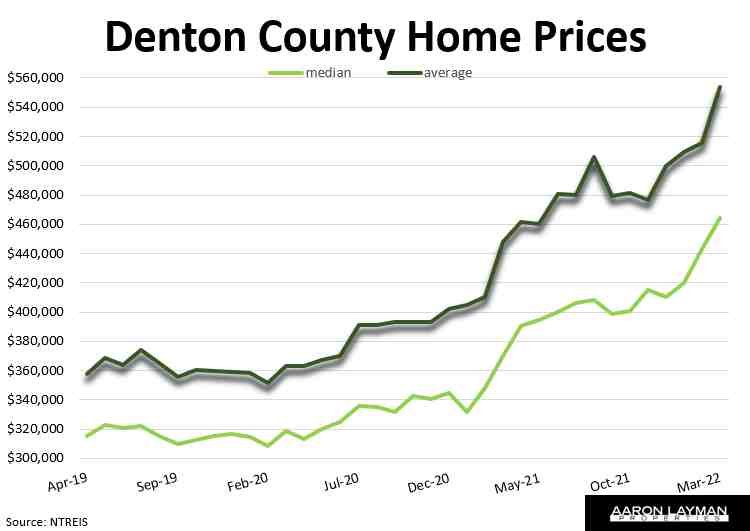

Fear of missing out (FOMO) was the theme last month in Denton County Texas as home buyers behaved like irrational humans often do. Buyers jumped into the local housing market front-running the coming Federal Reserve rate hikes. Home prices shattered records as a result. The median price of home rose 25.3% year-over-year to a record $464,000. Average prices rose 23.6% to a record high $554,098.

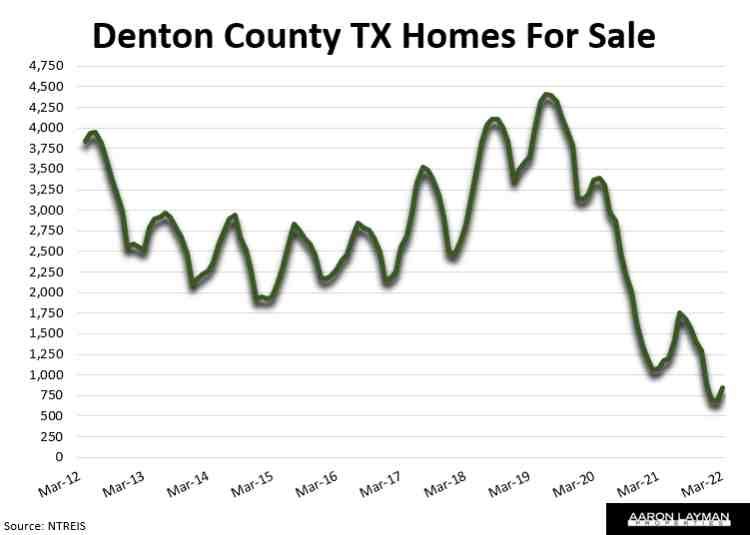

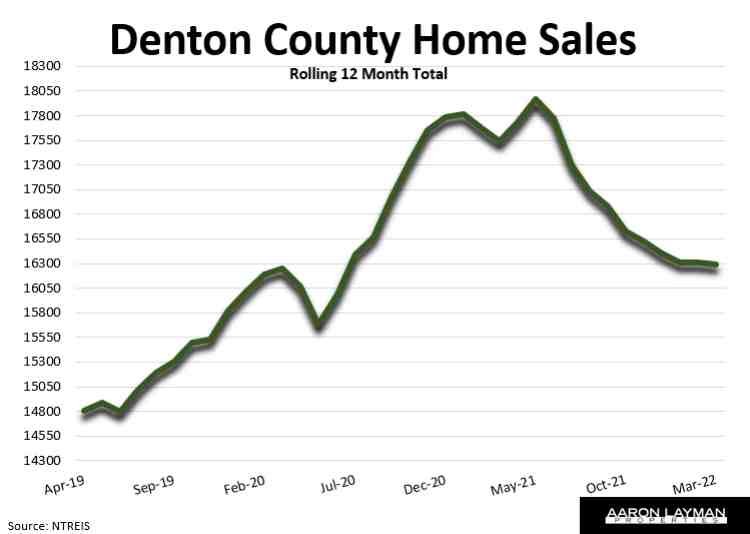

Closed sales were roughly flat compared to last year. That’s a testament to how frenzied the activity was given the current backdrop of spiraling interest rates. Pending sales (contracts) fell 10 percent. The number of homes available for sale jumped 23 percent from the record February low. Supply is finally warming up, and it will continue to grow.

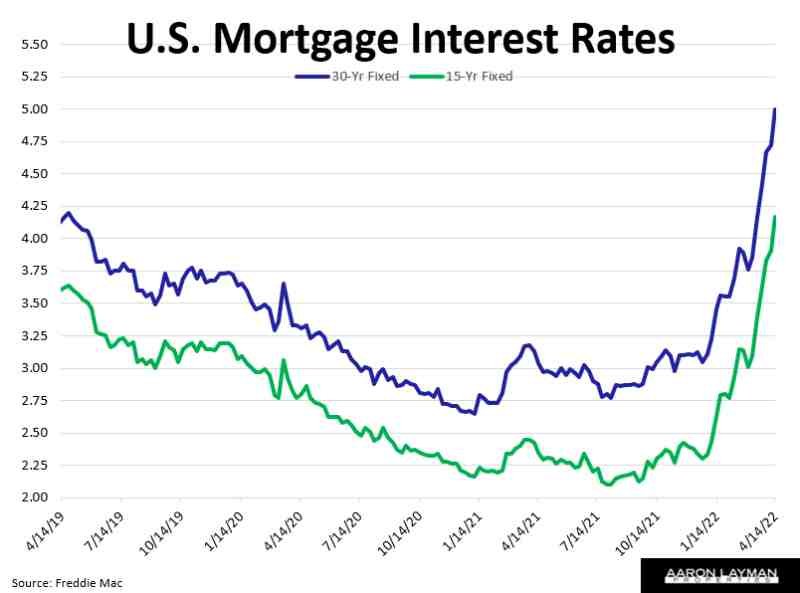

The slowdown in the housing market is just getting started. I will be posting a chart comparing the recent spike in monthly mortgage payments compared to last year. Real house payments are up dramatically as mortgage interest rates have roughly doubled from the 2021 lows. With the spike in nominal home prices, typical monthly mortgage payments for your average home buyer have soared by 50 percent looking at just the principal and interest payments.

The principal and interest payment on a median priced Denton County home was roughly $1312 last year, assuming a generous 20 percent down payment. In the span of 12 months median home prices have skyrocketed by over 93,000. Combined with the spike in mortgage rates, a median monthly P&I payment for a Denton County home buyer stands at roughly $1965. That’s a 50 percent increase in the monthly principal and interest payment in just 12 months! Throw in the increase in property taxes and hazard insurance and you get some real sticker shock. A realistic all-in monthly house payment (assuming 20% down payment) for a median priced home in Denton County Texas is now roughly $3,000 ($2959 by my calculations).

It doesn’t take a rocket scientist to see why FHA mortgage applications are dying on the vine. This has become a housing market for existing home owners and the wealthy (or at least moderately comfortable). Those living paycheck-to-paycheck have been left peering through the asset inflation window. Anyone without a sizeable down payment has been priced out of the market.

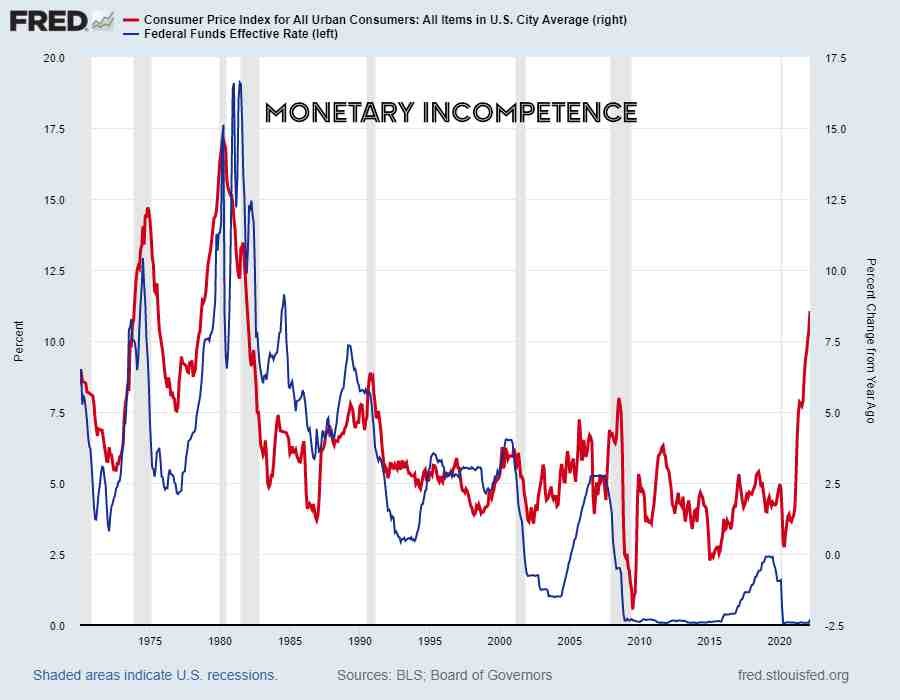

How did we get here? How could local home prices spike this hard into a Fed tightening cycle? It’s simple, really. The Federal Reserve and the economic arsonists inhabiting the Federal Reserve system have done basically nothing but talk so far. The real work has yet to begin. The Bureau of Labor Statistics just posted headline CPI inflation for March at 8.5 percent.

The official CPI reading for shelter inflation in March was 5%. You’d have to be an idiot to believe that’s anywhere close to reality. By official stats consumer price inflation in Dallas Texas stands at 9 percent. In reality inflation is easily above 10 percent in Dallas due to the gross under-estimation of housing costs by the CPI formulas.

Remember when the Powell Fed hiked the Fed Funds rate by a whopping 0.25% in February. Here’s how Jerome’s supposedly tough stance on inflation registers on a chart. The disconnect between real inflation and the Fed’s efforts to contain it is absolutely epic.

That gaping hole in the Fed’s credibility is precisely why there will be more pain to come for the housing market. The Powell Fed is still woefully behind the curve. At the same time the Fed’s clown economists wasting massive amounts of taxpayer dollars have been under-estimating how inflation has embedded within the economy every step of the way.

As Ben Hunt penned in a recent article it’s a case of NGMI, as in ‘not gonna make it’. The Fed’s economists are consistently wrong, and dangerous. They love their models and modals, no matter how useless they may be in the real world.

“Financialization is the zombiefication of an economy and the oligarchification of a society.”

The U.S. housing market has been ground zero for this financialization and zombiefication. As liquidity flooded the market during Covid existing asset homeowners went head-over-heals chasing every affordable home not tied down. Investors and speculators ramped up their already predatory activities in the housing market. Wall Street landlords have gobbled up thousands of additional single-family homes across the U.S. General speculation and investor activity went nuts the past 24 months as the trickle-down liquidity and stimulus went to work in the housing market.

What comes next will undoubtedly be less fun. Cleaning up the mess will require a lot of work. Up to this point, the Fed has trotted out every FOMC mouthpiece to offer up various flavors of spin and misdirection. Taming the inflationary monster they created will entail more pain for asset prices. By pretending inflation was not a problem for so long, the Fed has all but assured they will have to break something to bring the market back into balance.

Home prices are formed at the margins. With the market already turning it’s going to be interesting to see how much pain the Federal Reserve is willing to inflict on existing asset owners. They spent the last two years lining their pockets. Meanwhile, American workers are getting buried by spiraling costs. It is no mystery why U.S. labor is revolting in such large numbers. The purchasing power of said wages keeps getting whittled away by the Fed’s quest for inflation.

The first few months of 2022 have been absolutely brutal for housing affordability. Median monthly payments in Denton County have stretched beyond the reach of many marginal buyers with little or no down payment. I put together a chart showing the principal and interest payments and total payments since January 2021. Keep in mind the last data point on the chart factors a 4.5 percent interest rate for the month of March. We’re already above 5 percent. If I had used a 5 percent mortgage rate for that last data point, the year-over-year increase for a median P&I payment would have been 54 percent. Ouch!

If you think this kind of affordability crunch is not going to affect the housing market, you simply aren’t paying attention. I would also add that I included a rather conservative estimate of 2 percent for the property tax rate in that total monthly house payment. Most industry calculators low-ball your property tax estimate by a wide margin to make the payments look more affordable than they really are. Local buyers chasing new construction with PUD’s or MUD’s could easily find themselves with property tax rates above 2.5 percent. They’re going to receive some really nasty appraisal assessments in the next couple of years as the CAD’s look to empty the wallets of Texas homeowners.

The current picture for prospective buyers, particularly first-time buyers and those with minimal down payments is summed up by Freddie Mac’s chief economist, Sam Khater.

“As we contend with historically high inflation, the combination of rising mortgage rates, elevated home prices and tight inventory are making the pursuit of homeownership the most expensive in a generation.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment