DFW home sales took another hit in April. Home sales slid 18 percent during the month of April as the coronavirus took a toll on the Dallas-Fort Worth real restate market. Pending home sales slid even further, falling 24 percent for April. Despite the noticeable seasonal increase in activity during the past few weeks, it appears the spring/summer selling rush we would typically expect is going to be muted by Covid-19 this year. With over 33 million Americans filing for unemployment during the past two months, a downturn in real estate activity should be expected.

On the bright side, Dallas-Fort Worth home prices are holding up very well so far. The median price of a DFW home rose 4.9 percent year-over-year in April to $278,000. Average home prices in the DFW area were basically unchanged, falling 0.1 percent to $321,104. Both median and average price per square foot were at record highs for the month of April. Buyers continue to sacrifice size and space as they look to keep total prices and payments affordable.

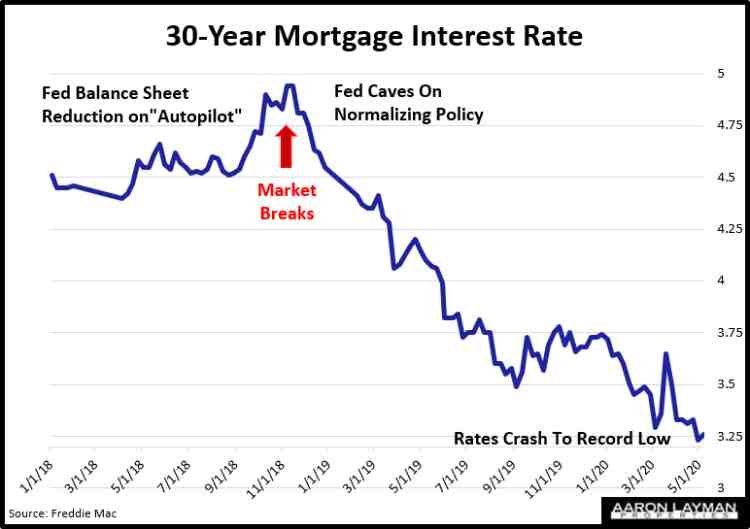

Home affordability was aided by some record low mortgage interest rates in April. Without those record low mortgage rates, the DFW real estate market would be getting hit even harder than it is. For those with good credit and income profiles, the rates are better than they’ve ever been. Borrowers with less than prime credit are getting hit with higher rates and fees in many cases as originators and servicers look to shore up the risk profiles of their mortgage portfolios.

New home sales continued to provide support to the Dallas-Fort Worth real estate market in April. The Covid-19 downturn has widened the gap between new and existing home sales. With more existing homeowners holding inventory off the market, new home sales have benefited from the continued demand for homes. Resale home closings were down 20 percent in the DFW area in April, yet sales of new construction fell only 9 percent. Pending sales for existing DFW homes plummeted 30 percent last month while pending sales of new homes in the Dallas-Fort Worth area were up about 6 percent. Builders are no doubt thanking their lucky stars that the market is not currently flooded with inventory, at least not yet. Overall months of supply dipped 15 percent in April to 2.8 months of inventory.

That preference for new construction during the Covid-19 downturn was also prevalent in Denton County, one of the fastest growing areas in the DFW real estate market. Denton County saw home sales fall 13 percent in April while pending sales slid 19 percent. Pending sales of existing homes were down 26 percent, while pending sales of new construction rose 3 percent. Median home prices in Denton County were flat in April while the average price of Denton County home rose 2.1 percent to $365,165. Prices of new homes in Denton County continued to fall, with the median price of new construction dropping 8.9 percent to $325,990. The average price of a new Denton County home fell 6.7 percent to $374,628.

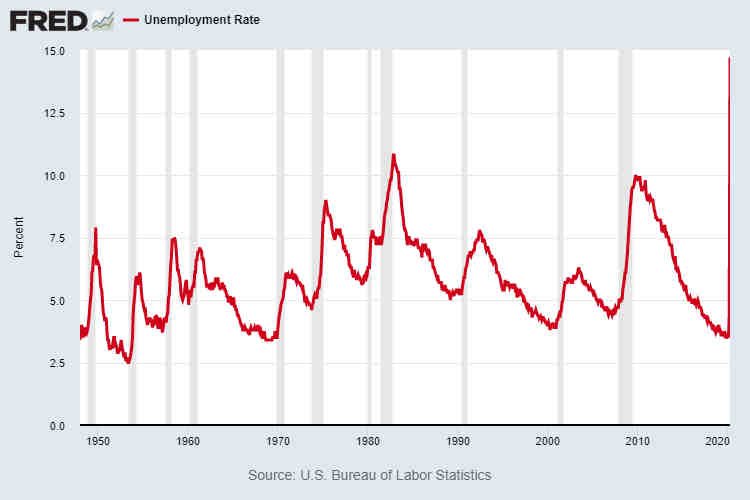

With skyrocketing unemployment levels not seen since the Great Depression it is not surprising (at least it shouldn’t be) that buyers are looking for affordable homes. In the University Park/Highland Park area, home sales plummeted 40 percent last month while pending sales nosedived about 65 percent. Average home prices in this tony Dallas submarket plunged 37 percent year-over-year to a bargain price of only $958,590.

In consumer-entertainment-centric Frisco Texas, the Covid-19 downturn continued to hit the market for McMansions. April home sales fell 33 percent in Frisco while pending sales tanked 36 percent. If it weren’t for the sale of some expensive new homes in Frisco in April, the 0.2 percent decline in median overall prices would have been worse. Median resale home prices in Frisco still fell 3.4 percent, with average resale prices sliding 1.9 percent.

The Federal Reserve has gone full Japan in its efforts to bail out Wall Street and corporate America, but that trickle-down monetary heroin is goosing asset prices rather than saving the real economy. Similar to the response following the Great Recession, government and Fed stimulus efforts have been largely directed to banks and existing asset holders. Covid-19 policy responses are exacerbating wealth and income inequality even further in the U.S. This will make any real “recovery” very problematic. That means the bifurcation in the real estate market will only continue, and perhaps become even worse.

After a massive increase in the Fed’s balance sheet during the past two months, the pace of QE has tapered off now that the stock market has been levitated. Unfortunately the stock market is NOT the real economy, particularly for the 90 percent of Americans who have little or no savings invested in it. This goes to the heart of the Federal Reserve’s credibility trap. With the money the Fed has printed during the past two months bailing out corporate parasites, the Fed (via the U.S. Treasury) could have sent a check of over $18,000 to every American family to shore up their finances. Of course that’s not what happened. If you were lucky you received a check for $1200. Many people are still waiting for stimulus checks or unemployment benefits, hoping the money arrives in time to avoid defaulting on payments. For Wall Street, that helicopter money arrived in spades with virtually no questions asked.

Matt Taibbi has an excellent review of how the Covid-19 bailouts have helped to save wealthy Americans and provide lift to the stock market, at least for the time being.

“The $2.3 trillion CARES Act, the Donald Trump-led rescue package signed into law on March 27th, is a radical rethink of American capitalism. It retains all the cruelties of the free market for those who live and work in the real world, but turns the paper economy into a state protectorate, surrounded by a kind of Trumpian Money Wall that is designed to keep the investor class safe from fear of loss.”

As we navigate our post-Covid-19 real estate landscape the preference for affordable real estate will likely continue. Despite some assertions of real estate pundits and professionals, a return to pre-pandemic sales levels isn’t going to happen anytime soon, not with real unemployment in the U.S. north of 15 percent. As the Texas economy begins to open back up, many business owners are realizing that demand is still depressed. Commercial real estate owners are staring at a perfect storm of over-supply and depressed demand, particularly when you are talking about retail and office space.

If you are in the market to buy or sell a home be safe out there. If you are looking for ideas to mitigate your Covid-19 risk, here is a good primer/update on the risks of the Covid-19 virus and how to avoid them.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment