The Denton County housing market experienced a temporary lift in the first two months of the year. February home sales bounced from the January lows putting them 15 percent higher than the same month last year. Pending sales were up 23 percent in February across Denton County. Median and average home prices bounced slightly during the month. The available supply of homes dipped to just 1.7 months.

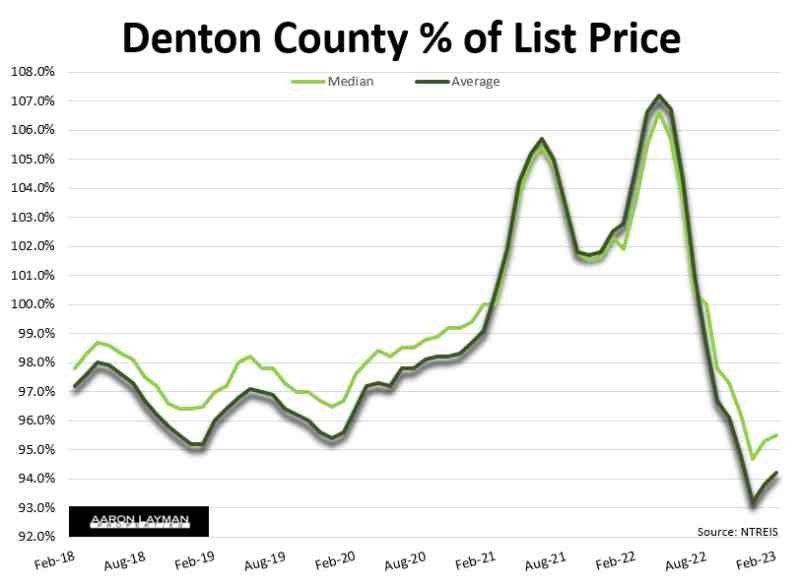

As more sellers and builders chopped prices in recent months, more buyers stepped back into the market. Percent of original list price has made marginal improvements for the past two months now. Even with the temporary bounce in activity and pricing it was still taking longer to sell a home. Average days on market for Denton County rose to 62 days in February.

The local market is still adjusting to this higher interest rate environment and increased volatility. We started off the year with loose financial conditions and a bounce in the stock market. The Powell Fed provided some additional lift by taking the foot off the break in terms of monetary policy with the first FOMC meeting of the year. That was all the excuse housing industry participants needed to begin calling a bottom in the housing market correction.

In the land of mortgage finance and real estate every day’s a great day to buy a home, or originate a loan, or write a new title policy. Many agents will regurgitate all sorts of financial nonsense if they think it will help them collect a commission faster. We saw how reckless some agents and buyers were during the height of the FOMO madness in the early part of 2022.

The February nonfarm payrolls showed that the U.S. economy added another 311,000 jobs in February. The jobs data suggests we’re still dealing with a tight labor market. The February CPI showed headline inflation at 6.0 percent. That’s still well north of the Fed’s 2 percent target. Core sticky inflation components were actually getting worse in February.

The housing market, and particularly the new home market, are still showing few signs of recession. This continues to be a major problem for the Powell Fed. It’s going to be really difficult to bring down inflation and contain it without a significant increase in unemployment. The Fed could be forced to take rates to 6 percent. That’s higher than most of the pundits in the real estate and mortgage industry are expecting. Many have been calling for Fed rate cuts to boost their transaction volumes. Bailout nation loves cheap money from the Federal Reserve Bank. After more than a decade of ZIRP (zero interest rate policy) many market participants have come to rely on continuous market intervention and interest rate suppression to maintain a comfortable living.

The problem for the local housing market continues to be the dramatic decrease in affordability caused by those years of intervention and market manipulation. While many housing industry professionals are quick to blame the recent rise in rates, they completely dismiss the artificially low interest rates and QE that fed the housing market along the way. Liquidity giveth, and liquidity can also taketh away.

Capitalism for Thee, Bailouts for Me

The implosion of Silicon Valley Bank (SVB) is yet another reminder of the cockroaches which have yet to be uncovered. Loose financial conditions and cheap money have helped many zombie companies and speculators fly under the radar over the past decade. Now we’re beginning to find out who was swimming naked.

It’s amazing how fast government officials jumped to the rescue of wealthy west coast speculators. Silicon Valley tech bros got a bailout less than 3 days after Silicon Valley Bank went under. While millions of struggling Americans are seeing food stamp benefits reduced this month, the Federal Reserve, Treasury and FDIC chose to bail out the California governor, Silicon Valley speculators, crypto mavens and uninsured SVB depositors who ignored basic risk management procedures. Wheee!

What’s going unnoticed is that the Fed/Treasury/FDIC trio just introduced more systemic risk into the financial system. Silicon Valley Bank’s management was apparently asleep at the wheel. SVB depositors were not innocent bystanders. They likely knew about the FDIC $250k insured threshold. Venture capital apologists and morons continue to suggest SVB wasn’t making bad loans. What else do you call it when SVB depositors and clients received generous lines of credit on businesses with no real profits?

Silicon Valley Bank was most certainly not a boring conservative bank. The CEO was on the board of directors of the San Francisco Federal Reserve for starters. California governor Gavin Newsom has three wineries listed as SVB clients. Newsom apparently had personal accounts at SVB for years. An SVB bank president sits on the board of Newsom’s wife’s charity. Of course Newsom didn’t mention his ties to the bank when he praised the bailout.

The SVB executive management team was loaded with recycled GFC participants. CEO Greg Becker and other officers were cashing in millions stock in the days and weeks prior to the bank going under. Greg Becker lobbied for looser regulations back in 2018. In testimony to Congress Becker touted the “low risk profile of our activities” Go figure!

The media landscape is now littered with an assortment of not-so-noble lies about how the SVB bailout was not actually a bailout and no taxpayer money was used. Considering we just socialized the entire banking sector; you would think Congress would want to impose some meaningful regulations. They could start by increasing the amount banks contribute to the FDIC insurance fund. They could prohibit stock buybacks and cap executive pay. If we’re going to treat banking as a utility where every depositor is insured, then it’s probably a good time to stop rewarding bank CEO’s and management for systemic failures and outright criminal behavior which many banks have admitted to over the past several decades.

While the market tries to sort out the mess in the banking sector here’s some context on where we stand in terms of policy normalization, price distortions and the road ahead.

Quantitative tightening is still in the early stages. It’s probably a bit early to call a bottom for the housing market when the Fed hasn’t hit terminal rate yet, not if the Fed want’s to claim victory over inflation. Powell has barely made a dent in that massive bubble-blowing balance sheet which is still over $8.3 trillion.

With unemployment still sitting near a 40-year low, it looks like Powell will have to press harder on the brakes to bring down the service sector.

If you are still confused how home prices in North Texas were able to climb to such dizzying heights coming out of the pandemic, it’s really not that complicated. When you throw $trillions in stimulus at the financials system a lot of that money goes into real estate. Homes are certainly part of that equation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment