More intervention won’t fix the housing market. This simple truth is obvious to most serious practitioners in the industry. The current affordability challenges facing the U.S. real estate market go well beyond interest rates. Truth is irrelevant to many politicians in an election cycle, so the insanity and market tinkering continues.

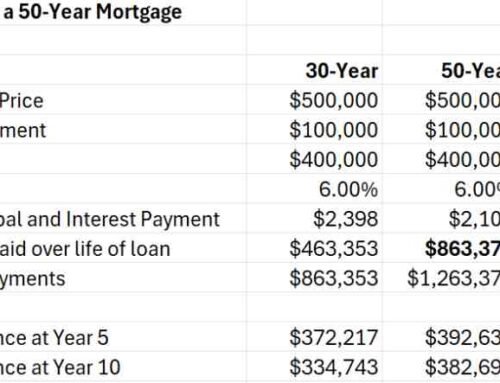

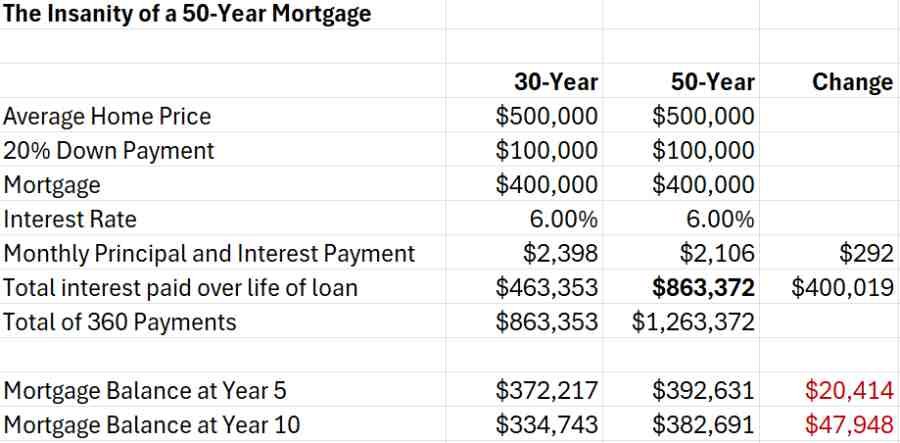

It was beyond absurd for the Trump administration to pitch the idea of a 50-year mortgage. That half-baked idea from FHFA director William Pulte Jr. fortunately had a fairly short news cycle. With midterms elections in focus and favorability ratings in the basement, Trump is grasping at straws to fix a complex problem with no easy solutions.

If you’ve been paying attention, you probably remember the colossal mistake of the Federal Reserve’s MBS purchases which turned the U.S. housing market into a pretzel. $3 trillion in MBS purchases by the Fed upended the housing market, facilitating a massive spike in home prices.

The Definition of Insanity

That bubble has been unwinding over the past three years, picking up steam in 2025 as inventory finally returned to the market. Many asset owners and real estate industry players don’t like the idea of affordability if it means actual affordability in the true sense of the word in current economic conditions. That brings us to Trump’s proposal to buy $200 billion in MBS to bring down mortgage rates. If market intervention is what caused your affordability issues, surely more intervention will be better, right?

Trump’s MBS tinkering is another bad idea piled on top of bad ideas we have seen over the last twelve months. If you look at the plumbing of the GSE’s (Fannie Mae and Freddie Mac), you will get a better idea of why Trump’s latest scheme is poorly designed, and likely a big nothing burger for the housing market. It could actually make housing affordability worse by propping up prices when the market needs more time to heal.

Mortgage spreads have already tightened. $200 billion will be a rounding error for the current size of the market. With the latest political pulp, Trump gets control of the narrative while pretending to do something. Providing a small bailout to banks and REITs while shifting more risk on to U.S. taxpayers won’t help the housing market. That’s irrelevant when the focus is on the November elections.

Denton County Housing Market Update

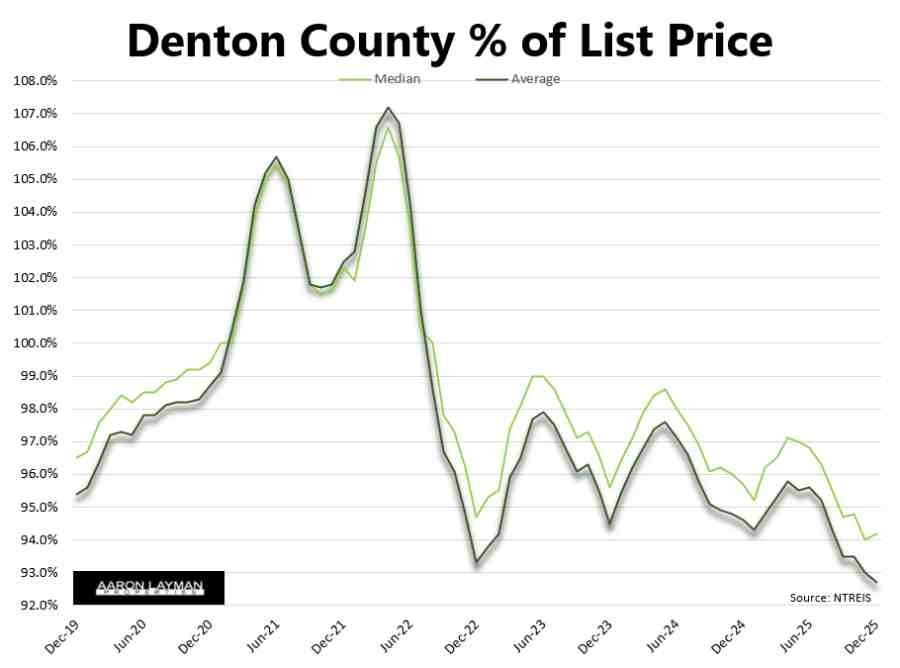

The housing market in Denton County finished 2025 on mixed footing. Median and average prices finished the year down 9.6 percent and 7.9 percent respectively. Closed sales were up 2.5 percent year-over-year in December. Pending contracts slid 8 percent. Months of supply was up 9.7 percent.

Average days on market jumped to 74 days in December. That was a 25 percent rise from the previous year and the highest since 2012. Sluggish would definitely be an accurate description of the overall sales picture. 2025 was a challenging year for the housing market. Affordability was severely strained and the labor market was particularly weak.

This brings us back to the issue of affordability and rates. Rates were never the problem. The problem has always been the prices and a massive bout of home price inflation where home prices became detached from incomes. Median home prices in Denton County are still roughly $110,000 higher than where they stood five years ago. If your salary hasn’t increased by 35 percent during that time frame, you understand why this could be a problem.

Mean Reversion

It’s no coincidence that median home values in both Denton and Collin Counties converged to roughly the same point at the end of 2025. These two North Texas counties each have over a million residents. Each area saw a significant bubble and subsequent unwind. The bubble in Collin County was more pronounced, so the correction has also been sharper.

Median home prices in Collin County finished 2025 over $155,000 lower than the 2022 bubble peak. Median prices in Denton County finished the year roughly $75,000 off the 2022 high. That difference can be attributed to a flurry of new construction in Collin County that is still working its way through the pipeline.

Median home values for both counties fell to roughly $420,000 in both areas. That’s a good indicator of what most families can afford in the current market relative to incomes. Average prices are higher because many cash buyers and luxury home buyers aren’t as constrained by income. They have assets and larger down payments.

If you want to sell a North Texas home above $500,000, you better bring the receipts. That theme will likely continue this year in 2026. Any prudent buyer is going to question the value…and for good reason. Above $500,000, the property taxes, insurance and carrying costs are getting prohibitively expensive for most Texas families.

Softer Rents

Single-family rents in Denton County finished 2025 down roughly two and half percent. Lease prices for single-family homes continued the trend we’ve seen for the last three years. After the construction boom and financialization frenzy culminating in 2022, rents continued to edge lower at a very modest pace.

Affordability for apartments has improved a little more. Apartment rents in Denton Texas are down 7.3 percent year-over-year in January. That’s the largest decline in asking rents across the DFW area tracked by Apartment List. Rents started off 2026 lower across the DFW area, but with more muted declines for most submarkets.

Chaos to Continue

With the focus on the midterm elections picking up steam, expect the chaos and shenanigans to continue. It’s going to be an interesting year for the housing market for sure. Will lower rates solve the affordability crunch? Of course not! Will that stop the current administration from more self-inflicted wounds? Probably not.

If you are in the market to buy or sell a home, expect more volatility and more shenanigans. The housing market’s affordability puzzle won’t be easy to solve. That won’t stop politicians from pretending they have a fix.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment