Home sales are stagnating, mortgage rates are falling and job growth is now waning. What’s not to love? Today’s nonfarm payrolls report was a resounding thud with only 75,000 jobs added in May. Previous months were revised downward as well. Everywhere you look, cracks are beginning to appear in the carefully varnished edifice the Federal Reserve likes to call an economy. Maybe this is why there were 13 Federal Reserve officials hitting the airwaves this week to talk up their most favored metric of economic validation, the U.S. stock market.

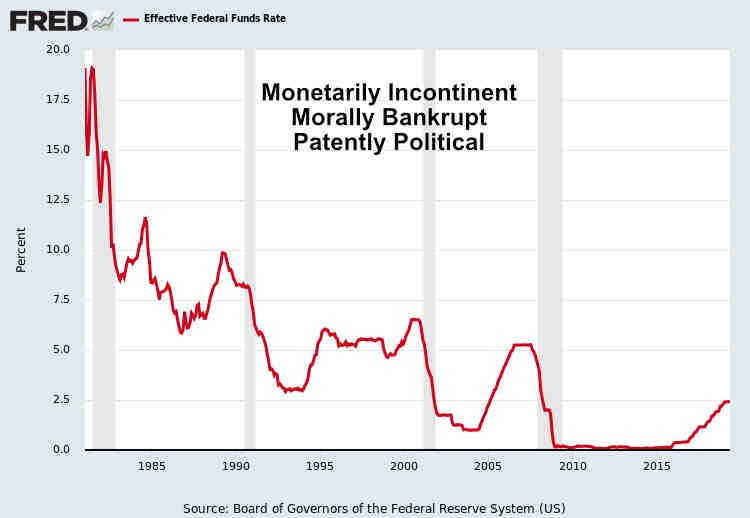

Earlier in the week we received news that mortgage purchase applications for homes have flatlined even though interest rates are well below the levels we saw last year. Things have certainly changed from November 2018, when Jerome Powell was here at the Dallas Fed telling the entire country that the economy was “in a good place”. Amazingly, those same clueless FOMC officials who told us everything was awesome just a few quarters ago are now talking about interest rate cuts and continued use of “unconventional” measures which should now be considered conventional. In Layman’s terms it appears we should not be surprised when the Federal Reserve resorts to more quantitative easing or drastic rate cuts when their ivory tower economic models are revealed to be the giant pile of scat they are.

The dramatic shift/U-turn in Fed policy during the past 6 months is not really a surprise to any one paying attention, but it is noteworthy. For all of the Federal Reserve’s vaunted ‘independence”, FOMC officials are increasingly looking like Trump’s lap dogs, which they are, because they are all serving the same master. If the only thing you value is growth at all costs, that’s what you get. Unfortunately, everyone eventually sits down to a banquet of consequences.

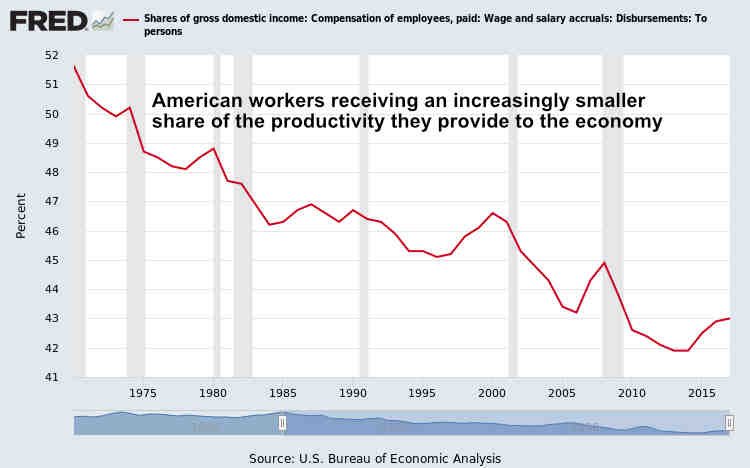

Personally, I would have no problem with the central bank constantly intervening to prop up the stock market, assuming every U.S. citizen received a share of the artificial asset gains FOMC officials seem to hold so dear. Unfortunately we are dealing with exactly the opposite. The central bank is hell-bent on facilitating massive wealth and income inequality while they run a protection racket for Wall Street crooks. Fed officials regularly opine about need for Americans to invest for their future, knowing full well that the majority of Americans don’t have enough cash to invest in the market even if they wanted to. For the Fed and their hoard of lackey economists on the take, it’s all business as usual. Everything is fabulous…as long as you are one of those insiders connected to the Fed’s liquidity spigot!

With wealth inequality near historic levels in the United States, it is not really surprising to see the law of diminishing returns manifesting in the U.S. economy. Debt is everywhere you look. It is not surprising that more and more Americans are struggling to keep up in a rigged economy that favors the few at the expense of the many. But the rigging of the economy goes even further than many Americans realize or are willing to admit. This week our own central bank, the Federal Reserve Bank of the United States, released a 104-page statement to run cover for America’s largest bank and serial felon, JPMorgan Chase. After the bank was found to be breaking the law and abusing customers for years, not only is JPMorgan’s CEO fabulously wealthy, JPM will be opening 90 new branches in new markets with the Fed’s blessing.

As we are experiencing in the housing market, the consequences of failed monetary and fiscal policy are coming home to roost. The financial predators have lined their pockets during the last decade as the Fed saw fit to bail them all out regardless of their profound transgressions. Here we are more than a decade later, and many of those same parasites are chomping at the bit to extract another pound of flesh from the carcass of the American middle class.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment