10 years after the housing crash and the Great Recession that nearly brought the world economy to its knees, the adults in the room are still pretending that everything is normal. If you read the Dallas Morning News and the spin of many professional economists, the DFW real estate market has emerged from the wreckage 10 years ago relatively unscathed. With DFW home prices at record highs, most housing pundits are eager to suggest everything is awesome. Apparently the recent rise in home inventories is just blip in an otherwise normalization of the formerly red hot housing market. But is it?

For those who have bothered to look, there is very little that is normal with today’s real estate markets. As I mentioned in a previous post, comparing the current bull market in real estate and stocks without mentioning the unprecedented interventions in the markets by the government and the Federal Reserve borders on the verge of journalistic incompetence. The media, and certainly many within the real estate industry, continue to push the “recovery” narrative, because that’s what sells.

The official narrative is full of holes if you bother to look, but the show must go on. Every day is a great day to buy a home is still the battle cry of your average real estate agent. Never mind the egregious policy errors that distorted real estate prices and enriched the wealthy and well-connected. Pay no attention to the obvious dislocation of Dallas-Fort Worth home prices from historical fundamental metrics like wage growth. “This time is different”, they will say.

“History is a vast early warning system.” Norman Cousins

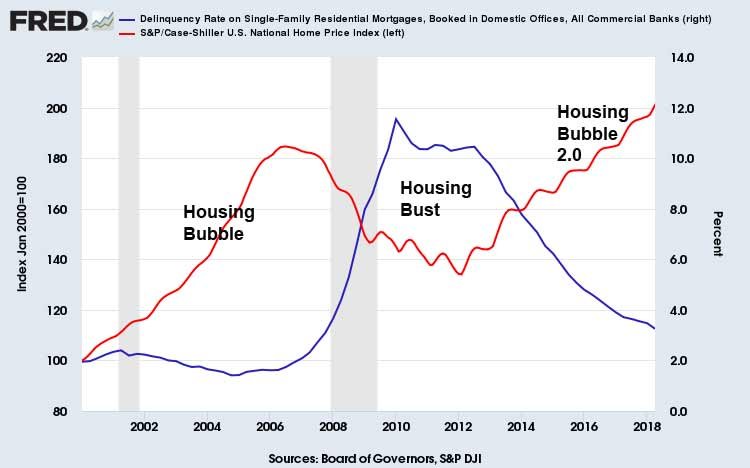

The DFW housing market has not fully dealt with the policy errors of the past 10 years. Not by a long shot! Texas as a whole was largely unaffected by the last housing downturn, but that doesn’t mean it will exit this current market cycle unscathed again, particularly when it has become so intertwined with the Federal Reserve’s policy distortions. As the attached graphic shows quite clearly, Dallas Texas home prices are definitely in bubble territory. To be sure, the robust economy and recovery in Texas contributed to the rise in local home prices. But more than anything else, the last 10 years have been about a continued narrative to cover up the crash with few, if any, real lessons actually learned, and no consequences whatsoever for the financial elite who profited from the fraud.

When a trio of Wall Street puppets are busy peddling the official (and blatantly erroneous) narrative of the crisis and the recovery, it’s refreshing that there are still some people who remember what actually happened. This past week Matt Taibbi penned a brilliant rebuttal to establishment narratives, highlighting 3 of the primary myths of the bailouts. Chief among those oft-repeated myths is that the bailouts were necessary to save capitalism. In reality, the bailouts were orchestrated and implemented to insulate Wall Street from capitalism and the consequences of reckless greed and obvious criminal behavior.

“An already-serious economic inequality issue became formalized. The people responsible for the crisis weren’t just saved, but made beneficiaries of another decade of massive unearned profits.”

Matt Stoller also penned a wonderful piece this week detailing how the entire concept of home ownership and property rights was turned on its head following the crash. As Stoller is careful to note, the bailouts which took place between 2007 and 2009 have had profound effects on the U.S. real estate market, primarily because the policies enacted to save the “system” caused untold damage for working-class Americans and the social contract in general. Rather than push the lauded goal of home ownership, the previous administration went out of its way to push renting over owning a home, while some large Wall Street firms were practically gifted thousands of single-family homes which they now rent to those foreclosure victims.

If the policy shift had simply been about pushing more people to rent, that might have been a forgivable transgression, but the policies of Obama, Geithner and Holder went far beyond that, as they systematically and selectively applied the rule of law to favor corporations and wealthy individuals over average Americans.

“During the crisis, everyone needed money from the government, but Geithner offered money to the big guy, and not the little guy…(Eric Holder, meanwhile, also de facto granted legal amnesty to executives for possible securities fraud associated with the crisis.) Second, Geithner chose to deny money and credit to the middle class in the midst of a foreclosure crisis. The Obama administration supported this by neutering laws against illegal foreclosures.”

One thing that should be perfectly clear 10 years later is the fact that the crisis was ultimately about elite white collar fraud. As banking analyst Christopher Whalen explains, we never talk about the real cause of the crisis, “namely securities fraud fraud by some of the biggest firms on Wall Street.” In a reminder that nothing has really changed, Whalen is also quick to point out that all of the extra “capital” the media and the Fed like to talk about is irrelevant when derivatives are still a huge part of the financial system.

Things could have played out far differently following the financial collapse, but alas it wasn’t meant to be. Leaders during the previous administration were working hand in hand with the Federal Reserve to shove trickle-down monetary and fiscal stimulus at the U.S. housing market and the economy in general. It should come as no surprise that much of that stimulus never reached the real economy, and certainly many of the areas in flyover country where millions of Americans are still underwater on their mortgages.

The former Fed chair during the Roosevelt administration, Marriner Eccles, is likely rolling over in his grave. He understood the importance of the distribution of economic wealth. In 1935 he was lamenting to Congress that a primary problem for the U.S. economy was “one of distribution of income”. Like FDR, Eccles understood that unbalanced wealth was a primary cause of the Depression, and a subsequent impediment to recovery.

When I hear real estate pundits suggesting that we’re finally getting back to normal, I often catch myself biting my lip. The establishment narratives of the Great Recession refuse to die, and many of my colleagues in the real estate industry certainly don’t help the situation when they refuse to talk about issues that have yet to be resolved. On the 10-year anniversary of what is likely the greatest wealth transfer in human history, it pains me to say that nothing really has changed.

We can pretend that the Dallas-Fort Worth real estate market is not a bubble. We can pretend that systemic fraud in the financial system is no longer a problem. Of course neither statement is true, and the longer we pretend otherwise, the longer we will be forced to deal with the consequences of egregious policy failures from leaders who promised much, but ultimately placed their own interests (and those of their corporate lobbyists) before the interests of the American public.

While real earnings for many Americans are barely treading water, mortgage interest rates are now back up to those make or break levels where the rubber hits the road. The U.S. federal budget deficit nearly doubled in August as deficits continue to pile up under Trumps corporate tax cuts and military spending glut. The budget deficit was a massive $895 billion for the first 11 months of fiscal 2018. Truth be told, Trump has no plan for paying down the ballooning federal debt. He’s just marching to the orders of Wall Street, just like the previous administration did. That reality will sink in eventually as the bills keep piling up.

Could it be that the “recovery” is just a continued mirage built on central bank liquidity and government policy favoring the rich? Time will tell. Mortgage delinquencies fell to 3.14 percent during the second quarter of the year, but those low delinquency rates can be deceiving. Delinquency rates are a function of both leverage and home prices. Those marginal buyers don’t default on their loans until home prices start declining, the point at which loose underwriting standards and small down payments put borrowers underwater.

“Trickle-Down-Theory – The less than elegant metaphor that if one feeds the horse enough oats, some will eventually pass through to the road for the sparrows.” John Kenneth Galbraith

“Government has coddled, accepted, and ignored white collar crime for too long. It is time the nation woke up and realized that it’s not the armed robbers or drug dealers who cause the most economic harm, it’s the white collar criminals living in the most expensive homes who have the most impressive resumes who harm us the most. They steal our pensions, bankrupt our companies, and destroy thousands of jobs, ruining countless lives.” Harry Markopolos – long-ignored Madoff whistleblower

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Aaron, always amazing writing. Thank you for your ability to always brilliantly summarize what is going on. Hope you are doing well. I see you moved out of Houston. I ended up moving to Mcallen. We need to play tennis one day when I am in DFW ! Hope you are doing well!