U.S. mortgage rates breached the critical 5 percent level today. Prepared remarks from FOMC dove Lael Brainard spooked the markets into a tailspin sending yields on the 10-year Treasury above 2.56 percent. Average mortgage interest rates quoted from Mortgage News Daily spiked to 5.02 percent. This is the first time rates have been this high since 2018. You may remember that the fourth quarter of 2018 also saw the stock market and real estate markets come unglued before the Fed stepped in to intervene.

Unfortunately for real estate bulls, this time is different. Instead of halting the slide in overly-inflated asset prices the Fed is actively encouraging it. They really have no choice with inflation spiraling out of control. This is a mess of their own making. After blowing bubbles in bonds, equities and real estate the Fed finds itself backed into a corner… again. The FOMC is under the the gun to tame the inflationary monster they unleashed in the U.S. economy with $trillions of inflationary stimulus during Covid. If inflation is still raging come November there will be a big house cleaning in DC. This inconvenient fact is certainly not lost on either Joe or the Fed.

Brainard’s hawkish comments spooked the iShares Home Construction Index ($ITB) to a fresh year-to-date low. Shares of builders and real estate brokerages got pounded today as mortgage rates spiked above 5 percent for the first time in years.

Brainard’s prepared remarks were quite a wake-up call.

“It is of paramount importance to get inflation down. Accordingly, the Committee will continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting. Given that the recovery has been considerably stronger and faster than in the previous cycle, I expect the balance sheet to shrink considerably more rapidly than in the previous recovery, with significantly larger caps and a much shorter period to phase in the maximum caps compared with 2017–19.

The reduction in the balance sheet will contribute to monetary policy tightening over and above the expected increases in the policy rate reflected in market pricing and the Committee’s Summary of Economic Projections. I expect the combined effect of rate increases and balance sheet reduction to bring the stance of policy to a more neutral position later this year, with the full extent of additional tightening over time dependent on how the outlook for inflation and employment evolves.

Our communications have resulted in broad market expectations for an expeditious increase in the policy rate toward a neutral level and a more rapid reduction in the balance sheet compared with 2017–19.”

Fed Official Admits the Obvious

In amusing fashion Brainard also spilled the beans on how inflation is much worse for working Americans and the working poor.

“Since lower-income households represent a relatively smaller share of overall expenditure, the inflation associated with their consumption baskets is underrepresented in the official consumer price indexes…recent research has begun to assess variation in the ways different households experience inflation…To take an extreme example, caviar and canned tuna are both in the same elementary index. The demand and supply dynamics for those products are likely quite different, meaning that their relative price dynamics are poorly described by a single index.”

It is pure comedy to hear an FOMC official, particularly a dovish member like Brainard, admit what anyone with a brain has known for centuries. Inflation is a tax that hits the poor and middle class much harder than it impacts wealthier Americans. For the top 10 percent, and most certainly for the top 1 percent, the recent bout of inflation has been an absolute gift. Wealthy Americans love having the value of their assets artificially inflated. As long as the food delivery doesn’t get interrupted why would they complain?

As Forbes writer John Wake has noted, real estate investors are making a mint in this Fed-juiced housing market. Wealthy Americans and mega Wall Street landlords have been gobbling up affordable single-family homes across the country to cash in on this inflation. The real estate industry has been loathe to discuss why home inventory is so thin in this post-Covid environment. The truth is ugly, and not exactly conducive to the fake narrative sold by many agents and economists.

Building more homes only gets you so far in terms of housing market normalization. To really level the playing field for working Americans who want to participate in the American dream of homeownership, we need better housing policy. Getting rid of the perverse tax breaks and incentives for real estate investors would be a great way to improve housing inventory levels. Tax breaks for real estate speculators and wealthy investors are contrary to good housing policy. Tax breaks for billionaire Wall Street landlords make wealth inequality even worse and facilitate the financialization of housing.

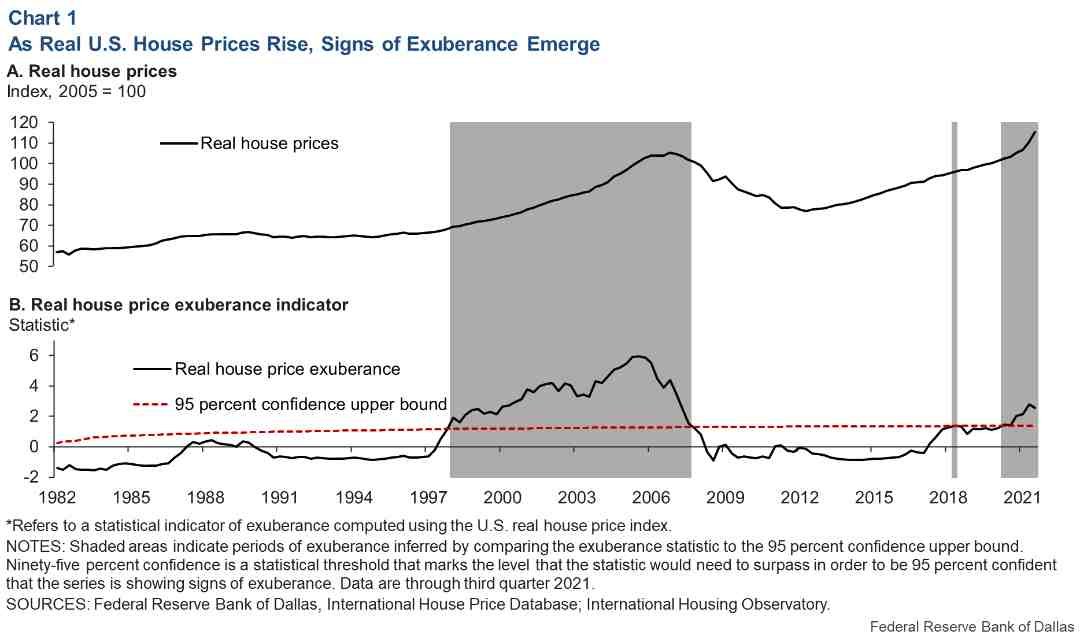

The Fed’s own research shows officials knew the U.S. housing market was overheating for 6 consecutive quarters while they stood by and watched. This revelation from the Dallas Fed is particularly entertaining considering Jerome Powell spent most of 2021 pretending that inflation was transitory while home prices and rents continued to melt up.

“Since the beginning of 2020, the price-to-rent ratio has soared beyond what observed fundamentals alone can explain…The gap between the actual price-to-rent ratio and its fundamental-based level in the U.S. has grown rapidly during the pandemic—comparable to the run-up of the last housing boom—and started showing signs of exuberance in 2021. The exuberance statistic confirms that recent increases are far from ordinary.”

Things are getting interesting for the real estate market. 2018 is not exactly a great comparison to our current environment. Inflation was still low then. You have to go back to the 90’s or the 1970’s to get anything similar to our current inflationary backdrop. Local inventory is still ridiculously low, but the winds of change are blowing.

Stay tuned.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment