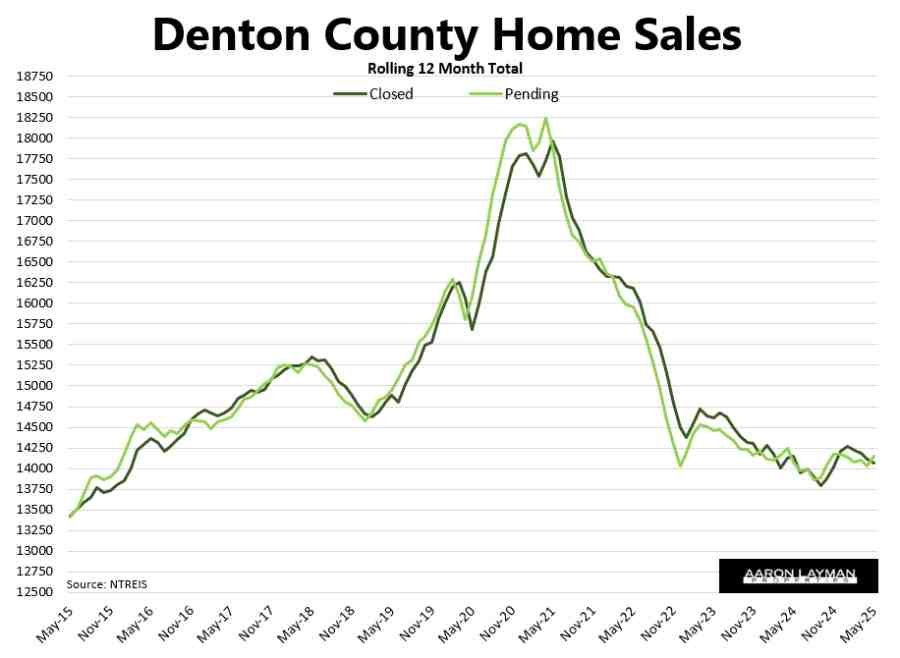

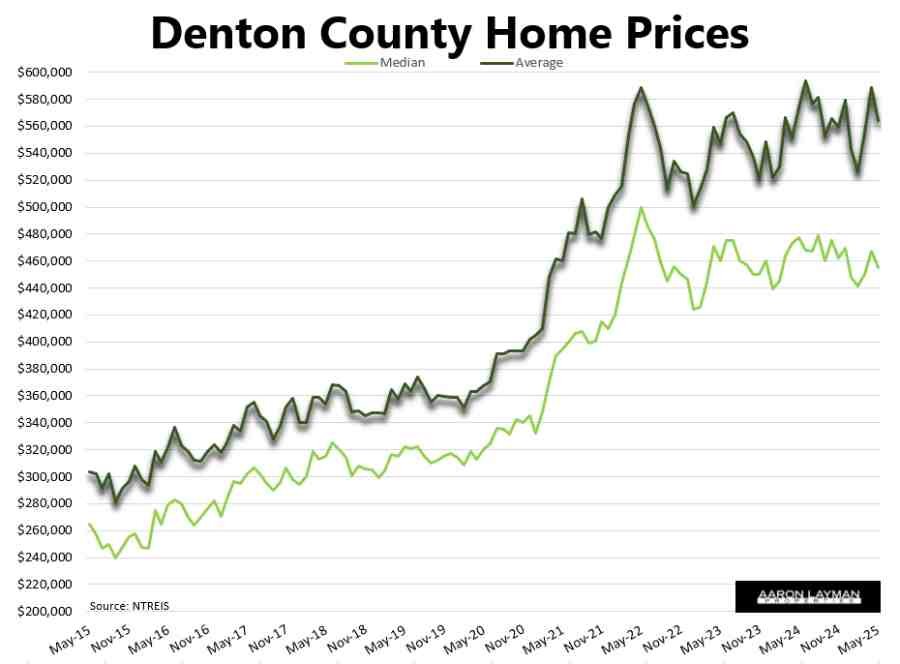

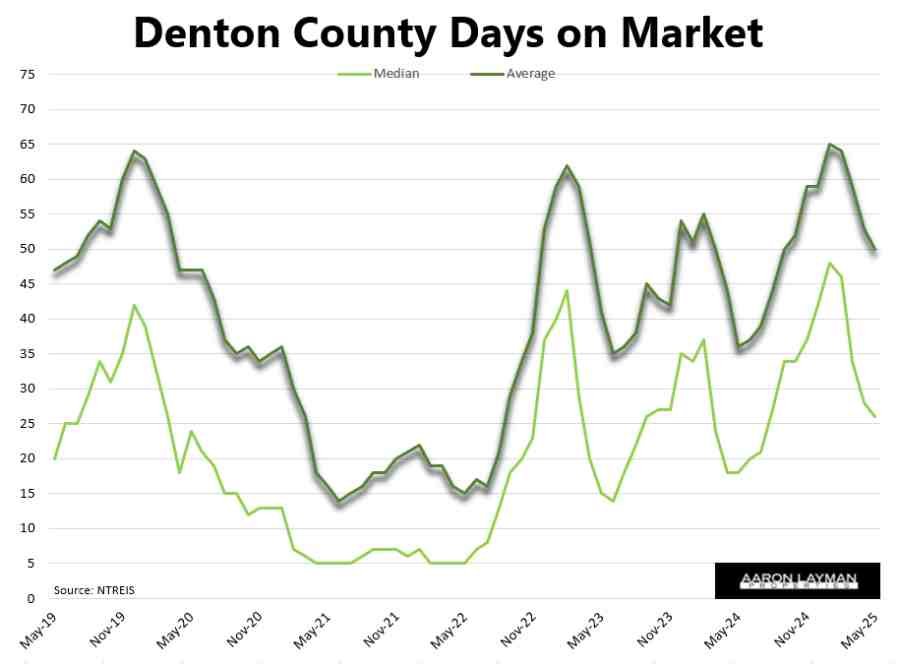

Stagflation continues to be the theme for the North Texas housing market. Sales and contract activity remain sluggish as DFW home prices remain at inflated levels. Home sales across North Texas slid 5.5 percent year-over-year in May. Sales were down 3.5 percent in Denton County. Collin County managed a 1 percent increase. Median prices slid 4.8% and 4.9 percent respectively in Denton and Collin Counties.

That reversion to the mean has been a consistent trend so far in 2025. Severely strained housing affordability levels continue to take a toll on contract activity. At the same time, wealthier buyers with larger down payments or full cash purchases are keeping average prices propped up. This stagflationary setup has resulted in a continued rise in carrying costs such as insurance and property taxes. Buyers shopping with a mortgage are still having a tough time with interest rates bouncing between 6 and 7 percent.

Drive Till You Qualify

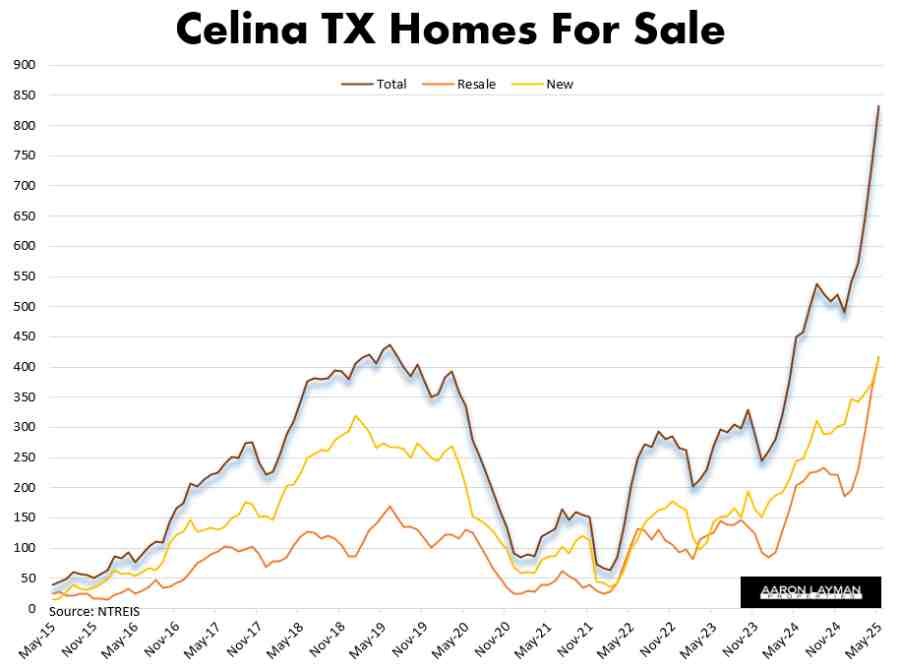

Celina and the north DFW suburbs remain grounds zero for this reversion to the mean. As inventory continued piling up in May, median home prices in Celina dropped 14.7 percent year-over-year. Average prices sank 5.5 percent in Celina from May of last year. To put the correction in perspective, average prices in this suburban DFW market are still $166,000 lower than the bubble top experienced in May 2022.

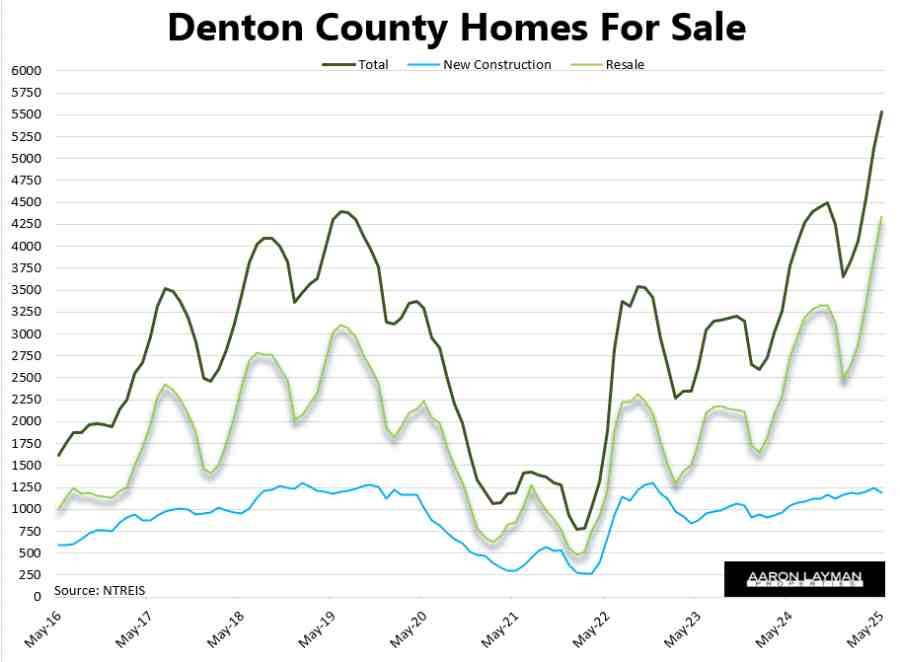

Available home inventory has exploded in Celina this year. The number of homes for sale rose 85 percent year-over-year. Months of suppy is up 74 percent to 7.3 months of inventory. While many DFW submarkets have experienced a sharp rise in resale existing home inventory in 2025, new home builders are still working off a large pipeline of new construction inventory.

Now that the economy is cooling, some buyers are obviously having second thoughts on just how far they want to drive for that dream home.

Builder Consolidation Messing With Texas Housing Affordability

Those who know me are aware I’m a strong advocate for sensible antitrust policy and enforcement. We need more enforcement of laws on the books, and the sooner the better. One of the components helping to erode housing affordability happens to be homebuilders themselves.

Basel Musharbash recently wrote about this very topic in a piece for Matt Stoller’s Big newsletter, Messing With Texas: How Big Homebuilders and Private Equity Made American Cities Unaffordable. It’s a great read if you want to understand how policy decisions drive housing affordability. Like Stoller, I was around for the 2008 housing crash. I saw the government’s response and the mistakes that were made. We’re still paying for a lot of those policy errors.

Musharbash’s piece is particularly relevant since it focuses on consolidation in Dallas and DFW home building sector. Basel makes a solid case that continued consolidation among major home builders is in fact contributing to the affordability issues buyers currently face. Roughly 85 percent of the new homes sold in DFW now come from less than 30 builders. Your eyes are not deceiving you. North Texas has a lot of cookie-cutter homes.

The issues run well beyond aesthetics. Builders are actively inflating the price of DFW’s housing stock by avoiding price cuts with below-market mortgages. The massive size and capital available to major builders means they are able to secure forward commitments that builders then use for juicy rate buy-downs for buyers. This virtuous cycle of big rate buydowns and incentives allows builders to keep prices higher. At the same time, major builders continue to spend $billions every year on stock buybacks. This financialization for the C-suites and shareholders sucks capital away from the construction of affordable homes.

It’s convenient to use regulations and red tape as a scapegoat while you lobby for more government assistance. Building more affordable homes would be relatively easy for major builders. It’s just not a major priority when the financialization game is such an attractive option.

The FHFA’s Loan Limit Credibility Gap

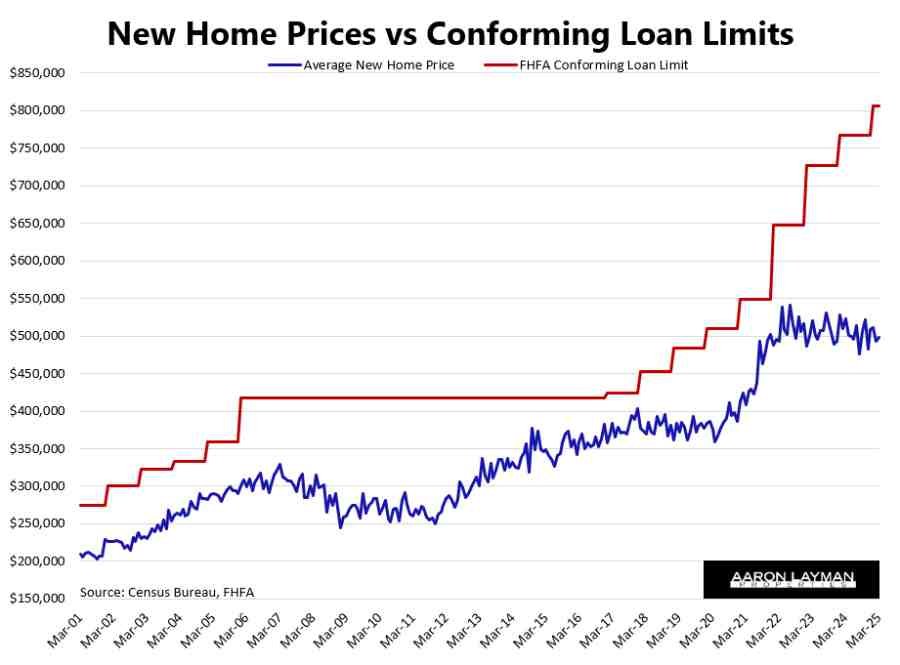

Speaking of financialization, Bill Pulte continues to provide some interesting views on a potential GSE release. We’re talking about Fannie Mae and Freddie Mac. Pulte seems to be keen on taking the government-sponsored entities private and releasing them from conservatorship.

If you know anything about the Great Recession and what led to their government takeover, that should raise some concerns. Director Pulte keeps avoiding my question as to whether he would support lowering conforming limits to more rational levels, prices and loan limits that most Americans can actually afford. My protestations have continued to go unanswered. I can understand why, but the lack of transparency is still extremely disappointing.

It’s kind of wild to see the new FHFA director gaslight Americans about housing affordability challenges. Pulte could be pushing to bring loan limits back toward reasonable, affordable levels. Instead, he seems more interested in letting the GSE’s run wild. It is beyond ridiculous for a government official to pretend they care about high costs to U.S. home buyers when they are simultaneously facilitating higher costs for home buyers.

Across most parts of the U.S. you can secure a conforming loan up to $806,500. That doesn’t mean you should. Sometimes a little restraint is a good thing.

If you are in the market to buy or sell a home, be safe out there.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment