RECenter at A&M economists and data junkies are still wasting the dues of Texas Realtors that pay a good chunk of their salaries. It seems the Real Estate Center at Texas A&M economists are phase-locked in a myopic pursuit to somehow rationalize or justify the status quo situation with Texas housing.

“Intellectual Phase-Locking is a condition that results when dogmatic ‘scientific’ assumptions inhibit further inquiry.” Rupert Sheldrake

Last year I wrote about some of the interesting details on the Real Estate Center at Texas A&M and their funding. I have also clued readers in on the “new era of REC-FED cooperation” that arrived in 2012 along with the arrival of one Dr. Luis Torres, a research economist. That timing was probably more important than many Texas Realtors realized.

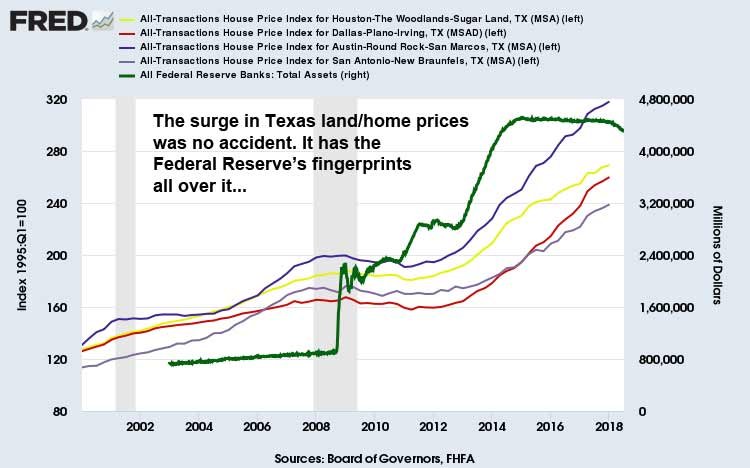

Particularly here in North Texas, that was when the Fed’s market-distorting, quantitative easing efforts were really kicking in with land and home prices. As the accompanying graphs clearly demonstrate, the Federal Reserve’s massive balance sheet expansion/asset inflation mechanism was firing on all cylinders from roughly 2012 to 2017, pushing stock prices to new highs along with North Texas home prices.

For all of their collective education and PhD profiles, the economists at the Texas A&M RECenter still can’t seem to bring themselves to mention the dirty little secret of the Texas housing market and the distortions that are causing severe affordability problems. They can tell us that “dirt isn’t cheap” or posit questions like “Where is all the new housing?”, but they continue to tap dance around the truth about Texas housing market distortions and why the current problems exist in the first place.

It would appear the economists at the Real Estate Center at Texas A&M are now mired in the same credibility trap of the Federal Reserve, their phase-locked views of Texas housing permeating much of their research. It’s bad enough that their data scientists have been missing the mark on real home sales volumes in DFW, but the slant of their “research” is probably even more disturbing. One could get the impression that RECenter research now closely resembles PR pieces for the Federal Reserve. Maybe this is the inevitable result of that new era of cooperation?

Truth be told, I don’t need five PhD’s to tell me that Texas has an affordable housing problem. Dr. Torres can keep deflecting attention from the causes of the lack of affordable housing or the dearth of new home construction, but a picture is worth a thousand words, even if he’s not willing to print it in the latest edition of Tierre Grande. Dr. Torres apparently wants me to believe that rising land prices and lagging labor productivity are the reason we don’t have enough new home construction. That’s absolutely laughable! This is how a PhD economist can waste a thousand words while telling you absolutely nothing you didn’t already know.

Yes, it’s true that rising land prices are a big part of the equation, but it would be nice if the good doctor would tell us whence those rising land prices came. I guess he doesn’t want to talk about the Federal Reserve’s direct interventions in the markets that prevented the appropriate “supply-side response”. I guess he doesn’t want to discuss how QE1, 2 and 3, along with the balance sheet expansion of other major central banks, inflated the cost of real estate in Texas and across the globe. I can only assume Mr. Torres not going to discuss how the Federal Reserve has directly facilitated wealth and income inequality since the Great Recession.

Dr. Anari’s recent article covering the ratio of Texas land prices to home prices skirts along the edge of the truth, but again there’s no chart or explanation of why Texas land prices have rebounded sharply following the Great Recession. Dr. Anari provides some nice charts showing how Texas land prices started taking off in 2012, yet the driver of those land price increases is strangely missing. Regulation, rising lumber and labor costs and other factors continue to be part of Texas’ affordable housing problem, but ultimately this is still a story about artificial asset inflation.

Since the economists at the RECenter at A&M seem to be unwilling to discuss it, here’s the picture telling you everything you need to know. This chart showing major Texas Metro house price indices overlaid with the Federal Reserve’s balance sheet mirrors the rise in Texas land prices. This is no coincidence. They are one in the same. The lines for the house price indices only run through the end of 2017, but I extended the range for the graph to capture the current tail of the Fed’s balance sheet, which is only now beginning to reflect that normalization process initiated last October.

Those phase-locked PhD economists at the RECenter will likely continue to waste my money, but I know where to look if I want the honest truth on Texas home price inflation and the root of our housing affordability problem. Completely reversing QE 1, 2 and 3 would help to solve Texas’ affordable housing problem, but you will likely never hear RECenter economists come out and say it. The resulting stock market collapse and home price deflation that would result from a collective unwind of global central bank balance sheets is not considered polite conversation among the status quo.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment