North Texas home sales continue to soften. September sales data reflect a 9 percent slide in closings in Denton County. The DFW area experienced a 5 percent slide in home sales last month according to NTREIS Trends data. Pending sales in Denton County were flat to just slightly negative last month. The broader Dallas-Fort Worth area saw a 3 percent decline in September sales contracts. With the Federal Reserve expected to announce a taper of their huge asset purchase program ($120 billion per month) things have been a little wobbly in the markets.

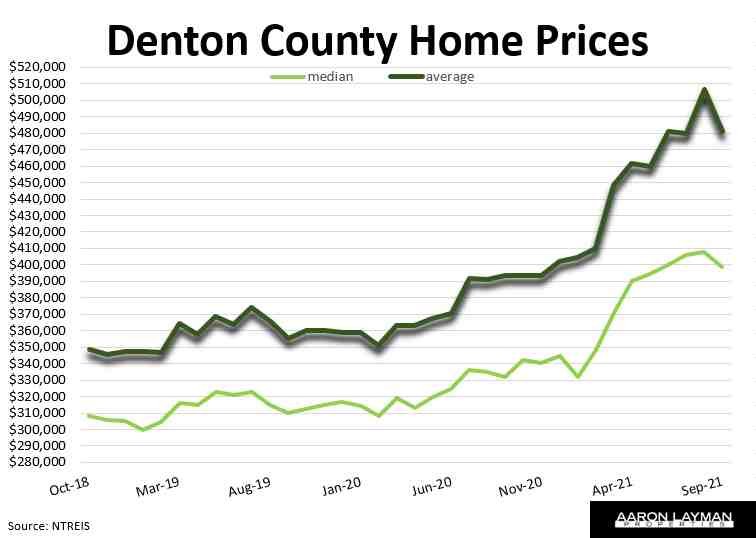

After marching to new record highs in August, median and average home prices fell in September. The average price of a home in Denton County dropped about $25,000 from the previous month. That still puts average price up 22.4 percent compared to last year. The entire North Texas area saw average prices that were 17.9 percent higher. Average prices in the greater Dallas-Fort Worth area have been treading water for the last 3 months, hovering just above the $400,000 mark.

All eyes are now on the Fed. Central banks have made another fine mess of global asset markets with a record deluge of liquidity during the last two years in response to Covid. Supply chain disruptions and shortages are popping up all over the economy. Global energy markets are in turmoil as natural gas prices recently soared to record highs. Power outages are being reported in numerous countries across the globe.

China’s Evergrande story is just getting warmed up as the country’s over-developed housing industry attempts a major deleveraging. Canada hasn’t even come to grips with their property bubble, as the country’s leadership is apparently pinning their hopes on continued immigration to support massively inflated property values.

Here at home many property owners are still in denial. Don’t ask a local economist for a forecast, because most of them have been asleep at the wheel. Industry shills involved with housing are still expecting a soft landing and hoping for continued growth. That growth may be hard to come by.

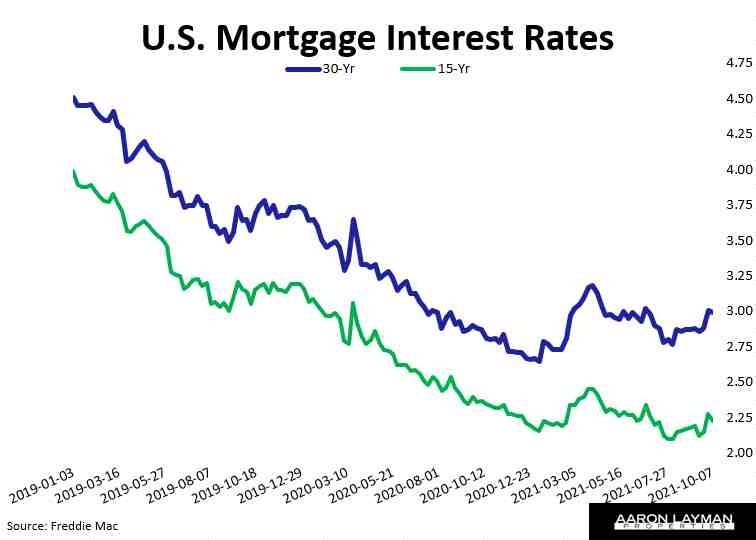

The last few weeks have seen interest rates move higher. Inflation is now firmly embedded in the U.S. economy now matter how many denials we keep hearing from Federal Reserve officials. While they were busy trading their own books for pandemic profits, FOMC officials neglected to do their real job and regulate the U.S. financial system.

Decades of trickle down fiscal and monetary policy are hollowing out the economy and killing what’s left of a productive U.S. middle class. With continued bailouts of elite white collar criminals and Wall Street parasites, the Federal Reserve has managed to shift even more wealth to the top 1% of income earners. The top 1% in America now own a larger share of U.S. wealth than the entire middle class. The Fed’s own statistics show the evidence of the decades-long destruction.

It’s actually worse than the chart above shows. The middle 60 percent of U.S. income earners, those making between $27,000 and $141,000, now hold less wealth than the top 1 percent of Americans. That means 1.3 million households have more wealth than the 78 million households in the middle combined. And they say crime doesn’t pay. LOL!

Julius Krein penned a wonderful essay The Value of Nothing: Capital versus Growth. It helps to explain how Wall Street parasites have continued to sacrifice long term prosperity and productivity for short term wealth and elevated asset prices. You could call it the Nikefication or financialization of American business. From San Francisco to New York, American CEO’s have become devoid of a moral compass. We live in a world where the CEO of one of America’s largest banks received a retention bonus AFTER racking up multiple felony counts over the last decade. It’s almost like there are two different sets of rules for regular businesses and TBTF banks.

“Behind every great fortune there is a great crime, as the saying goes. And within every celebrated Silicon Valley company there is also extraordinary self-delusion. The two are not unrelated.”

Those Silicon Valley/Wall Street values certainly extend into the housing sector. Economists, agents and various pundits keep preaching the endless growth story even as the ranks of homeless Americans keeps growing. It’s telling that you have consultants in the housing space cheering record high prices even as millions of Americans are getting priced out of the market. Federal Reserve officials, entrusted with the nation’s monetary policy, were actively trading their own books during the pandemic even as they pushed a transitory narrative of inflation. It’s hard to imagine anything more deplorable, but that’s where we are.

The local housing market is already correcting, before the Fed has even had a chance to taper. More typical seasonality is beginning to enter the market. The larger question is what happens when the Fed pulls the rug from these inflated asset prices. Average percent of original list has fallen for 3 consecutive months in North Texas. Homes were selling for 100 percent of list in September. That’s still above normal market conditions of 96 to 98 percent of list.

Builders have tried to meet the sharp spike in demand created by the Fed’s liquidity bomb. It will be interesting to see what happens with prices when housing supply levels come back to more typical historical trend. We currently have 1.4 months of supply in North Texas. New construction supply is sitting at 2.1 months. That could grow with a backlog of permitted construction projects and cooling demand in general when the Fed walks back their massive stimulus experiment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment