Luxury homes and land continue to see strong demand in North Texas. Expensive properties have been driving up nominal prices in North Texas for several months. March 2024 sales data shows average home prices in Denton County up 7.4 percent from last year. Before you get excited, most of the price appreciation over the last few months has been centered in the luxury home market and inflated land values.

Zooming in to normal single-family homes between 1500-3500 square feet, average prices increased by 4.1 percent over the past year. In fact, the average price for those typical single-family homes was $78,000 lower than the overall average which includes all property types and sizes.

New homes are still selling well as builders make price cuts and concessions. Resale inventory has seen a noticeable increase in 2024, rising 41 percent from a year ago. That increase translates to a 60 percent increase in terms of months of inventory. Builders will have to continue the incentives if they want to maintain sales momentum. Today’s red-hot inflation data means we’ll probably seen even more home inventory on the market as demand gets curbed again.

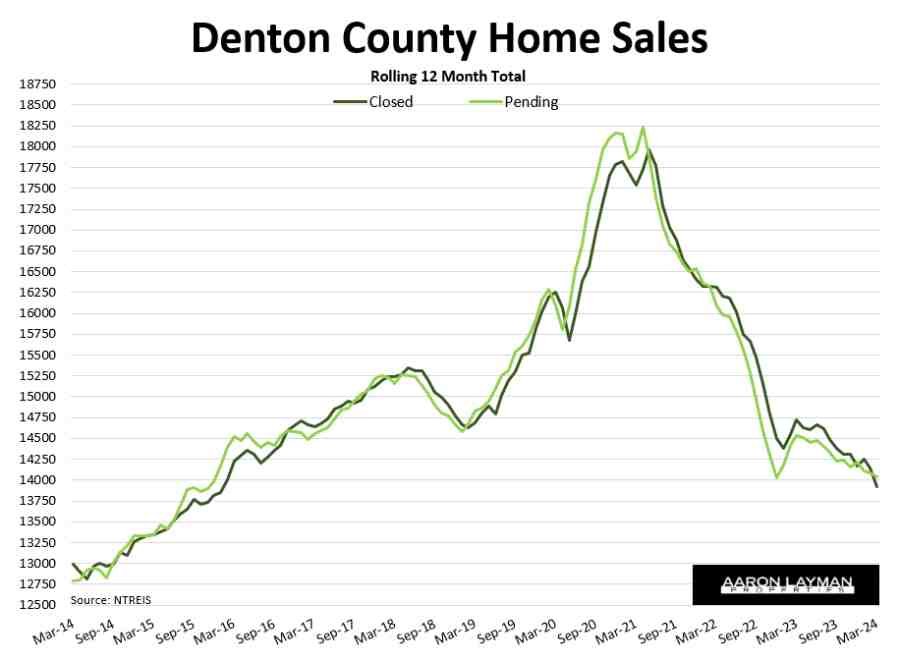

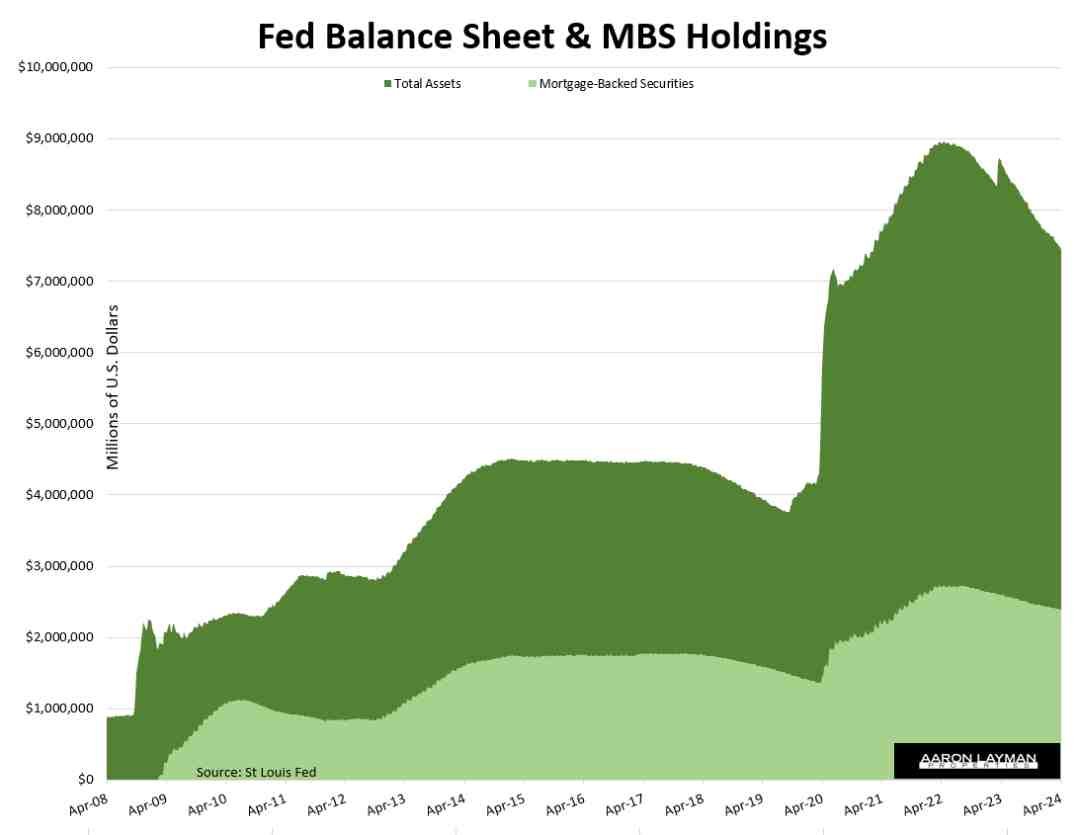

The North Texas housing market is holding up pretty well despite lagging sales. Closed sales were 15 percent lower year-over-year, but prices have been holding up. Some people are surprised that expensive luxury homes are seeing a strong bid, but it makes more sense if you understand the expanding monetary base and the huge budget deficits propping up spending. Did someone say it’s an election year.

While the Federal Reserve has waffled back and forth on quantitative tightening, Janet picked up the slack and kept the money printers flowing this year. With ample and liquidity and stock prices near record highs, asset-rich consumers have shown they are happy to keep spending.

Land Owners Still Gaming the System for Huge Tax Breaks

Luxury homes aren’t the only property category seeing strong demand. Raw land continues to be a popular investment hedge in Denton County. The property tax shell games available to owners of $million dollar properties are extremely lucrative for those who understand the loopholes.

This is why we see Denton County landowners with real full-time jobs outside of agriculture sitting on expensive land while paying virtually nothing in property taxes. An average homeowner in Denton County could be paying $10,000 in annual property taxes for the average single-family home while an adjoining land owner pays less than $100 per year on property worth twice as much. Sounds fun, right.

The Ruse of Uniform and Equal Appraisal

This is how Texas does “uniform and equal appraisal”. It’s significantly different than the official version floated by representatives in Austin. While many less affluent homeowners are getting hit with continued appraisal creep (and higher property taxes) we have land-owning speculators trying to sell land for over a $million while paying only $5 in annual property taxes. This is the kind of insanity happening in the current market in Denton County Texas.

Generous gifts/loopholes in the property tax code allow these owners to hold out for inflated prices while they destroy a significant portion of the local tax base. It’s fascinating to watch, because many of these same land owners also hold themselves out as staunch supporters of business and economic development. What they really mean, of course, is that they support business and development as long as it doesn’t infringe on their scenic views or cause them to pay property taxes like a normal homeowner.

Financialization of Housing Fueling Shortage of Affordable Homes

I have been pounding the table on the financialization of homes for several years, so this latest development was pretty entertaining. As readers of this blog or my monthly column understand, the shortage of affordable homes is much more complicated than industry cheerleaders would have you believe.

The “shortage” of available homes in the U.S. ranges from 2-5 million depending on which industry player you are talking to. The standard answer to the problem from most of these industry players is always more supply. It’s a broken record, and a disingenuous solution to a complex policy-driven problem.

The example I am about to describe goes to the heart of the housing “shortage” and the financialization of homes in general. My social media feed is scattered with posts from home builder sales reps, but one recent post in particular caught my attention. A builder sales representative working for the largest builder in the country posted a brand new home for rent. My initial reaction was to query why the builder was leasing this home instead of selling it since this was not a rental community. The rep responded that it wasn’t the builder’s property.

Turns out the sales rep and his wife purchased the house for their own investment, directly from spec inventory…in a community this representative is actively promoting and selling. If you don’t understand the moral hazard of that setup, no amount of explaining will convince you that’s a problem.

Inflation Surprises to the Upside…Again

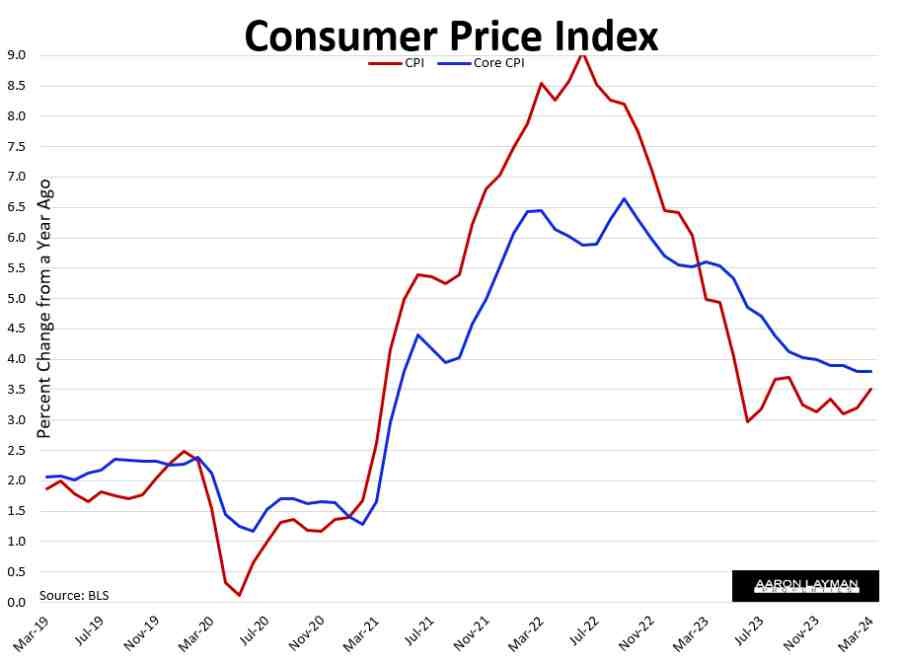

March inflation numbers came in pretty hot. The official Consumer Price Index showed inflation at an annual rate of 3.5 percent in March. Core inflation was higher still at 3.8 percent. The truth is that both numbers are probably understating real inflation. To see what I mean just take a look at your costs for homes, automobiles and health insurance.

Wage and price inflation is firmly embedded into the economy. This is why many consumer’s “vibes” are simply a reflection of reality. Real inflation continues to be higher than what the government is reporting in the official numbers. A recent analysis found that the CPI last year could have been 80 basis points higher if the BLS factored in actual homeowner’s insurance costs in the Consumer Price Index calculations.

The gaslighting is even worse if you look at health insurance costs. The March 2024 CPI change for health insurance costs shows a 15.2 percent decrease over the last year. You read that right. The BLS wants you to believe your health insurance costs decreased by 15 percent over the past 12 months.

It appears election-year politics will continue through November. The Biden administration seems to be willing to accept the gamble of higher inflation to keep asset prices elevated, probably in the hopes enough people will still “feel” wealthy.

If you are in the market to buy or sell a home, remember that it could get a little bumpy. Elevated inflation means mortgage rates aren’t coming down as some agents and loan officers were hoping. This will continue to put a damper on home affordability and restrict demand in the real estate market.

Updated: Mortgage rates had their worst day since October 2022 today. The rate on a 30-year fixed-rate mortgage spiked to 7.34 percent. Ouch!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment