Denton County house payments hit record highs in July. Prospective home buyers continued to get pinched by higher mortgage rates and the rebound in North Texas home prices through the first half of the year. As mortgage rates mushroomed back toward 7 percent, area house payments have soared for buyers using a market rate mortgage.

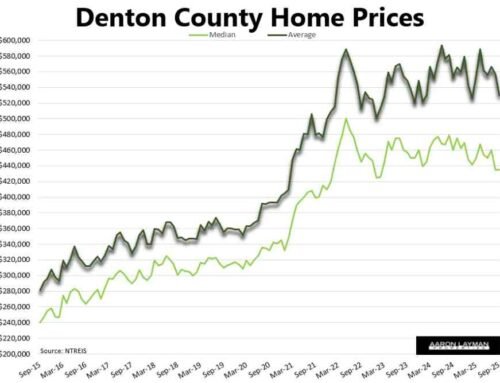

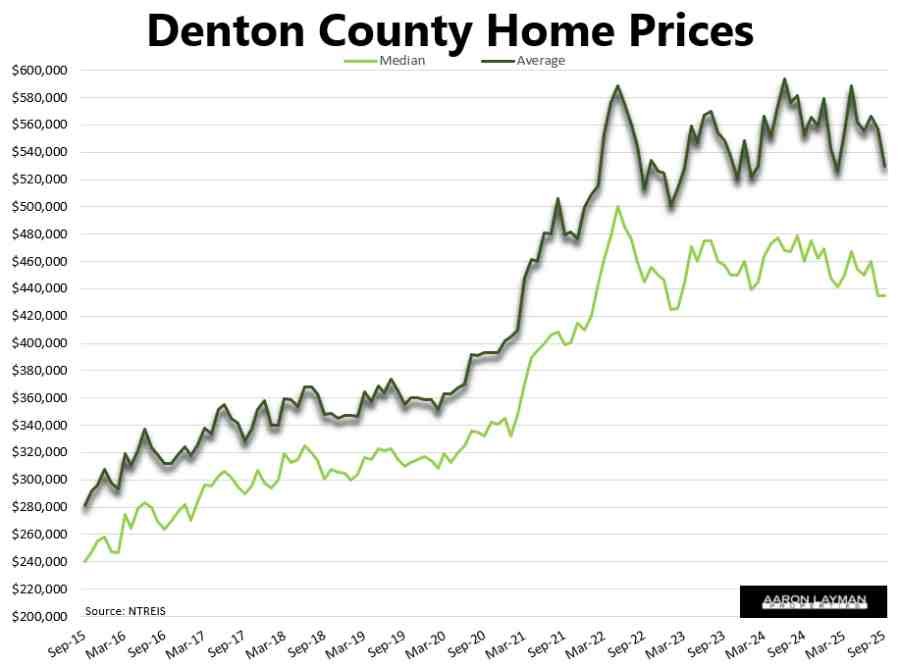

Median home prices came in at $475,000 for the month of July. The median house payment for Denton County buyers factoring in the rise in interest rates translates to a principal and interest payment of over $2500 per month. That’s just for the mortgage loan. A Denton County home buyer was looking at total monthly payment of over $3,400 in July. Those are conservative estimates factoring in a 20 percent down payment. The total monthly payments would be even higher for buyers putting less money down.

The numbers get even more nuts if you look at average home prices of $568,000 in July. That would translate to a principal and interest payment of roughly $3,000 with a total house monthly house payment over $4,000. House payments for prospective buyers have essentially doubled from where they stood at the beginning of 2021. Principal and interest payments have skyrocketed 130 percent!

As homes have become increasingly unaffordable, home sales have continued to stagnate. Closed sales posted a noticeable drop in July, while pending contracts dipped as well. Contract activity was 7 percent lower than last year. This is a longer-term view of sales activity in Denton County…

As I have said before, it is likely premature for housing industry pundits to be calling a bottom in the housing market. A recession is still squarely in play, and it looks like sales activity is going to get pushed lower again heading into the end of the year.

Higher mortgage interest rates continue to take a bite out of housing demand. This is why we are seeing local home builders ramp up the incentives again. Mortgage rate buy-downs have become a critical ingredient behind recent sales activity. Those incentives aren’t going away as long as rates stay elevated.

While headline inflation is finally cooling, the reality is that homes, cars, healthcare and insurance are all still very expensive. If you strip out all of the things consumers need on a regular basis, inflation looks to be making some improvement. In the real world asset price inflation has put a major dent in consumers’ purchasing power.

It was always dishonest for Federal Reserve officials to pretend inflation was transitory. Inflation spiked post-Covid because the Fed was monetizing monstrous deficits. The sad part is they are still doing it. Government spending over the last 12 months has been off the rails with over $6.7 trillion spent to keep the illusion of a strong economy going. Did we say the election cycle has started?

The U.S. budget deficit for 2023 is looking like a giant sink hole.

“The Congressional Budget Office (CBO) estimated Tuesday that the federal budget deficit reached $1.6 trillion in the 10-month period ending in July. The agency said the amount is more than double the deficit seen during the same period the year prior, while noting a 10 percent drop in revenues and 10 percent increase in outlays.”

If you were wondering how the stock market and housing market were able to rebound during the first half of the year, wonder no more. As I have said numerous times, liquidity continues to be driving force behind the housing market. The “pent-up demand” story continues to be a work of fiction driven by monetary and fiscal stimulus with the Fed monetizing increasingly larger piles of debt. The Fed’s bloated balance sheet is still over $4 trillion higher than before the pandemic. The Fed is still sitting on $2.5 trillion in mortgage-backed securities. Those are the same instruments the Fed used to lower mortgage rates to the basement during the pandemic and severely distort the housing market.

Prospective home buyers are now paying dearly for the Fed’s hubris and market-distorting activities.

Headline inflation has been moderating for most of the year. That’s good news. That doesn’t mean the Federal Reserve has won the battle against inflation. Many industry pundits and apologists continue to talk about a soft landing for the U.S. economy. They are missing the bigger picture. There’s a lag effect to monetary policy. While some progress has certainly been made this year in terms of inflation, much of the damage is still lurking in the system.

Core services inflation was still ripping at 6.1% in July. Most consumers can relate. It’s still really expensive to get work done when you need it. No real surprise there. When asset prices spiral higher, workers respond by demanding higher wages. This fact has not been lost on some at the Fed. Even if they won’t say it out loud, they understand they will have to push the economy into a recession to truly kill that inflationary impulse. If the current wage-price spiral were to re-accelerate, that would wreak havoc on the economy and markets. In Layman’s terms, that would be really, really bad for the housing market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment