Home inventory in Denton County continues to pile up as the North Texas housing market stalls. The post-pandemic housing bubble is now popping under the pressure of dramatically higher mortgage rates and a lack of affordability.

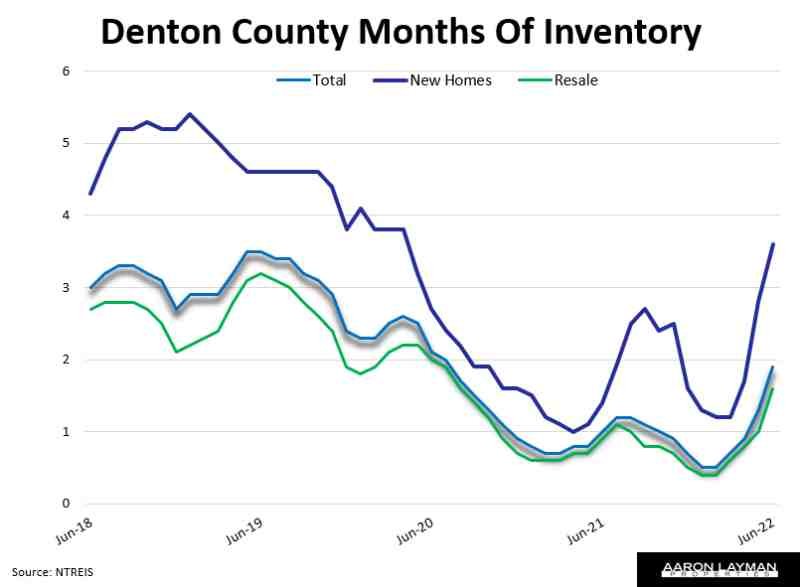

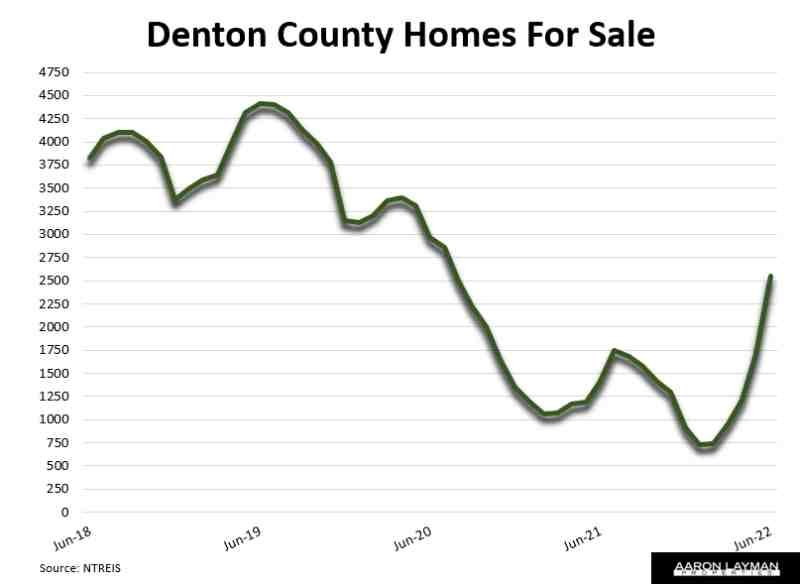

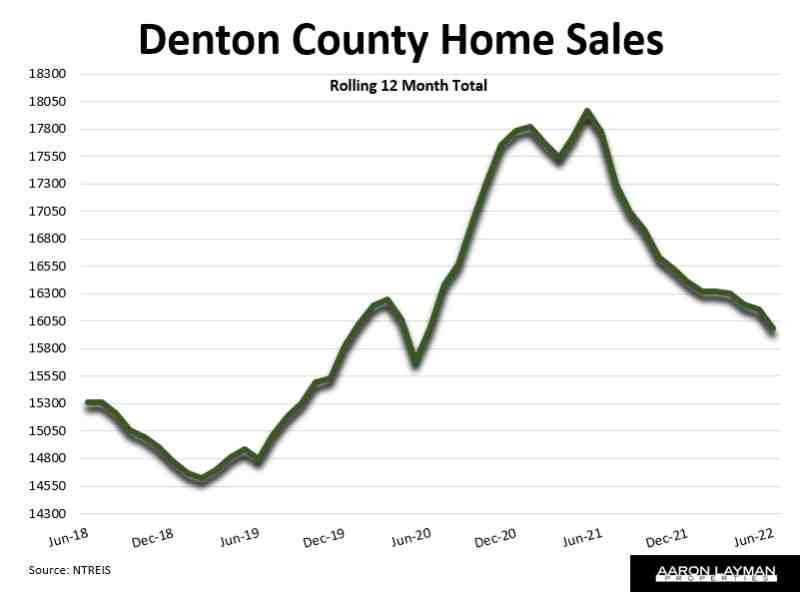

NTREIS figures show Denton County home sales fell 10 percent from June of last year. Pending sales declined roughly 8 percent year-over-year. The inventory of homes available for sale is up 80 percent from a year ago. With the decline in sales, months of inventory has spiked 90 percent from a year ago. Months of inventory for new construction is up a whopping 157 percent. Median and average home prices in Denton County both fell from their May peak. Prices could fall a lot more if the inventory keeps piling up at the current rate.

It’s sad reflection on the industry that most of the real estate “experts” agents, and economists were parroting fake news about a massive housing shortage earlier this year. Anyone with a brain could tell the true culprit behind spiraling home prices and low inventory was the artificial suppression of interest rates and a massive liquidity injection into the markets. The Federal Reserve has admitted the real estate boom was fueled by cheap debt, not a lack of supply.

Earlier in the year we saw a professional economist babbling on 60 Minutes about a fake housing shortage while U.S. home construction was doing this…

A few months later we had the opportunity to see the truth behind the industry’s nonsensical claims as mortgage rates hit 6 percent and the liquidity-fueled housing bubble finally popped. I’m offering up Prosper Texas as the poster child for what happens when the the real estate industry’s fake narrative of a housing shortage is revealed as a ridiculous work of fiction. With prices skyrocketing to ridiculously unsustainable levels, most North Texas submarkets are experiencing a serious mean reversion. New home inventory in Prosper (months of inventory) is now the highest since the Great Recession back in 2007. Median prices in Prosper collapsed over $125,000 last month as the May blow-off top came crashing back down to reality.

Markets across North Texas are finally getting a dose of reality in the form of higher rates and a Federal Reserve which has finally stopped juicing asset prices. The government (and specifically the Federal Reserve) encouraged this housing bubble. Now they have to break it. Unless they want riots in the streets with double-digit inflation impoverishing millions of Americans they have no choice. Inflation is a killer for the economy, and Jerome knows it.

Across Denton County home sellers and agents are slowing realizing the Fed is no longer fueling asset price inflation. They are doing the opposite. The Fed is now doing whatever it can to tame asset inflation short of destroying the economy and the labor market. They may blow it all up. If history is any guide, the odds are good that a soft landing is not going to be the end result.

That won’t stop the sell-side real estate and mortgage industries from selling a good story. Earlier this week we saw how financial media and industry puppets will run with a fake story regardless of the circumstances. We saw supposedly serious financial news sources regurgitating headlines this week about a fall in mortgage rates to 5.3 percent. The only problem was that the headlines were completely untrue. We ended the week with rates at 5.84 percent, not the lower rates you saw in many major media outlets.

When the Freddie Mac index printed on Thursday morning showing a rate of 5.3 percent, media hacks ran with the story. They failed to mention the Freddie Mac survey data point they were referencing is a lagging indicator of rates, and particularly misleading in a volatile market like we have this year. The media news spin was so bad, Mortgage News Daily even addressed it directly.

“This week’s misleading headlines are invariably a result of Freddie Mac’s weekly mortgage rate survey. This is the longest-running and one of the most highly regarded records of interest rate movement over time. A majority of news organizations rely on it as the primary source for their once-a-week coverage of rates.

During more normal times, this strategy is good enough. The mainstream consumer of financial news doesn’t particularly need a new update on rates every day (unless they’re home shopping). And Freddie’s data does a great job of capturing the broad, long-term trends in rates.

Unfortunately, it does a terrible job of capturing rate changes when bonds are experiencing high volatility, especially if that volatility occurs during the last 3 days of the week.”

If you are in the market to buy or sell a home, this is critical information. We are in a volatile market with a housing correction that is only starting. Instead of reporting up-to-date factual information, you have industry players trying to pump more sales. As many sellers are figuring out, misjudging the market can be a costly mistake. Price cuts on top of price cuts are a bad formula for selling a home. You lose both time and equity when you miss the mark in a market turn.

Prospective home buyers need to look at the current inventory situation and see the writing on the wall. Forget the nonsense spouted by many agents and the sell-side industry. If the market is turning in your favor, time is friend. There is no need to rush. If you don’t need a home right now, it could be in your best interest to let the Fed do its job and cure the demand overshoot in the housing market. As inventory continues to build, prices should come down in response.

We are already seeing this dynamic play out in the new home market. Denton County new home communities which were selling off of customer waiting lists and huge demand earlier in the year are now offering big commission bonuses to Realtors and generous closing cost incentives for buyers. As many of the under-construction inventory approaches completion and we get back to something resembling a normal market, price cuts will likely follow. Builders will dabble incentive carrots before they actually lower prices. The market will eventually force their hand as long as the Fed follows through on their current path of policy normalization.

Home prices are simply too high to be sustainable. No amount of whining or squealing by agents and industry apologists will change that. The June release of consumer price inflation (CPI) showed a 9.1% year-over-year increase. That was the highest reading so far this year. The Bureau of Labor Statistics measures of housing inflation ticked up slightly, but they’re still far below actual housing inflation.

This is the challenge facing the Powell Fed. They let housing costs boil over for at least a year longer than they should have. Now the bill is coming due. We still have a good 6 months or so of highly elevated housing inflation built in to the official government statistics which are a lagging indicator. The Fed is going to be forced to tame home prices by any means necessary, even if it drives the U.S. economy into an recession. Remember this the next time you hear some Federal Reserve talking head talking about the Fed mandates of stable prices and full employment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment