North Texas home prices continue to defy the Fed’s transitory narrative. While Jerome Powell and various FOMC officials waffle back and forth on continued stimulus, DFW homes are becoming more unaffordable. NTREIS figures for April show the median price of a DFW home jumping 17.4 percent to a record $317,000. The average price of a North Texas home hit a new record of $397,582. That was a jump of 26.8 percent from the same time a year ago. Those numbers make a mockery of Powell’s ridiculous 2 percent inflation targets over the longer term.

Home sales were still strong across the DFW area in April as buyers continued to bid home prices to the moon. FOMO (the fear of missing out) pushed the average percent of list to a record high of 101.1 percent. The supply of homes remained parked at record lows with just 1 month of available inventory.

Denton County Texas has roughly 3 weeks of supply. This helped push home prices in the area to nosebleed territory. The median price of a home shot up 26 percent to $395,000 while the average price of a Denton County home rocketed 28 percent to $464,020. Looking at the price per square foot, things were just as crazy. Median and average prices up 20 percent and 21 percent respectively. Denton County home buyers are throwing out offers for homes like they are Halloween candy.

This begs the question of whether there will be some goblins visiting the local housing market once the Federal Reserve puts the brakes on $120 billion per month in asset purchases. Mortgage interest rates have cooled off recently after a sharp rise in the first quarter of the year. Signs of inflationary pressure in the economy continue to build while the Fed waffles about removing unprecedented stimulus to support markets. Meanwhile the price of lumber has shot up 377 percent in a single year to a record $1635 per 1000 board feet. Manheim’s Used Vehicle Value Index is up a whopping 54 percent from April of last year.

Business owners continue to worry about those inflationary pressures while they whine about a shortage of qualified labor. Other pundits claim the government’s unemployment support is keeping low wage workers from coming back to their dead-end service jobs. Heaven forbid Johnny or Alice hold out for $15 per hour while Mr. Bezos is building a $500 million yacht. In truth there’s no shortage of labor at all. If you pay people a living wage (something above basic unemployment assistance), people will show up to work.

I have seen a number of professional economists and housing industry talking heads playing up the “resiliency” of the housing market during the Covid pandemic. Call it economic quackery if you will. The truth is that no one can accurately gauge the health of the housing market until Powell and company quit propping it up. The Fed refuses to let markets, particularly the housing and stock markets, function because they know what a glorious mess they have made.

“In the end the Party would announce that two and two made five, and you would have to believe it. It was inevitable that they should make that claim sooner or later: the logic of their position demanded it. Not merely the validity of experience, but the very existence of external reality, was tacitly denied by their philosophy. The heresy of heresies was common sense.” George Orwell, 1984

We are headed into the summer selling season, and buyers are looking at one of the most challenging housing markets in history. The supply of homes has never been lower and prices have never been higher. Simply put, there are no good choices. The only winners in the current housing market are home sellers. Buyers who are brave enough to take the plunge and try to compete with the FOMO crowd are simply making the best of a bad situation.

Buying a home in today’s market is a significant risk because the Federal Reserve has destroyed normal price discovery. Sure, there’s some upside if the Fed keeps pumping QE, but the downside risk is larger because the Fed has backed itself into a corner. Things would get ugly in a hurry if the Fed removed those asset purchases all at once. Powell and his FOMC counterparts are likely trying to find a way to ween the markets off of the heroin they injected without watching the whole house of cards implode. No easy task for sure, but before you get soft and cry a tear for Jerome, just remember that every Fed board governor is a multi millionaire.

It’s called trickle-down economics for a reason. Monetary policy by the rich, for the rich. Welcome to your warped, flipped, inflated U.S. housing market, sponsored by the Federal Reserve Bank of the United States.

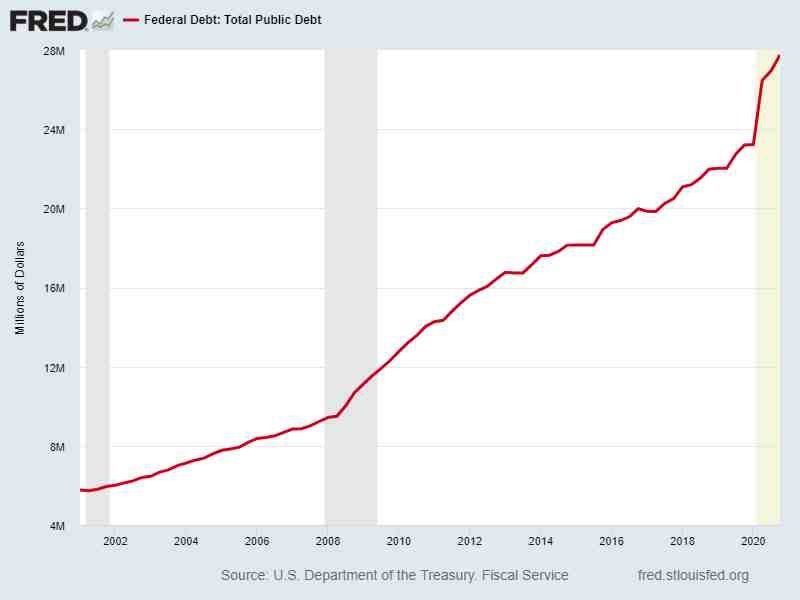

Rates are still low primarily because they have to be. With total debt in the system at stratospheric levels it wouldn’t take long for a sustained rise in interest rates to bring the entire house down. Someone has to service the growing pile of debt.

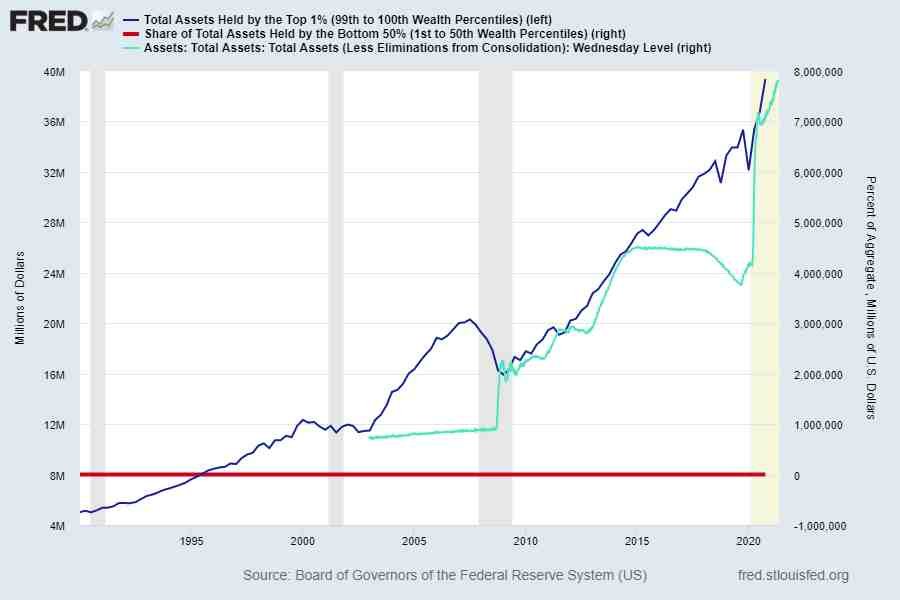

With continued corporate bailouts and QE the Federal Reserve has morphed into a virtual inequality machine. It should not be surprising to see the effects of Fed policy showing up in the local housing market, unless you haven’t been paying attention or refuse to look.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment