The Denton County and North Texas housing market continued to bounce in April. Median home prices were up over $40,000 from January, but still down 1.6 percent from April of last year. The ridiculous bubble from the spring of 2022 continues to make for tough year-over-year comparisons. Thin resale inventory and higher prices are still taking a toll on sales. Closed sales in Denton County were down 8 percent from a year ago, while pending contracts were 5 percent lower.

With the tighter conditions this spring average days on market fell to 51 days. Average percent of list price received by sellers edged up to 96.5 percent. The available inventory of homes remained relatively unchanged for April sitting at only 1.8 months supply. Resale inventory has been rising slightly the past few months, but new home supply has been falling rather sharply as builders capitalize on another opportunity to move a good portion of their backlog.

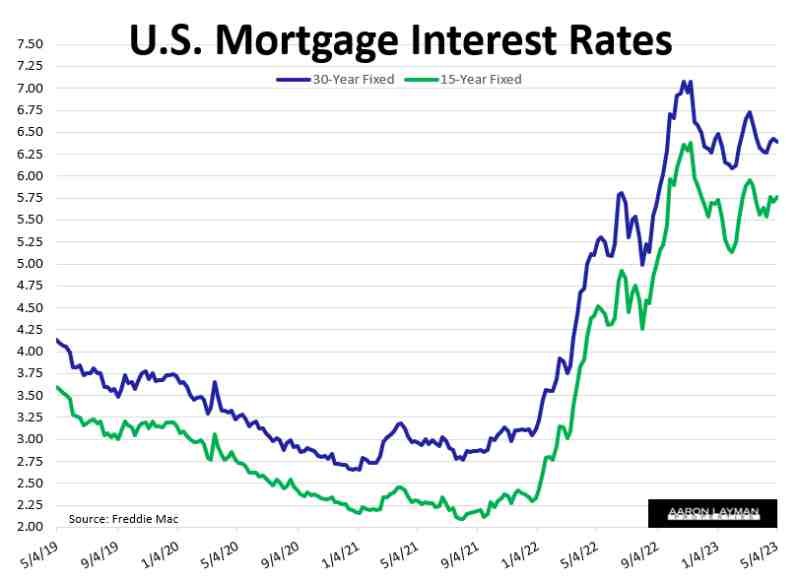

Mortgage interest rates continue to be range-bound. A 30-year fixed rate mortgage has been bouncing between 6 an 7 percent for the past few months. The Federal Reserve can’t afford to let their foot off the throat of their inflationary monster. At the same time fears of recession and more Zombie bank blowups keep hopes alive for lower rates. Many real estate industry participants are still crying for lower rates. The irony is that many will also be crying for another bailout when the next recession does actually arrive.

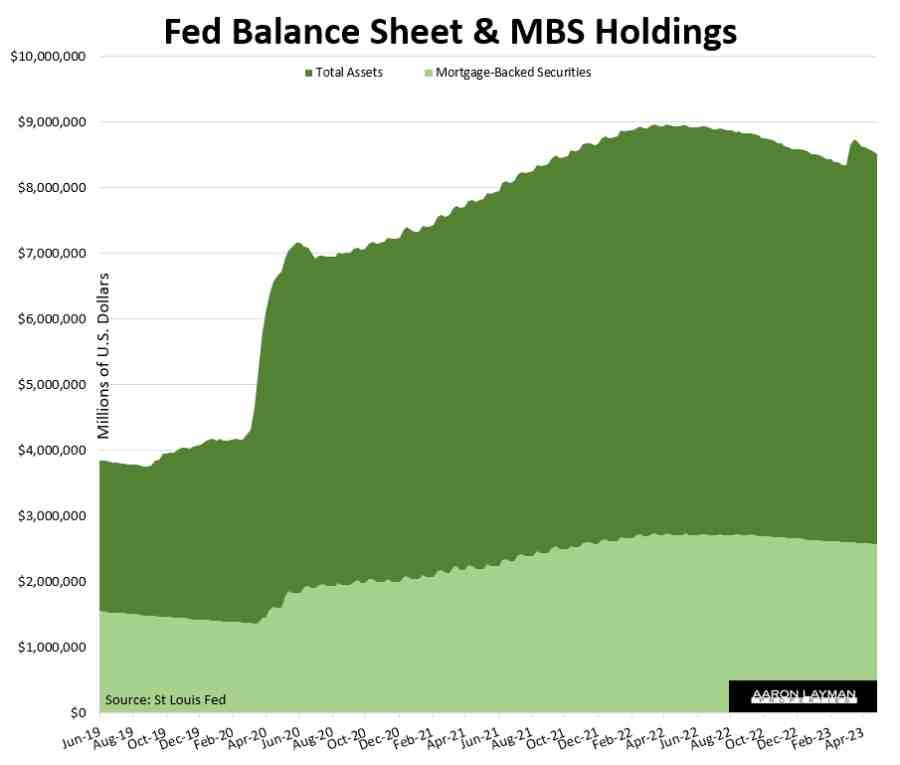

The Powell Fed has resumed quantitative tightening amid the zombie bank blowups. That means more liquidity has to exit the financial system. The pending debt ceiling negotiations and the subsequent rebalancing of Treasury accounts could cause some additional hiccups in the coming months.

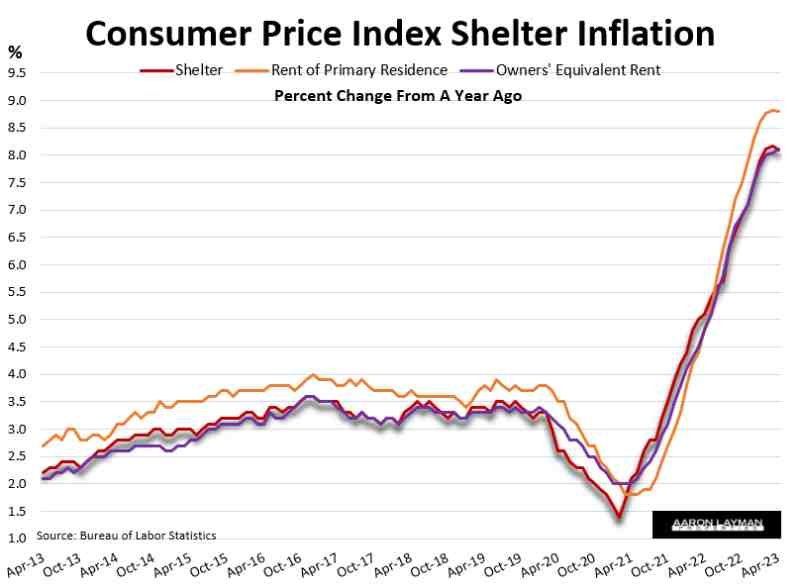

Official headline inflation for April came in just shy of 5 percent, so the Fed is making some progress in that regard. The challenge for the Fed is that core CPI remains sticky above 5 percent. Core inflation is not showing same disinflationary impulse. Rising home prices and rents don’t help the Fed’s cause. To understand what I mean, consider this. Single-family rents in Denton County were actually 5.5 percent higher year-over-year in April when adjusting for the size of homes. That’s the kind of sticky shrinkflation now embedded in the economy.

Another rate hike in June is still on the table without a meaningful weakening of the labor market. The Fed needs to see a noticeable bump in the unemployment rate and softening wage pressure to have any hope of their 2 percent inflation target. If home prices or rents continue to bounce, Jerome’s problems compound even more.

Official CPI shelter inflation is finally rolling over. While many real estate industry participants continue to talk up the prospects of lower rents, the situation on the ground is still challenging for most prospective renters. To really tame inflation, the Fed will probably need negative year-over-year rent growth, something the industry seems vehemently opposed to.

Appraisal District Overreach

You may have noticed that the appraisal district took the liberty of adjusting the market value of your home significantly higher for 2023. This has been happening all across Texas as central appraisal districts toss reality to the wind and ignore a basic requirement of the Texas tax code. Here’s what the appraisal districts are supposed to be doing according to the state comptroller:

“With few exceptions, Tax Code Section 23.01 requires taxable property to be appraised at market value as of Jan. 1. Market value is the price at which a property would transfer for cash or its equivalent under prevailing market conditions if:

- it is offered for sale in the open market with a reasonable time for the seller to find a purchaser;

- both the seller and the purchaser know of all the uses and purposes to which the property is adapted and for which it is capable of being used and of the enforceable restrictions on its use; and

- both the seller and purchaser seek to maximize their gains and neither is in a position to take advantage of the need or demand of the other.”

I have highlighted the critical section above. After protesting a property this spring it is pretty clear to me that the appraisal districts (and the software they are using) is simply extrapolating the spring 2022 housing bubble forward into 2023 as if nothing had happened. It appears many of the CAD’s algorithms and evidence are completely ignoring the fact that “prevailing market conditions” for 2023 involve a new environment where mortgage rates and the cost of borrowing are dramatically higher than they were for the first quarter of 2022.

I have no doubt that appraisal districts will be making concessions off of those inflated 2023 notice values. In the cases where they refuse to back down, I suspect the CAD’s will be looking at number of district court lawsuits this year. I reached out to the Denton Central Appraisal District a few weeks ago. A representative confirmed they had over 1000 suits against the CAD in 2022. It wouldn’t surprise me if even more wealthy and commercial property owners utilize the district court loopholes available to them in 2023.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment