostic seller has a much better chance to make it to the closing table. Builders are the professional sellers, so they are throwing everything and the kitchen sink in to make deals work.

Disappearing New Home Premium

Another interesting dynamic in the current market is the disappearance of the new home premium. It used to be that a new home might cost you a $100,000 more than a comparable existing home. Not anymore. New homes are now dramatically cheaper than existing resale homes. Well, at least on paper.

What we’re really experiencing is the new home premium shifting to a “real estate” premium. Lots for new homes have continued to shrink across the DFW area. This is particularly true when we are talking about the heart of the market where most of the affordable inventory is selling.

If you want a useable back yard, you are still going to pay a premium. A nice new home on a quarter acre lot is now a luxury item for most families, and probably only available in exurb areas out of the city job centers. With the dramatic decline in new home prices, one might get the impression that new homes are now cheap. That’s not necessarily the case, particularly when you are factoring in quality of construction and the size of the actual dirt. Everything is relative.

Fed Cuts Another 25 Basis Points

The Federal Reserve cut rates another 25 basis points at the December meeting. That makes three cuts for 2025. What’s interesting to note is that real bond yields on the 10-year Treasury have barely noticed.

The Federal Reserve also announced it will be buying $40 billion per month in T-bills to shore up the plumbing in the financial system. These reserve management purchases are not really QE, but more to do with internal plumbing and the now bloated size of the Fed’s balance sheet.

What’s important with this move is the dovish tilt from the Fed toward growth. This comes at a time when the markets are near all-time highs and inflation is still a huge problem. To translate in Layman’s terms: This won’t help bring real interest rates down, not when the current administration is still running things hot with a massive fiscal deficit. The U.S. government blew a $1.8 trillion deficit hole in 2025. The first two months of fiscal 2026 show more of the same. If you thought Trump was going to bring fiscal sanity to the U.S. government, you haven’t been paying attention.

If you are in the market to buy or sell a home, be careful out there. There are plenty of people hoping for greener pastures in 2026, but we have a lot of work to be done before there can be a sustainable recovery.

If lower rates do come knocking at your door, you might not like the company they bring with them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment